BEIJING, Oct. 9 (Xinhua) -- The Baltic Exchange has published its weekly report of the dry and tanker markets for September 30-October 4, 2024 as below:

Capesize

The Capesize market experienced a steady decline throughout the week, marked by softening conditions across both the Atlantic and Pacific basins. In the Pacific, early week activity from the miners and operators saw some momentum, but as the Golden Week holidays began in Asia, rates quickly weakened, with an increasing tonnage list. The C5 index fell from $11.656 to $10.73 by Friday as miner participation and cargo availability dwindled. The south Brazil and West Africa to China markets remained busy, but there was a noticeable gap between bids and offers, leading to limited fixtures, and continued downward pressure on rates, with the C3 index dropping from $28.17 on Monday to end the week at $27.095. Meanwhile, the north Atlantic market saw intermittent activity, with fronthaul and transatlantic routes softening amid low sentiment. Overall, the market appears to be in a wait-and-see mode, with expectations for activity to pick up next week after Golden Week ends. The BCI 5TC saw a notable drop, ending the week at $26,897, down from $30,258 on Monday.

Panamax

A compelling week for the Panamax market, with limited action in the Atlantic and the North seeing a mid-week mineral push ex US east coast to India and China, but this failed to inject any momentum to an ailing market. Asia was blighted by Golden Week and other Asian holidays, and despite some steady demand ex Australia and NoPac all week, this failed to make any profound impact and the market drifted. Fronthaul highlights included reports of an 82,000dwt delivery Rotterdam trip via US east coast redelivery India at $25,000 whilst in the south an 82,000dwt delivery EC India agreed a rate of $13,250 for a trip via EC South America back to the Far East. In Asia, reports of $13,000 being achieved a few times for NoPac and Australia round trips on index type tonnage delivery China/Japan. Again, a week of limited period activity, however reports emerged of an 82,000dwt type delivery Japan achieving $17,000 for one year.

Ultramax/Supramax

A rather challenging week for the sector with rates in both the Atlantic and Pacific regions facing continued downward pressure. The south Atlantic and US Gulf continued to struggle with a lack of fresh inquiries and a growing tonnage list. A 66,000dwt fixed delivery aps SWP redelivery Türkiye with petcoke at $22,000. Across Continent and Mediterranean, with the overall sentiment being positional, the fixtures surfacing are indicating that rates were hovering around the last done. A 58,000dwt fixed delivery passing Gibraltar via Continent redelivery West Africa at $15,000. The Pacific market also remained under pressure, with rates generally dipping below from previous levels across the region. A 54,000dwt open north China was fixed trip to Indonesia with steel at $15,000.

In the period market, a 63,000dwt open Qingdao fixed for 12 months at $16,000. Meanwhile, a 56,000dwt open Dalian fixed for 3-5 months at $17,000 and 63,000dwt open Yeosu was reported fixed for 4-7 months WW at $15,000.

Handysize

Generally, the market has seen a mixed affair this week. The Continent and Mediterranean markets have seen more support, with a noticeable pick-up in fresh demand and cargo coverage. A 40,000dwt open Bejaia 1/2 Oct reported fixed delivery passing Canakkale redelivery US Gulf at $11,500. In contrast, the south Atlantic and US Gulf continued to be a tough environment for owners, with negative sentiment prevailing and few favourable options available. A 38,000dwt open Rio Grande 27 Sep fixed delivery APS Imbituba for a trip to UK / Continent with sugar at $13,000. Pacific market remained relatively balanced despite the usual disruptions from holidays and a shrinking cargo book. A 28,000dwt open Philippines fixed via SE Asia to Indonesia at around $11,000. On the period side, a 40,000dwt open Japan was placed on subjects for short period in the high $15,000.

Clean

LR2

LR's in the MEG were back to being subjected to downward pressure this week, taking them back to around the same level as a fortnight ago. TC1 sunk 26.39 points, taking the index to WS120.28 and, for a run west on TC20, the index settled down $374,447 to $4.22 million.

West of Suez, Mediterranean/East LR2's on TC15 remained flat at around the $3 million mark, with the market seemingly dormant this week.

LR1

In the MEG, LR1's also took a relatively steep downturn this week. A TC5 index run 55kt CPP AG/Japan was marked 23.44 points lower than this time last week and the Baltic TCE round trip dipped below $20,000/day. For a voyage west on TC8, the index came off by around 12% to $3.63 million.

On the UK-Continent, the TC16 market stayed relatively level seen in the index, bubbling around the WS110 mark or thereabouts.

MR

MEG MR's have managed to hold on this week and not be too affected by the larger sizes in the region. The TC17 index, as a result, was assessed a modest 4.99 points lower than this time last week to WS178.58.

UK-Continent MR's looked to have reached a floor this week and even began signs of recuperating. TC2 bottomed out at WS87.97 mid-week and is now back at WS90.31 and TC19 followed suit plateauing at WS107.43 and is now marked at WS115.94.

USG MR's resurged leaps and bounds this week. TC14 went from WS117.5 to WS184.64 with the Baltic TCE for the trip shooting from $9,811/day to $22,760/day. TC18 followed this and is currently assessed at WS236.43 (up WS67.14). For a trip down to the Caribbean on TC21, we saw the index add 93% to its value from this time last week to $912,143 where it currently resides.

The MR Atlantic Triangulation Basket TCE gained $11,146 to $27,065.

Handymax

In the Mediterranean, Handymax's came down a tick to WS94.44 (-8.06). Up on the UK-Continent, the TC23 shed 14.17 points to WS109.44.

VLCC

The VLCC market rose this week despite, or because of, the Golden Week holiday in the Far East. The 270,000 mt Middle East Gulf to China trip climbed four points to WS57.80, which gives a daily round-trip TCE of $36,359 basis the Baltic Exchange's vessel description.

In the Atlantic market, the rate for 260,000mt West Africa/China also saw a gain of four points to WS61.83 (corresponding to a round voyage TCE of $41,077/day), whilst the rate for 270,000 mt US Gulf/China ascended by $312,500 to $8,172,500 (a daily round trip TCE of $40,234).

Suezmax

Suezmax rates clawed back recent rate reductions, and some, this week. In West Africa, the 130,000 mt Nigeria/UK Continent voyage claimed a 28-point recovery to WS103.44, or a 38.5% increase (a daily round-trip TCE of $40,850). The TD27 route (Guyana to UK Continent basis 130,000mt), which has now moved from public trial to live reporting, was assessed even stronger than West Africa at WS107.78, up 33 points (+45%) week-on-week, which translates into a daily round trip TCE of $43,305 basis discharge in Rotterdam. In the Mediterranean and Black Sea region, the rate for 135,000mt CPC/Med had 12 points added to WS96.80 (showing a daily TCE of $31,404 round-trip). In the Middle East, the rate for 140,000 mt Middle East Gulf to the Mediterranean (via the Suez Canal) gained five points to just break through the WS100 level.

Aframax

In the North Sea, the rate for the 80,000 mt Cross-UK Continent rose 14 points to almost WS130 (translating to a daily round-trip TCE of almost $32,000 basis Hound Point to Wilhelmshaven). There was a report of WS135 being on subjects, but no further details were available at the time of writing.

In the Mediterranean market, the rate for 80,000 mt Cross-Mediterranean recovered recent losses, moving up from the WS110 level to close to WS145 (basis Ceyhan to Lavera that shows a daily round trip TCE of about $37,200).

Across the Atlantic, owners picked themselves up, dusted themselves down and shifted the market into a higher gear on Wednesday, which continued through Thursday. Rates surpassed rises of over 150% for the shorter hauls, with TCE gains further remarkable. The 70,000 mt east coast Mexico/US Gulf (TD26) route dramatically increased by 135 points to WS221.25 while the 70,000 mt Covenas/US Gulf (TD9) route is being assessed at a comparable WS218.13, up 132.5 points showing a round-trip TCE of $65,460 (+890%) and $57,782 (+683%) per day, respectively. The rate for the transatlantic route of 70,000 mt US Gulf/UK Continent (TD25) rose only 119 points to WS220 (a round trip TCE basis Houston/Rotterdam of $57,850/day, +248%).

LNG

We are very much in the winter season for LNG, although if you were to look at the spot freight rates you would not be able to tell. With muted enquiry and only a couple of requirements on either side of the canal, there is not much to report back. All three routes have lost value this week. In the East of Suez arena a few questions ex-Australia is the only reported enquiry dragging the rate down for BLNG1/BLNG1-174 from $48,300/$65,100 to $44,700/$61,100, while in the Atlantic a few traders and utilities are looking for November tonnage but not sufficient enough to prevent the rate slide on BLNG2/BLNG2-174 from $42,600/$56,400 to $39,500/$52,000. The trans-Panama route (BLNG3/BLNG3-174) suffered the same fate, dropping from $58,000/$76,199 to $52,000/$69,000.

Continuing lack of interest on period has kept the rates falling for all three periods. Our multi-month charter came off $2,950, closing at $68,200 while one-year charter rates fell by $1,250 to $76,250 while the three-year term came off $250 to $80,400.

LPG

It does not take much for the LPG market to change, and the winds of change hit hard and fast this week. BLPG1 Ras Tanura-Chiba is up 47.65%, which is one of the greatest jumps on the route for a long time. With a rise of $32.916, the index closed at $69.083, which pushed earnings on the TCE up by $34,359 a 67.29% and a close of $51,059. The rates initially dragged up by the activity in the US found its own feet, fixing high with reports of a cargo working in the high $70's.

Across the Atlantic, the market was busy, with several early cargoes coming out, pushing the rates up and many charterers who had been taking their time came out with stems that fueled the fire and pushed the levels even higher. BLPG3 Houston-Chiba gained $39.5 (31.14%) closing well above the triple digits at $126.833, which had a corresponding TCE earning of $56,920, which was up 53.34% or $30,363. BLPG2 though quiet in actual fixtures still gained moving up $20 (30.3%) closing at $66 and a TCE earning equivalent of $68,685.

Headquartered in London and a subsidiary of the Singapore Exchange (SGX), the Baltic Exchange publishes a range of indices and assessments which provide an accurate and independent benchmark of the cost of transporting commodities and goods by sea. These include the Baltic Dry Index (BDI), the dry bulk shipping industry's best known indicator. Published daily since 1985, this provides a snapshot of the daily spot market earnings of capesize, panamax and supramax vessel types on the world's key trading routes.

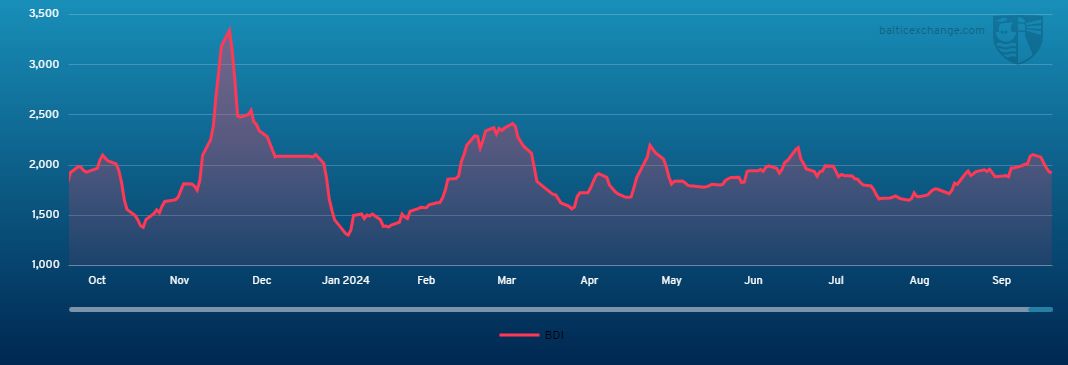

Chart shows Baltic Dry Index (BDI) during Oct. 6, 2023 to Oct. 4, 2024

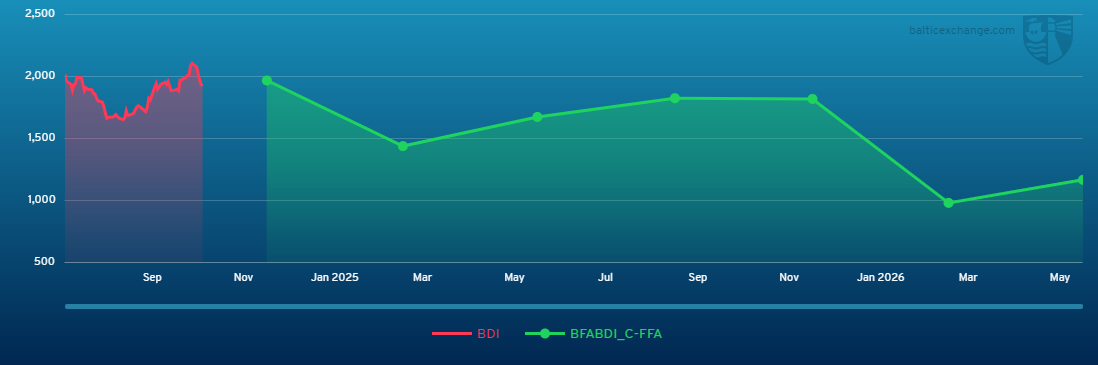

Baltic Forward Assessment for BDI

In March 2018 the BDI was re-weighted and is published using the following ratios of time charter assessments: 40 percent capesize, 30 percent panamax and 30 percent supramax. The information is provided by a panel of international shipbrokers.

(Source: The Baltic Exchange, edited by Niu Huizhe with Xinhua Silk Road, niuhuizhe@xinhua.org)

A single purchase

A single purchase