BEIJING, April 27 (Xinhua ) -- The Baltic Exchange has added quarterly assessments of the cost of operating crude oil carrying Aframax tankers and clean product carrying Medium Range (MR) tankers to its growing suite of shipping investor tools.

In a news release, the Baltic Exchange introduced that the new service is based on assessments made by independent third-party ship management companies Anglo Eastern, Fleet Management and V-Ships. Using the full suite of independent Baltic Exchange indices, investors are now able to benchmark daily vessel earnings, running costs, sale & purchase and recycling prices. The same vessel descriptions are used across all the datasets.

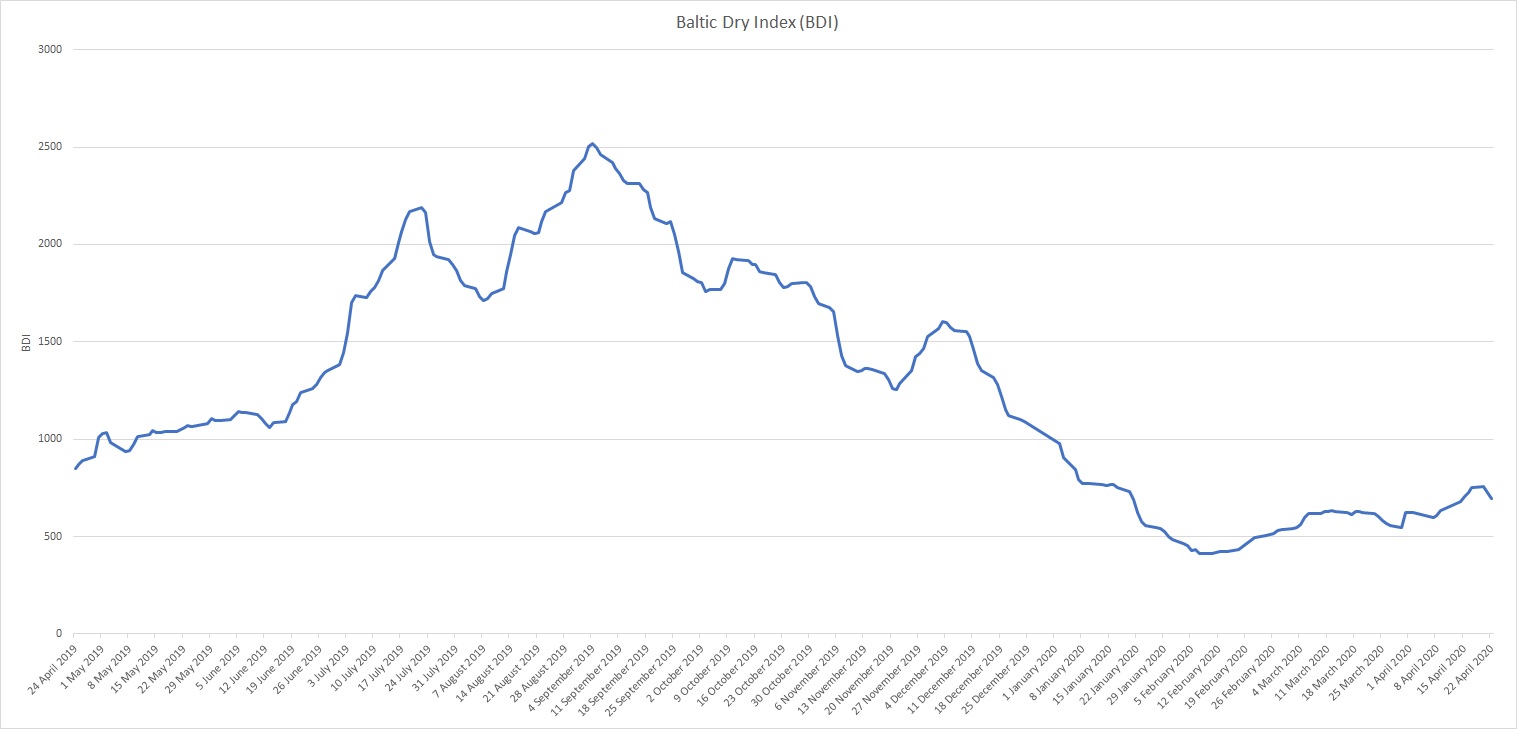

Headquartered in London and a subsidiary of the Singapore Exchange (SGX), the Baltic Exchange publishes a range of indices and assessments which provide an accurate and independent benchmark of the cost of transporting commodities and goods by sea. These include the Baltic Dry Index (BDI), the dry bulk shipping industry’s best known indicator. Published daily since 1985, this provides a snapshot of the daily spot market earnings of Capesize, panamax and supramax vessel types on the world’s key trading routes.

Chart shows Baltic Dry Index (BDI) during Apr.24, 2019 to Apr.22, 2020

In March 2018 the BDI was re-weighted and is published using the following ratios of timecharter assessments: 40 percent capesize, 30 percent panamax and 30 percent supramax. The information is provided by a panel of international shipbrokers.

The Baltic Exchange also publishes weekly report of the dry and tanker markets and below is the weekly report for April 20-24, 2020.

Dry Bulk Report

Capesize

The tide turned this week for the Capesize market, as voyage rates registered dramatically falling fuel costs. This was led primarily by weakness in the energy market, as the global supply of oil continues to mount. US suppliers are finding storage levels are brimming, while being reluctant to turn off the taps. The Capesize 5TC peaked early in the week at $10,081, before gains were gradually eroded down to $8,381 by Friday. Fixture activity was relatively strong throughout the week, with a flurry of cargoes fixing out of Brazil to China across a wide range of dates. West Africa and Eastern Canada to China were also notable on fronthaul activity. The Brazil to China C3, while active, shed over $1.60 to settle down at $10.505. The Pacific had a reasonable flow of trade before petering out on Friday. The West Australia to China C5 settled Friday at $4.073, down $0.84. Along with the oil, Brazilian iron ore forecasts for the 2020 year were revised down by Vale this week. Cashflow troubles were heard out of a Steel maker in India, as Covid-19 continues to wreak havoc on the world markets.

Panamax

The Panamax market had a real directional shift this week, with the Baltic Panamax Index (BPI) veering negative for the first time in over two weeks. East Coast South America grain activity, so often the market driver, has come under pressure this week, with a vast amount of ballasters from Asia compounding the issue. With varying rates being fixed, the mean rate averaging out was at around $8,750 for 82,000dwt, basis delivery Singapore. Elsewhere in the Atlantic, trans-Atlantic demand has failed to deliver again despite some increased activity from North Coast South America. In Asia further falls were witnessed, and despite cargo volume remaining steady week on week, the tonnage count began to build. This counter balanced charterer’s standpoint, and consequently lower bids, with $6,500 being agreed on an 80,000dwt ship for a North Pacific round. Some period deals were agreed. An 82,000dwt ship agreed to $6,100 for the first 55 days, $9,835 thereafter, for seven to nine months. An 81,000dwt vessel achieved $10,000 for 12 months earlier in the week.

Supramax/Ultramax

As the week ended, there was a change in direction from some areas, with vessels in Southeast Asia seeing rates from where they are open rather than absorbing ballast time. Other areas remain finely balanced, but some brokers saw more enquiry from East Coast South America. However, this has yet to be seen on rate values. There was limited activity on the period front. A 58,000dwt vessel open Nantong fixing in the mid $3,000s for the first 30 days, with $7,750 for balance of period up to five months. From the Atlantic, a 63,000dwt ship was fixed for a trip delivery US Gulf, redelivery China, at $13,000. From East Coast South America a 58,000dwt ship fixed a trip to Algeria in the low-mid $6,000s. From Asia, a 58,000dwt vessel was fixed delivery Singapore trip via Indonesia, redelivery West Coast India, at $4,500. From the Indian Ocean, a 53,000dwt vessel fixed for a trip East Coast India, redelivery China, at $5,000 for the first 35 days then balance $7,500.

Handysize

The same trend continued from last week, with limited activity reported from either Basin. There was a minimal gap reported among the four Atlantic and three Pacific routes. From Upriver region, Handysize vessels were competing with bigger sizes as the draft further dropped. East Coast South America coastal trips were reported at the level of $3,000 to $4,000. Inter-Mediterranean trips were at rates in the mid $4,000s. For a mid-large sized delivery in the Black Sea, a trip to the US Gulf paid in the range of $4,000 to $5,000 and slightly higher level for redelivery in the Continent. Otherwise little was reported from the Pacific.

Tanker Market Report

VLCC

The week got off to a slow start, then on Tuesday activity ramped up with an influx of cargoes causing rates to rocket upwards. However, by the end of the week the trajectory was downwards, with heavy pressure being applied.

In the Middle East, 280,000mt to the US Gulf via the Cape to Cape routing is now rated at WS110, having peaked at WS125, this still represents a rise of about 18 points week-on-week. For 270,000mt to China, rates peaked at WS195/197.5 level. They are currently at mid WS160s, again a rise of 15-17.5 points since a week ago. In the 260,000mt West Africa to China market a similar story unfolded, with rates peaking at W177.5/180 level. This was before falling back to mid WS150s, up 15-17.5 points from last week. There was minimal enquiry for the 270,000mt US Gulf to China route and rates are being assessed now at just over $16m. This is a rise from just under $14m last week, with only one notable fixture of a Columbia to China trip at $15.5m.

Suezmax

The market for 130,000mt West Africa to the UK-Continent had a much more adventurous week than in previous weeks. Rates were rapidly firming in the early part of the week, moving 50 points to low WS180s. A mirrored effect took place in the 135,000mt Black Sea to Mediterranean trade, with rates gaining 45 points to mid WS180s. The 140,000mt Basrah to Mediterranean route also gained traction and moved sharply upwards, with rates now at WS155, up 45-47.5 points over the week.

Aframax

A much more positive week in this sector. Rates for 80,000mt Ceyhan to the Mediterranean almost doubled, now being assessed at high WS220s, showing a gain of 120 points. In Northern Europe owners played a waiting game, which worked in their favour. Rates for 80,000mt cross-North Sea are now close to WS240, up 75 points. The 100,000mt Baltic to UK-Continent trade gained about 67 points to WS207.5/210 level. Across the Atlantic the market for 70,000mt Caribbean to the US Gulf has been boosted to WS200, a rise of 75 points. The 70,000mt US Gulf to UK-Continent-Mediterranean performed even better, gaining nearly 80 points to WS187.5-190 level.

Clean

For owners trading in the clean market, it was a phenomenal week in all areas. The market in the Middle East Gulf to Japan trade for 75,000mt started the week with a relatively modest gain of just over 27.5 points to low WS270s. By the end of the week it had risen to WS500, which was reported fixed by Chevron on STI tonnage. The LR1s followed suit, gaining just over 160 points, with last reported done here being on ‘Sunda’ to ATC at WS425. With plenty of enquiry, including period and charterers also looking for storage, the tonnage list was extremely tight. With delays at discharge ports, this was the perfect storm for owners to capitalise, with ships in ballast especially attractive. In the 37,000mt UK-Continent to US Atlantic Coast trade, rates more than doubled, with the market now hovering around WS425, with Baltic to West Africa fixed at WS450. Similarly, rates in the 38,000mt backhaul trade from the US Gulf to UK-Continent firmed from WS112.5 at the start of the week to sit now in the low WS260s. The 30,000mt clean cross-Mediterranean market ended last week in the low WS250s. There are now reports of WS550/575 having been done, with Black Sea to Mediterranean reportedly fixed at WS615.

(Source: The Baltic Exchange, edited by Niu Huizhe with Xinhua Silk Road, niuhuizhe@xinhua.org)

A single purchase

A single purchase