BEIJING, March 18 (Xinhua) -- The Baltic Exchange has published its weekly report of the dry and tanker markets for March 11-15, 2024 as below:

Capesize

The week started positively for the capes, especially in the Pacific, where rates saw a slight increase. However, Tuesday brought a downturn in the Pacific market, with fixtures dropping significantly by $1.50 from west Australia to China. This drop was attributed to increased competition from older vessels and a pessimistic FFA market. Consequently, the C5 index declined by $1.41 to reach $13.125. This downward trend continued as the week progressed, with more pressure in the Pacific market due to a growing tonnage list and shortage of coal cargoes. The negative FFA market also exerted pressure from south Brazil and West Africa to the Far East, leading Charterers to swiftly lower their bids. Sentiment in the north Atlantic weakened for trans-Atlantic business, although the fronthaul market displayed resilience. A notable fixture was reported from east coast Canada to the Far East, leading to a $1,813 increase in the C9 index, reaching $58,688. Towards the end of the week, activity picked up in the Atlantic. Brokers reported that a major player had quietly entered the market and fixed a handful of vessels from south Brazil to China for the first half of April. Overall, it's been a turbulent week, with the BCI 5TC shifting direction daily, and ultimately closing down $189 at $33,332.

Panamax

The Panamax market erupted into life midweek with rates improving as a strong push from both South and North America led the drive. The period market remained robust, and a raft of deals were concluded at stronger levels, notably a new build 82,000dwt delivery China achieving $21,000 for one year’s employment. In the Atlantic, the week began on a firm note against a tight tonnage count in the North. With both strong mineral and grain-led demand, Charterers scrambled to hit the offers where owners were willing to stand still, $31,500 rumored fixed on an 81,000dwt delivery north Spain for a trip via NC South America redelivery the Far East seemingly the highlight. Midweek witnessed a binge of fixing from EC South America and this in turn gave additional support to the Asia market that, up until that point, had been relatively flat all week with limited rates nudging up slightly on the week.

Ultramax/Supramax

A change in direction during the week as the recent positive momentum seen from Asia was seemingly being eroded with lower fresh enquiry and a slight build-up of prompt tonnage. However, the Atlantic side saw a slightly more positive feel return with more activity. More enquiry was seen from the south Atlantic and sources spoke of a tightening tonnage supply. From the Atlantic, a 61,000dwt was heard to have fixed a trip from West Africa to China at $28,000. Elsewhere a 63,000dwt open Ghent fixed a scrap run to the east Mediterranean at $17,000. From Asia, a 56,000dwt open south China fixed a trip via Indonesia redelivery China in the mid $13,000s. As the week came to close many felt that the Indian Ocean was picking up again, a 56,000dwt open Arabian Gulf was heard to have fixed a trip to Chittagong in the mid $18,000s.

Handysize

A general feeling of positivity across the Atlantic saw levels make slow but steady gains, in the south Atlantic a 36,000dwt in ballast from west coast South America was rumored to have been placed on subjects for a trip from Recalada to Morocco at $19,000 with further improvements expected for Owners. In the US Gulf, more activity was seen with a 42,000dwt rumored to have been fixed from Panama City to the UK-Continent with wood pellets at $11,000 whilst a 38,000dwt fixed from NC South America to the Continent with an intended cargo of metcoke at $12,000. More activity was also seen on the Continent with a 40,000dwt fixing from Rouen to Vera Cruz at $18,000. In the Mediterranean, a 34,000dwt fixed from Otranto via the eastern Mediterranean to the US Gulf at $13,000. Activity in Asia has been muted, however, enquiry levels have been said to show signs of improvement and pockets of positivity have begun to emerge.

Clean

LR2

LR2 freight levels resurged with gusto this week. The rate for 75kt MEG/Japan drove up 121 points to WS277.78. The 90kt MEG/UK-Continent TC20 trip similarly climbed aggressively to the tune of $1.98 million and is currently pegged at $6.61 million.

West of Suez, Mediterranean/East LR2 freight dropped again this week losing ultimately $266,000 to $4.22 million it looks to have bottomed out mid-week at $4.1 million.

LR1

In the MEG, LR1 freight also turned sharply upwards this week. The 55kt MEG/Japan index of TC5 added 60% to its value to currently rest at WS283.15. The 65kt MEG/UK-Continent of TC8 also went from $3.98 million to $5.40 million

On the UK-Continent, the 60kt ARA/West Africa was assisted upwards by the movement in the MEG, the TC16 index improved 19.37 points to WS196.25.

MR

MR’s in the MEG were a little slow to react to firming in the region on other sizes but are now catching up. TC17 35kt MEG/East Africa hopped up 21.78 points to WS352.14 taking the Baltic round trip TCE for the run back up over the $40,000 per day. Up in the UK-Continent MR’s firmly improved from steady enquiry. The 37kt ARA/US-Atlantic coast of TC2 index shot up from WS192.22 to WS230.56. On a TC19 run (37kt ARA/West Africa) the index also went from WS216.25 to WS253.75. What goes up must come down was the story for the USG MR's this week. TC14 (38kt US-Gulf/UK-Continent) came off 52.86 points to WS180.71. The 38kt US Gulf/Brazil on TC18 also shed 42.14 points at WS282.86. The 38kt US-Gulf/Caribbean TC21 dropped by $300,000 to $885,714.

Handymax

In the Mediterranean, Handymax’s remained resolute and the TC6 index stayed again at WS320 all week.

Up in north west Europe, the TC23 30kt Cross UK-Continent managed to reach WS250 (+7.78).

VLCC

The market saw refreshed confidence this week assisted by April liftings. The rate for the 270,000 mt Middle East Gulf to China climbed to WS71.95 up from WS69.14 and corresponds to a daily round-trip TCE of $49,737 basis the Baltic Exchange’s vessel description.

In the Atlantic market, the 260,000 mt West Africa/China route demonstrated a similar movement upward, climbing 3.2 points to WS74.25 which gives a round voyage TCE of $52,725 per day. The rate for 270,000 mt US Gulf/China dipped to around $8.88 million early in the week with some fixtures reported at this level it has since then returned up to $9.03 million providing a round-trip daily TCE of $44,697.

Suezmax

Suezmaxes in West Africa dropped incrementally from WS106.23 to WS102.41 for the 130,000 mt Nigeria/UK Continent trip (a daily round-trip TCE of $37,700). In the Mediterranean and Black Sea region the rate for 135,000 mt CPC/Med held flat around the WS106-107 level (showing a daily TCE of $36,700 round-trip). In the Middle East, the rate for 140,000 mt Middle East Gulf to the Mediterranean (via the Suez Canal) shaved off a meagre 2.17 points to WS96.22 basis routing via the Suez Canal.

Aframax

In the North Sea, the rate for the 80,000 mt Cross-UK Continent hopped up 7.5 points to WS133 (showing a round-trip daily TCE of around $33,828 basis Hound Point to Wilhelmshaven).

In the Mediterranean market the rate for 80,000 mt Cross-Mediterranean continued its upward track to the tune of 22 points this week to WS174.56 (basis Ceyhan to Lavera, that shows a daily round trip TCE of just over $50,500).

Over the Atlantic, the US Gulf market took a downturn this week. The rate for 70,000 mt east coast Mexico/US Gulf (TD26) dropped 5.32 points WS175.31 (a daily TCE of $40,920 round trip) while the rate for 70,000 mt Covenas/US Gulf (TD9) came off 4.68 points to WS170.63 (a round-trip TCE of $36,742 per day). The rate for the trans-Atlantic route of 70,000 mt US Gulf/UK Continent (TD25) had 20 points chopped off it to the WS180.63 level (a round trip TCE basis Houston/Rotterdam of approximately $41,692 per day).

LNG

It is another week of little spot fixing in the LNG market, both the Atlantic and Pacific have seen some tentative enquiries but with these either delaying or being fixed on quietly, the material difference to spot rates is negligible. On the Aus-Japan BLNG1 route both the 160cbm and 174cbm shed a few dollars to finish down at $33,897, and $51,265 respectively; constructs for these deals are being assessed both as Ballast Bonus to Hub and Roundtrip. While the Atlantic held more enquiry a stable and unchanged tonnage list didn’t drive prices up particularly, this could be some small hangover from the US governments pause on new FTA requests, but it’s more likely down to a continued shutdown in Freeports train 3 which enters its 7th week and overall market bearishness.

Rates for BLNG2 US-Continent gained modestly with the 174cbm BLNG2 run moving up to $51,697 a gain of $1,000, while the 160cbm moved less up $497 to $38,989. BLNG3 US-Japan fared better with greater increases (but in LNG freight market circles, still very flat) up $1,991 for the 174cbm while the 160cbm gained $1,400, these closed at $56,464 and $44,391 respectively. The deal constructed for Atlantic basin are being assessed on a Round Trip basis.

The period market floundered significantly for a three year period losing $10,400 down to $79,700 while one year deals moved down to $78,700 and the six month period lost $3,700 to finish at $58,800.

LPG

The LPG market has made a pretty miraculous turnaround this week we are seeing levels fixed not seen since early January before the “big fall”. The AG market is awash with potential ships available for early April while the US market has a fair amount of uncertainty remaining around ship itineraries. In any case, rates have bolstered significantly for BLPG1 Ras Tanura-Chiba where an increase of $15.428 has put us back on track with a closing price of $78.857 and a daily TCE earning equivalent of $59,825.

The Atlantic market was very busy with many fixtures reported and every day improving bids/offers pushed the index up. With BLPG3 Houston-Chiba rising by $19.571 throughout the week and a close of $137.714, levels fixed that have not been seen since early January. The BLPG2 Houston-Flushing gained a comparably modest $10.8 closing at $77 but it is still not to be sniffed at. Both routes TCE earnings gained close to $16,000 PD and finished at $81,160 and $60,390 for BLPG2 and BLPG3 respectively.

Headquartered in London and a subsidiary of the Singapore Exchange (SGX), the Baltic Exchange publishes a range of indices and assessments which provide an accurate and independent benchmark of the cost of transporting commodities and goods by sea. These include the Baltic Dry Index (BDI), the dry bulk shipping industry's best known indicator. Published daily since 1985, this provides a snapshot of the daily spot market earnings of capesize, panamax and supramax vessel types on the world's key trading routes.

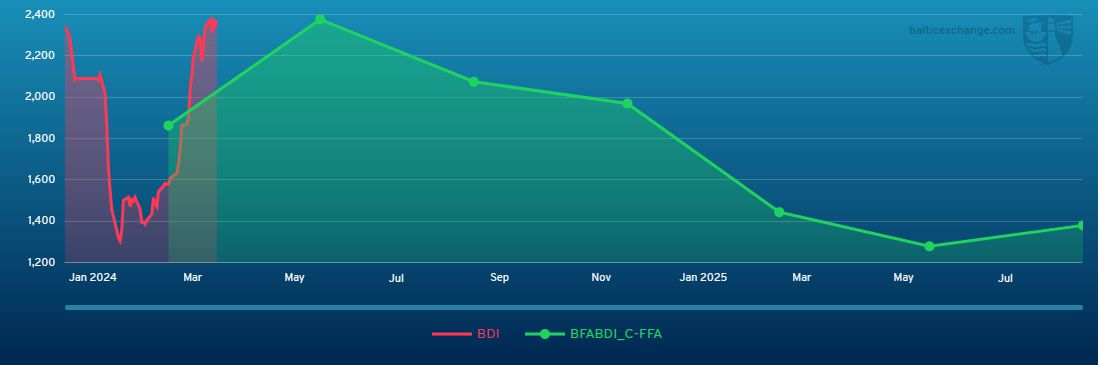

Chart shows Baltic Dry Index (BDI) during March 17, 2023 to March 15, 2024

Baltic Forward Assessment for BDI

In March 2018 the BDI was re-weighted and is published using the following ratios of time charter assessments: 40 percent capesize, 30 percent panamax and 30 percent supramax. The information is provided by a panel of international shipbrokers.

(Source: The Baltic Exchange, edited by Niu Huizhe with Xinhua Silk Road, niuhuizhe@xinhua.org)

A single purchase

A single purchase