BEIJING, Sept. 18 (Xinhua) -- The Baltic Exchange has published its weekly report of the dry and tanker markets for September 11-15, 2023 as below:

Capesize

The week in the Cape market has shown a mix of activity in both the Pacific and Atlantic regions. In the Pacific, the week began positively with two major players active in the market, contributing to a slight uptick in rates. Increased coal enquiries provided overall market support. However, as the week progressed, conditions stabilised, and activity became subdued. Towards the end of the week we witnessed increased activity, characterised by significant volume of cargo. This heightened market activity led to improved sentiment and a further increase in rates. In the Atlantic, the North Atlantic region saw tight conditions leading to improved fixtures. At the outset of the week, activity in the South Atlantic was sluggish, but it gradually gained momentum as the week unfolded. The C3 market had solid support, highlighted by the upward movement in rates from South Brazil and West Africa to the Far East. Overall, the week saw fluctuating market conditions, with the Pacific experiencing intermittent activity and the Atlantic showing signs of positivity.

Panamax

A strong week for the Panamax sector with steady rises throughout the Atlantic and Asian markets although we seemed to have reached a period of consolidation as the week ended. From the Atlantic basin, we saw decent levels of both grain and mineral demand versus a limited tonnage list, creating the perfect storm for owners, reports of close to $30,000 achieved for quick duration trips via US east coast to India. South America focus appeared to be for the end of September arrival with a host of deals concluded. Asia was mostly NoPac centric, ably supported by solid mineral demand ex Australia and Indonesia enabling rates to climb from the doldrums of recent months, rates in the $15,000’s not uncommon for NoPac round trips, even in the $17,000’s for the real decent spec types with Japan delivery. A bunch of period deals concluded the highlight $14,650 agreed basis one year on an 82,000dwt type delivery China.

Ultramax/Supramax

A better week for the sector, with increased levels of enquiry from key areas. From the Atlantic, stronger numbers were recorded from the Continent-Mediterranean regions. The US Gulf remained evenly balanced, but some healthier numbers also appeared. Whilst from South America a tightening of prompt tonnage helped sustain levels. From Asia, increased enquiry from Indonesia both to China and India was seen and owners’ expectations across the region increased. Period cover was sort, a 58,000dwt fixing delivery Los Angeles end September for three to five months trading at $12,000 plus $400,000 ballast bonus. From the Atlantic, a 58,000dwt was fixed delivery Fos for a trip to China around the mid $20,000s. Whilst from US Gulf a 58,000dwt was heard to have fixed a trip via US East Coast redelivery China at $20,000. In Asia, a 61,000dwt open SE Asia was reported fixed for an Australian round voyage at $17,000. A 63,000dwt open Chittagong was fixed for a log’s run via New Zealand redelivery WC India at $14,000.

Handysize

Divided sentiment for the sector as healthier numbers were seen in the Atlantic, from Asia brokers generally described the week a fairly flat with cargo and tonnage levels remaining balanced. However, as the week closed some felt that there was a slight shift with a few more cargoes appearing from North Asia. In the Atlantic, better numbers were being achieved from the Continent-Mediterranean, a 35,000dwt was heard fixed basis delivery Kalamata for a trip via Turkey to Durban with redelivery EC South America in the mid $15,000s. Further north, a 36,000dwt was fixed delivery Continent for a trip to EC South America with fertiliser at $13,000. Elsewhere, a 38,000dwt fixed delivery US East Coast for a trip to the Continent-United Kingdom with wood pellets in the upper $12,000s.

Clean

LR2

LR2 freight levels in the MEG rose optimistically early on this week only to then come to a halt. TC1 topped out at WS145 up from WS136 to then resettle at WS142.78 at time of writing. At the WS145 mark the Baltic TCE ticked over the $30,000/day round trip. Meanwhile a run to the UK-Continent on TC20 gradually hopped up from $3,810,000 to $3,950,000.

West of Suez, Mediterranean/East LR2’s saw the TC15 index for second week on week continue along in the low $2,900,000 region.

LR1

In the MEG, LR1’s have led the pack this week with a consistently firming sentiment. The TC5 index added 24.06 points to WS169.69 and TC8 hopped up $135,000 to $3,420,000.

On the UK-Continent, TC16 held resolute in the mid WS160’s all week with the TCE hovering around $31,000-32,000/day level.

MR

Despite an increase in activity on MEG MR’s this week and a subsequently strengthening market the TC17 index has held in the WS290 region all week.

UK-Continent MR’s after the significant improvement on last week look to have stagnated at current levels. After reaching WS182.75 early in the week, up from WS172 the TC2 index has now been suspended there for the last three days. TC19 has mirrored TC2 as per usual practice and currently sits at WS190.

In the USG MR’s have come under a significant amount of pressure this week. Even with Panama canal delay days still in the double figures TC14 has shed 34.16 points to WS94.17 and TC18 has gone from WS228.33 to WS180. Similarly on a run to the Caribbean on TC21 freight has dropped 43 percent this week to $516,667. The Baltic TCE’s at these levels are notably sombre, especially TC14 at only $554/day.

The MR Atlantic Triangulation Basket TCE dropped from $24,941 to $18,717.

Handymax

In the Mediterranean, Handymax’s have resurged optimistically this week, tonnage has been tight and enquiry high leading the TC6 index to add 75.56 points to WS275.56. Up on the UK-Continent, the TC23 index yet again rattled along at the WS190 mark.

VLCC

The market remained static this week with rates being held, presumably on the floor. The rate for 270,000mt Middle East Gulf to China was maintained at just below WS37 corresponding to a daily round-trip TCE of $4,244 basis the Baltic Exchange’s vessel description. The 280,000mt Middle East Gulf to US Gulf trip (via the cape/cape routing) was assessed at WS22.89, much like the level seen a week ago.

For the Atlantic market, the 260,000mt West Africa/China rate hovered around the WS43 (which shows a round voyage TCE of $13,725/day). The rate for 270,000mt US Gulf/China climbed a meagre $25,000 to $7,116,667 ($19,347/day round trip TCE).

Suezmax

Suezmaxes in West Africa continue to flirt with the bottom of the market. The rate for the 130,000mt Nigeria/Rotterdam trip lost a solitary point to WS71 (a daily round-trip TCE of $14,500). In the Mediterranean and Black Sea region the 135,000mt CPC/Med route has been held at the WS72 level (showing a daily TCE of $6,800 round-trip), although tonnage has started to build up again potentially leading to softer sentiment both here and in West Africa. In the Middle East, the rate for 140,000mt Basrah/Lavera eased 3.5 points to a fraction below WS56.

Aframax

In the North Sea, the rate for the 80,000mt Hound Point/Wilhelmshaven route modestly gained two points to WS95 (still showing a negative round-trip daily TCE, about -$600). In the Mediterranean market the rate for 80,000mt Ceyhan/Lavera slipped five points to about WS85 (a daily round trip TCE of $3,500).

Across the Atlantic, in the Stateside Aframax market, the rate for 70,000mt East Coast Mexico/US Gulf eased almost two points to a shade under WS95 (which shows a TCE of $2,800/day round trip) and for 70,000mt Covenas/US Gulf the market rate has had 3.5 points shaved off it to WS93.44 (a round-trip TCE of $5,000/day). The rate for the trans-Atlantic route of 70,000mt US Gulf/Rotterdam has lost about nine points to WS98.75 (a round trip TCE of $10,273/day).

LNG

After a successful and well attended Gastech in Singapore the market has come back to life, refreshed and invigorated. Rates for all three routes saw good gains with the Atlantic showing a particular comeback, brokers have reported that in terms of activity the Atlantic is now catching up with the East.

BLNG1g Aus-Japan saw $16,026 gained on the week bringing up freight to $185,884 on a round trip basis. Reports of some intra pacific private deals fueling strength in a continued rise for rates. BLNG2g US-UKC gained an impressive $24,534 to close at $182,969 while BLNG3g US-Japan finished at $219,219. Fixing windows have moved out well into the depths of the upcoming winter market and rates are reflecting this now.

LPG

The LPG market has remained firm this week with BLPG1 Ras Tanura-Chiba rising $4 over the week to close at $155.429, giving a daily TCE earning of $144,676. A relatively tight tonnage list and continued cargoes being shown has kept levels high. With more expected cargoes coming into the works the quieter end to the week is perhaps the calm before the continuing storm.

The Atlantic was busy with fixing though this is still behind the same level of fixtures concluded at this time last year. What is more positive is that rates have risen again, with BLPG2 Houston-Flushing moving $5.2 and over $6,500/day to close at $123.8 for a round trip with TCE earnings at $145,729. For the eastern run BLPG3 Houston-Chiba a slightly more reserved rise gave a week’s close of $223.143 and a TCE earning of $133,128.

Headquartered in London and a subsidiary of the Singapore Exchange (SGX), the Baltic Exchange publishes a range of indices and assessments which provide an accurate and independent benchmark of the cost of transporting commodities and goods by sea. These include the Baltic Dry Index (BDI), the dry bulk shipping industry's best known indicator. Published daily since 1985, this provides a snapshot of the daily spot market earnings of capesize, panamax and supramax vessel types on the world's key trading routes.

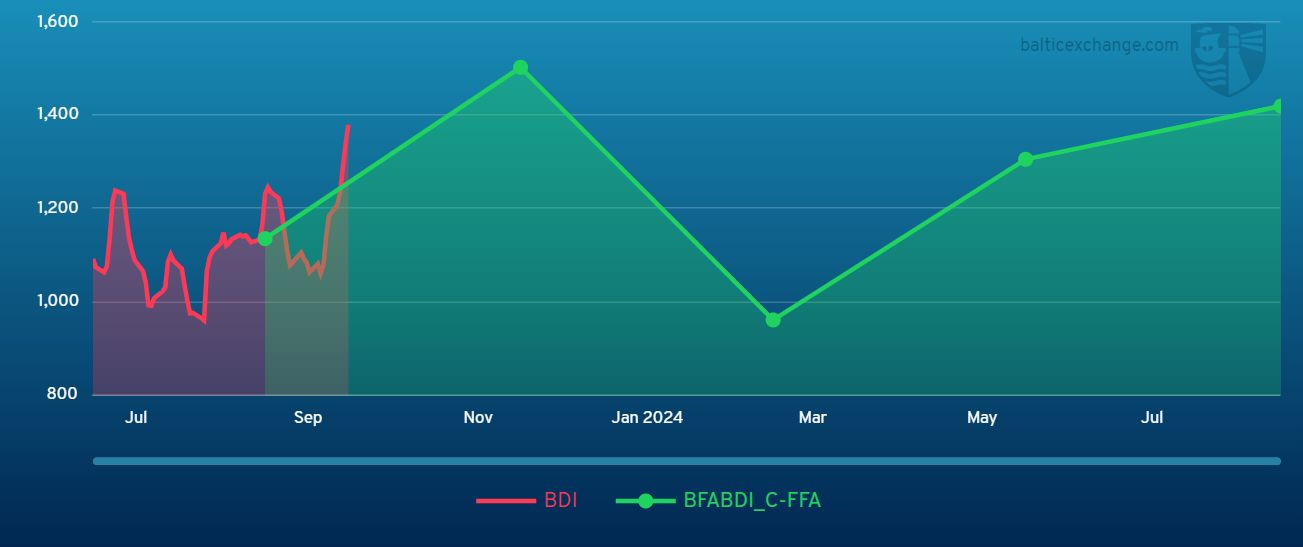

Chart shows Baltic Dry Index (BDI) during Sept.16, 2022 to Sept.15, 2023

Baltic Forward Assessment for BDI

In March 2018 the BDI was re-weighted and is published using the following ratios of time charter assessments: 40 percent capesize, 30 percent panamax and 30 percent supramax. The information is provided by a panel of international shipbrokers.

(Source: The Baltic Exchange, edited by Niu Huizhe with Xinhua Silk Road, niuhuizhe@xinhua.org)

A single purchase

A single purchase