BEIJING, Oct. 23 (Xinhua) -- The Baltic Exchange has published its weekly report of the dry and tanker markets for October 16-20, 2023 as below:

Capesize

The Capesize market experienced a strong week with the timecharter average breaking over $30,000/day, the highest value in 17 months. However, the surge hit pause on Thursday and the 5TC slipped below the threshold to $29,493 on Friday. Strong rates were reported from north Atlantic, regardless of short or long duration fronthaul trips, with tonnage list remaining tight throughout the week. Early loading dates from Saldanha Bay and Brazil paid a good premium on vessels with prompt dates. A Tubarao to Qingdao run was paying $25.772, or about mid $21,000s, for a China-Brazil round trip. In the Pacific, decent cargo levels were traded when the week first began but with only one major in the market later of the week, settling the West Australia to Qingdao run at $10.70. The second half of the week was slower across both basins in general.

Panamax

The Panamax market returned a real Atlantic/Asia divide this week. The Atlantic market progressed all week, particularly midweek, primarily driven by both solid mineral and grain demand both for trans-Atlantic and fronthaul trips, with the former assisted by some cape split cargo entering the fray. The headline rate was an 81,000 dwt delivery Gibraltar securing $18,000 for a trans-Atlantic grain round trip. South America added sound support, with a host of deals concluded for first-half November arrival window at rates better than last done. It was a lethargic Pacific market this week, except for a minor push ex-Indonesia where demand remained steady all week, but mostly absorbed by smaller/older type tonnage. Disappointing demand ex-NoPac and Australia failed to lend any support to rates and numbers for these longer runs drifted over the course of the week. Period activity was limited, with a scrubber-fitted 82,000 dwt delivery China achieving $15,500 for a one-year period.

Ultramax/Supramax

Overall, a rather subdued end for the week. The only bright spark was from the US Gulf, which saw a strong rebound at the beginning with better levels of enquiry and tightness of prompt tonnage. Other areas within the basin remained at best stable but an increasing lack of fresh cargo saw rates put under downward pressure. From Asia, the week was slow to pick with limited fresh enquiry appearing in most quarters but as it closed, more enquiry was being seen. However, there still remained a good supply of tonnage. Period action was fairly sparse, but a 63,000 dwt open Continent fixed for minimum four months trading redelivery worldwide at $18,750. In the Atlantic, a 61,000 dwt fixed delivery SW Pass redelivery Far East at $35,000. Whilst a 62,000 dwt fixed a trip delivery US east coast redelivery China at $31,500. In Asia, a 61,000 dwt open Japan fixed a NoPac round at $13,000. Further south, a 64,000 dwt open Singapore fixed a trip to India at $20,500 (scrubber benefit to owners).

Handysize

Levels continued to improve in the south Atlantic, with a 36,000 dwt fixing from Rio Grande to Caldera at $26,000, whilst a 37,000 dwt was rumoured to have been fixed from north Brazil to Algeria with an intended cargo of grains at $21,000. The Mediterranean slowed as the week progressed with limited fresh cargo and suggestion that events in the region were also playing their part, a 36,000 dwt opening in Varna was fixed for a trip via Romania to the Continent at $14,000. On the Continent, a 40,000 dwt fixed from Bremen to the US east coast with lumber at $16,650. In Asia, activity was subdued across the region and numbers had begun to soften, a 40,000 dwt opening in the Philippines was fixed via Indonesia to Malaysia at $12,750 whilst a 32,000 dwt opening in Brisban on 1 November was fixed to north China at $13,500. Period activity also remained, with a 38,000 dwt opening in Conakry fixing for four-to-six months with worldwide redelivery at $13,500.

Clean

LR2

LRs in the MEG have again been at the forefront of activity this week. Although rates have not climbed exponentially, sentiments have been firm in the MEG all week for the largest of CPP vessels. TC1 hopped up 19.72 points to WS171.11 and for a run westward on TC20 the index improved $343,750 to $4.475m.

West of Suez, Mediterranean/East LR2’s on TC15 improved an optimistic $333,333 this week to $3.57m.

LR1

In the MEG, LR1’s have not been as active as the LR2’s this week. Freight rates have been held up by the strong sentiments from above. TC5 held stable in the WS171-176 range all week. Similarly on a trip to the UK-Continent on TC8 levels hover around the $3.6m mark all week.

On the UK-Continent, the TC16 index, for the third week ticked along at around WS155.

MR

MR’s in the MEG have been a touch lacklustre this week. Supply/demand remains in balance and the improving LR’s will have helped prevent rates from dipping. The TC17 index has, as a result, hovered around the WS235-245 level.

UK-Continent MR’s have suffered from a distinct lack of enquiry this week. Subsequently TC2 and TC19 rates come under pressure and we saw both drop around 12-13 Worldscale points with TC2 currently pegged at WS142.5 and TC19 at WS152.19. Another bout of downward movement will take the TC2 Baltic TCE below the $10,000/day level.

A quieter start to the week combined with a notable oversupply of vessel led the USG MR’s to soften again this week. For the sixth time this year TC14 dropped into double figures losing 22.38 points to currently sit at WS99.29. TC18 also went below WS200 this week with the index 41.45 points lighter at WS179.29 at time of writing. A short run to the Caribbean on TC21 also lost 20% of its value this week and is pegged at $596,429 for the moment.

The MR Atlantic Triangulation Basket TCE lost just under 30% of its value shedding $6,591 to $15,777.

Handymax

In the Mediterranean, Handymaxes looked to have reached a balanced position this week. A lack of enquiries slimmed down the available tonnage kept the TC6 index around the WS185 level.

Up on the UK-Continent, the TC23 index recovered to the tune of 6.94 points to WS173.61.

VLCC

The market powered on from last week for the first couple of days, with rates climbing with each fixture until Wednesday when cracks started to appear in the owners’ steadfastness. The market is now softer than a week ago and sentiment is lower. The rate for 270,000 mt Middle East Gulf to China rose to WS63 and has now fallen back 2.5 points week-on-week to WS55.54 corresponding to a daily round-trip TCE of $28,774 basis the Baltic Exchange’s vessel description. The 280,000 mt Middle East Gulf to US Gulf trip (via the cape/cape routing) is now assessed 0.5 points up on a week ago at WS32.

In the Atlantic market, a similar tale was evident with the 260,000 mt West Africa/China rate rising to WS64 then falling back two points since last Friday to WS58.85 (which shows a round voyage TCE of $33,896/day). The rate for 270,000 mt US Gulf/China ascended to $10,200,000 but has been reduced by $397,222 week-on-week to $9,902,778 ($42,742/day round trip TCE).

Suezmax

Suezmaxes in West Africa have had another steady week of gains. The rate for 130,000 mt Nigeria/UK Continent rose to WS121 but has now slipped back to three points above last Friday’s number to WS119.55 (a daily round-trip TCE of $47,790). In the Mediterranean and Black Sea region, the 135,000 mt CPC/Med route, buoyed by a firm Aframax market adding support, rocketed 35 points to WS135.05 (showing a daily TCE $59,624 round-trip). In the Middle East, the rate for 140,000 mt Middle East Gulf to the Mediterranean amassed eight points over the week to WS82.83.

Aframax

In the North Sea, the rate for the 80,000 mt Cross-UK Continent route continued the upward trajectory, rising 24 points to WS153.57 (showing a round-trip daily TCE of $51,900 basis Hound Point to Wilhelmshaven). In the Mediterranean market where demand was high, the rate for 80,000 mt Cross-Mediterranean is another 37 points firmer at WS216.06 (basis Ceyhan to Lavera, which shows a daily round trip TCE of $75,871).

On the other side of the Atlantic, the market continued to firm for the shorter voyages, while trans-Atlantic was softer. The rate for 70,000 mt east coast Mexico/US Gulf has shot up another 55 points since last Friday to WS267.81 (a daily round-trip TCE of $86,179) and the 70,000 mt Covenas/US Gulf rate escalated 42 points to WS243.44 (a round-trip TCE of $70,211/day). The rate for the trans-Atlantic route of 70,000 mt US Gulf/UK Continent was reduced by 10 points to WS201.88 (a round trip TCE basis Houston/Rotterdam of $51,653/day) as owners seemingly wanted to get back to Europe.

LNG

A subdued LNG spot freight market has kept rates relatively flat. Consensus among market players only exists in that there isn’t much driving force up or down otherwise there are contrasting opinions of where the market should go. With few spot enquiries any change has been driven by some tenders offered up in the Atlantic ex Bonny for end November and mid-December and Middle East from Oman for start November while in Asia there has been few enquires made. LNG pricing fluctuations has diminished the tonnage list while portfolio players have removed relets from circulation to cover internal movements.

Rates themselves haven’t done much with BLNG1g Aus-Japan losing only $4,916 to close at $124,592 while the Atlantic runs BLNG2g USG-Cont finished at $127,679 and USG-Japan BLNG3g moved $135 down only to finish at $158,920. Period has calmed, with rates steady with a one-year timecharter on a 174cbm 2 stroke at $108,467.

LPG

The market has been up and down this week losing nearly $20 off the start of the week by the midpoint but the index rose again to close at $112.857 (an actual fall of $1.143 on the week) giving a daily TCE of $95,990. With the fixing window now looking out to the last decade of November, the earlier and more ‘affordable’ ships already fixed away has helped bolster rates and by the tail end of the week we had a rise of over $16 in one day.

The US market has suffered heavier casualties with both BLPG2 and BLPG losing quite a chunk of their value. Houston-Flushing BLPG2 lost $13.4 to finish at $101.8 meaning a daily TCE earning on a round voyage was $114,968. While Houston-Chiba lost $24.143 giving a closing index value of $185.857 and a daily TCE earning of $102.628. With delays in Panama causing headaches for charterers we have seen an increase of freight rates with options to go via the Cape rather than via the canal. Overall enquiry has been down and all three routes have corrected with brokers estimations they should remain flat.

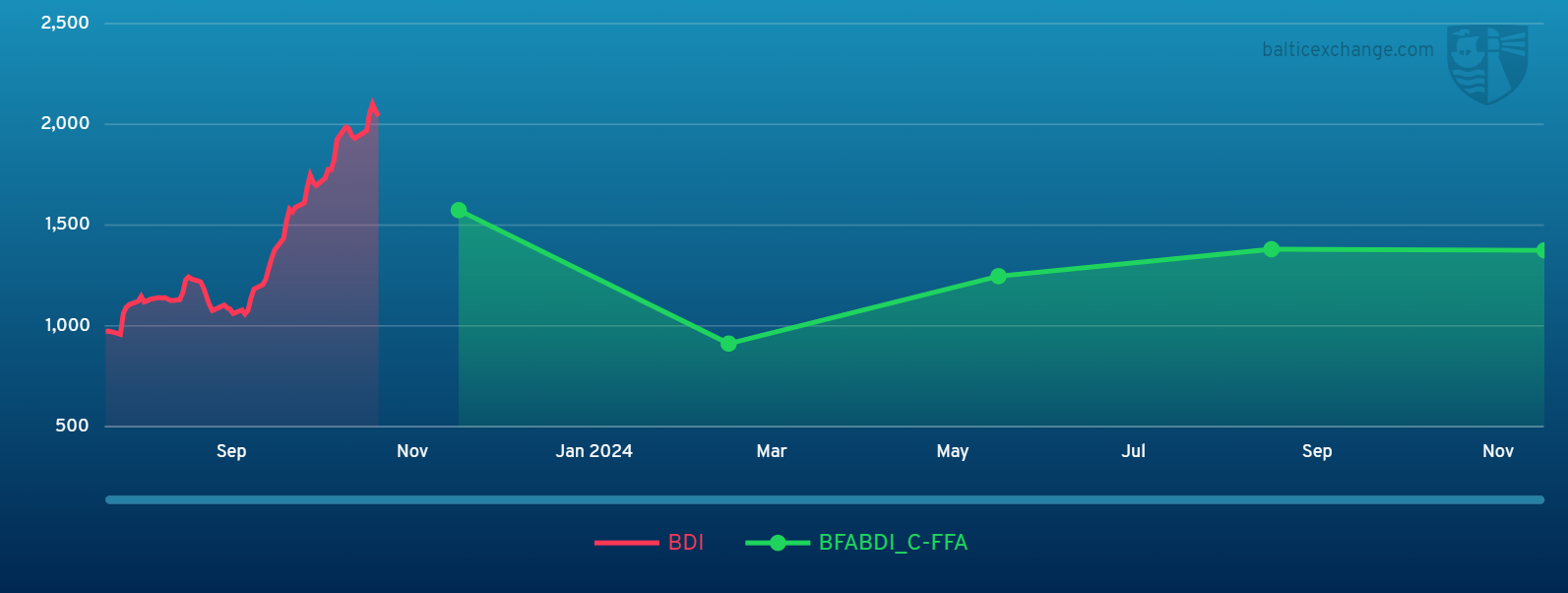

Headquartered in London and a subsidiary of the Singapore Exchange (SGX), the Baltic Exchange publishes a range of indices and assessments which provide an accurate and independent benchmark of the cost of transporting commodities and goods by sea. These include the Baltic Dry Index (BDI), the dry bulk shipping industry's best known indicator. Published daily since 1985, this provides a snapshot of the daily spot market earnings of capesize, panamax and supramax vessel types on the world's key trading routes.

Chart shows Baltic Dry Index (BDI) during Oct. 20, 2022 to Oct. 20, 2023

Baltic Forward Assessment for BDI

In March 2018 the BDI was re-weighted and is published using the following ratios of time charter assessments: 40 percent capesize, 30 percent panamax and 30 percent supramax. The information is provided by a panel of international shipbrokers.

(Source: The Baltic Exchange, edited by Niu Huizhe with Xinhua Silk Road, niuhuizhe@xinhua.org)

A single purchase

A single purchase