BEIJING, May 8 (Xinhua) -- The Baltic Exchange has published its weekly report of the dry and tanker markets for May 1-5, 2023 as below:

Capesize

All in all, it has been a rather uninspiring week for the capes. Various holidays in Asia have had a small impact creating perhaps a quieter feel. Volumes from West Australia to China have been relatively low, resulting in a very flat market, although, as the week in Asia comes to an end, there are rumours of slightly better fixtures being concluded. Sources said earlier in the week fresh coal cargoes were emerging from East Coast Australia to China, and the level of fixing activity increased towards the end of the week. The Atlantic started the week with slightly more optimism, brokers said supply of tonnage was tight in the North Atlantic, and fresh enquiry was emerging, both within the Atlantic and fronthaul. Stronger fixtures were concluded by the middle of the week. However, there was a slight shift in sentiment towards the end of the week, with softer fixtures being concluded, resulting in a rather static market.

Panamax

An uneventful week largely fragmented by various holidays spread across the globe. The Atlantic basin saw very little fresh demand, as many charterer/operator business visible in the market cast a false picture as most of these had backstop tonnage behind but, aside mid-week of a mini grain push ex NC South America, this did little to stem the slow erosion of rates all week across all routes. Some voyage fixtures ex EC South America came to light for June dates, with reports of $42.75 fio agreed ex Santos to China. Asia with varying holidays returned little cheer for owners too, with the Indonesian round coal trips being the most engaging beginning the week around the $13,500 mark but slipping to closer to $12,500 by the close. Unsurprisingly, with very little support from the FFA market, there returned limited period news, reports of an 82,000dwt delivery in China achieving $17,250 basis 5/7 months.

Ultramax/Supramax

A rather uninspiring week overall with holidays in many areas at the beginning, this led to a limited amount of fresh enquiry and a good supply of prompt tonnage. As a result, rates struggled in most regions, brokers saying key areas such as the US Gulf, East Coast South America and Southeast Asia remained positional. From the Atlantic, a 55,000dwt was heard fixed delivery US Gulf for a trip to Singapore-Japan at $21,500. Further south, a 61,000dwt was heard fixed delivery Santos for a trip to Chittagong at around $17,000 plus $700,000 ballast bonus. From Asia, limited activity surfaced. An ultramax open Japan fixing a NoPac round redelivery SE Asia-Sri Lanka with grains in the low teens, while a 56,000dwt fixed delivery passing Singapore trip via Indonesia redelivery India at $10,000. From the Indian Ocean, a lacklustre feel, although a 61,000dwt was heard fixed delivery East Coast India for a trip to China at $11,000.

Handysize

In a week full of holidays, there was minimal visible activity across the sector leading to negativity across both basins. In the South Atlantic, levels of open prompt tonnage were said to have increased and a 37,000dwt was fixed basis delivery where ready in Rosario for a trip to the Caribbean at $20,000. The US Gulf also saw minimal prompt enquiry and a 32,000dwt was fixed basis delivery US Gulf for a trip to East Coast Mexico with an intended cargo of grains at $12,500. In the Eastern Mediterranean a 35,000dwt fixed basis delivery passing Canakkale via Varna to Tunisia with an intended cargo of grains at $11,000. A 32,000dwt open in the Caribbean was fixed for 3 to 5 months, with redelivery in the Caribbean at $12,500. In Asia, a 36,000dwt open in Niihama was fixed for 3 to 5 months at $13,250 and a 36,000dwt open spot was fixed for 2 to 3 laden legs at $11,500.

Clean

LR2

LR2’s in the MEG took a major retest down this week. TC1 has dropped 33.13 points to WS147.5 and for a trip west on TC20, a widely reported fixture late in the week, saw a $842,000 chunk taken out of the index to $3,657,143.

West of Suez, Mediterranean/East LR2’s have been sombre. The TC15 index has dropped $254,000 to $3,220,833.

LR1

In the MEG, LR1’s have been relatively steadfast. TC5 took a dip from WS200 to WS191 end of week and TC8 shed $325,000 from $3,849,950 to $3,524,950 off the back of the LR2’s softening.

On the UK-Continent, TC16 remained mute this week, seeing the index drop from WS155 to WS138.75. Despite this, the round trip TCE is still up in the mid $26,000 /day.

MR

MEG MR’s saw more negative freight movements this week as a result of the market sedation in the Far East. TC17 lost 37.86 points to WS191.43.

Steady activity on the UK-Continent this week drove a tick up in freight levels. TC2 peaked at WS173.89 mid-week then resettled at WS169.72 (a 26.66 point improvement on this time last week). TC19 followed suit, topping out at WS182.86 and currently pegged at WS178.85. This has taken the round trip TCE’s for these runs back over the $20,000/day mark.

In the US Gulf, the MR’s returned to life this week and rates rebounded. TC14 climbed back up over the WS100 mark to WS110.42 with that level reportedly done several times mid-week. TC18 added 25 points to the index to WS178.75 and a trip to the Caribbean on TC21 hit the $700,000 mark again (+$191,667).

The MR Atlantic Triangulation Basket TCE improved 52% to $25,949.

Handymax

Mediterranean Handymax’s look to have levelled off this week and TC6 has hovered around the WS145-150 mark. Up on the UK-Continent TC23, which dipped 15 points to WS153.13.

VLCC

The VLCC market was quiet this week, with the Far Eastern holiday season under way and, because of the resultant limited demand, rates fell. The rate for 270,000 mt Middle East Gulf to China retracted by about 10 points to WS46.41, which corresponds to a round trip TCE of $27,400 per day basis the Baltic Exchange’s vessel description. The rate for 280,000mt Middle East Gulf to US Gulf (via the cape/cape routing) is now assessed at almost 5 points lower than a week ago at WS33.17.

In the Atlantic market, the rate for 260,000mt West Africa/China needed testing, and on Thursday the market was assessed at WS45, 12 points down week-on-week, which shows a daily round voyage TCE of $23,700 after Unipec were reported to have taken a Koch relet on subjects at this level.

The rate for 270,000mt US Gulf/China is now assessed $794,445 lower than a week ago at $7,161,111 ($27,200 per day round trip TCE), unaided by very little interest or activity.

Suezmax

The Black Sea and Mediterranean markets were flat this week. The rate for 135,000mt CPC/Med remains at around WS122.5 (a round trip TCE of $53,900 per day). In the Atlantic region, the Caribbean and US Gulf markets drew tonnage away from West Africa and rates firmed for 130,000mt Nigeria/Rotterdam, which now sits 2.5 points up on last Friday’s assessment at WS92.25 (a round trip TCE of $35,600 per day). In the Middle East, the rate for 140,000mt Basrah/Lavera recovered about 4 points to just shy of WS60.

Aframax

In the North Sea market, the rate for the 80,000mt Hound Point/Wilhelmshaven route remained flat at around the WS130 level (showing a round-trip daily TCE of $38,300).

In the Mediterranean, the rate for 80,000mt Ceyhan/Lavera firmed 10 points to WS162.5 (a daily round trip TCE of $51,300).

Across the Atlantic, the Stateside Aframax market reached bottom last Friday and the bounce-back has been gathering pace this week. A tonnage tightening situation and a sudden in-flux of cargo enquiry mid-week gave the owners all they needed to regain lost ground.

The rate for 70,000mt East Coast Mexico/US Gulf is now almost 97 points higher than a week ago at WS188.75 ($57,000 per day round-trip TCE) and the rate for 70,000mt Covenas/US Gulf has risen 82.5 points to WS170 (a daily round-trip TCE of $44,300).

For the trans-Atlantic route of 70,000mt US Gulf/Rotterdam, the rate rallied 45 points to WS170 (showing a round trip TCE of $44,400 per day).

LNG

With holidays in the East, and a short week in the UK the market had expected to remain flat as it has for the last few weeks. But there was some spot enquiry during the first half of the week that got participants excited for potential burst of fixing, but with most of this ending up being sold as FOB requirement the spot interest fell away and removed what little hope for improvement in rates that there had been. The price of Fuel itself has been a major driving factor in the direction of the index, which as the Fuel price fell so has the index while ballast bonus decreased driving the index down.

BLNG1g Aus-Japan lost over $2,000 to finish at $50,026, the lowest we have published this year and a fall of nearly $100,000 from the year’s current high. The Pacific basin fared even worse shedding $3,770 for a BLNG3g US-Japan to close at $44,447, a fall of $117,133 from the height of January. While the BLNG2g market remained flat there had been some BFALNG trades that was good to see, so there remains life in the market yet. A small fall closed BLNG2g US-Cont at $41,439.

LPG

The week started quietly with holidays in the Far East and expectation that the fixing would stay quiet. This was the case up till the end of the week when rates and fixing took off. A sharp rise in rates of $3 in one day gave a total gain of $5.215 on the week meaning BLPG1 Ras Tanura -Chiba closed at $78.429, which gave an increase of TCE earnings of just under $7,000 to $62,868 for a round voyage. A vessel fixed in the last week of May was done so at $78 and with cargo outstanding, this will be repeated/improved upon going into next week.

It wasn’t quite as uplifting in the West where markets saw minimal gains. This bearish rate gain was not quite reflected in the amount of cargo being moved though, as brokers reported more than 85 vessels fixed in April alone. This activity coupled with the final destination for nearly three quarters of those fixtures being the Far East has put pressure on tonnage lists and will continue the rise for rates going forward. BLPG3 Houston-Chiba rose a little to close at $132.429, while BLPG2 shifted even less and closed the week 60 cents up at $77 for Houston-Flushing.

Headquartered in London and a subsidiary of the Singapore Exchange (SGX), the Baltic Exchange publishes a range of indices and assessments which provide an accurate and independent benchmark of the cost of transporting commodities and goods by sea. These include the Baltic Dry Index (BDI), the dry bulk shipping industry's best known indicator. Published daily since 1985, this provides a snapshot of the daily spot market earnings of capesize, panamax and supramax vessel types on the world's key trading routes.

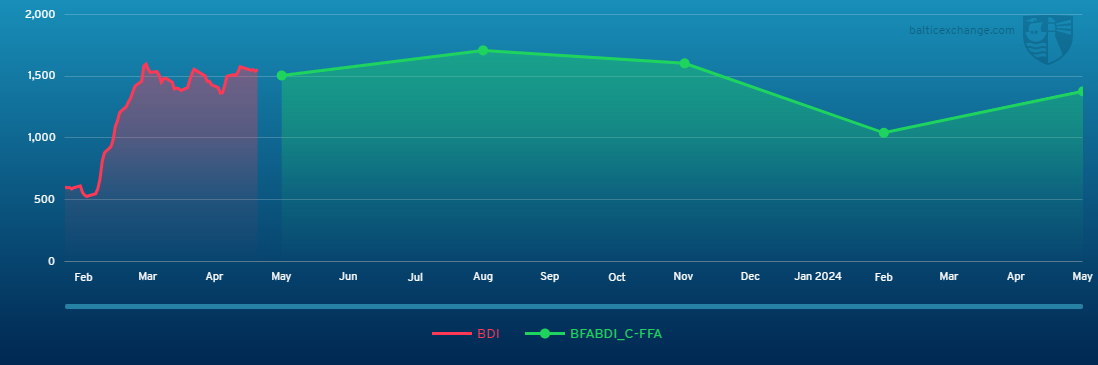

Chart shows Baltic Dry Index (BDI) during May 5, 2022 to May 5, 2023

Baltic Forward Assessment for BDI

In March 2018 the BDI was re-weighted and is published using the following ratios of time charter assessments: 40 percent capesize, 30 percent panamax and 30 percent supramax. The information is provided by a panel of international shipbrokers.

(Source: The Baltic Exchange, edited by Niu Huizhe with Xinhua Silk Road, niuhuizhe@xinhua.org)

A single purchase

A single purchase