BEIJING, Dec. 11 (Xinhua) -- The Baltic Exchange has published its weekly report of the dry and tanker markets for December 4-8, 2023 as below:

Capesize

The Capesize market faced a challenging week characterised by significant fluctuations. The week began positively with a robust increase in the BCI 5TC, reaching $54,584, driven by active engagement in the Pacific. However, profit-taking in the FFA market late on Tuesday triggered unease, leading to a decline in rates. Throughout the week, the Cape market experienced a downward trend, with the BCI 5TC dropping to $34,854 by Thursday, reflecting a substantial decline. The Pacific market remained sluggish, marked by a persistent lack of major players on C5, contributing to a negative sentiment. South Brazil and West Africa to the Far East sustained pressure throughout the week as the bid-to-offer gap widened, compelling owners to pursue aggressively. Despite earlier optimism, the north Atlantic did not tighten as expected, with C8 and C9 experiencing significant drops towards the end of the week. As the week draws to a close, there has been an increase in Pacific activity, leading to a rise in rates on C5 by 50 cents to a $1.00. Additionally, in the Atlantic, from south Brazil to West Africa to the Far East, a stabilisation in rates has been observed, prompting a shift in sentiment. Overall, the Capesize market faced challenges, highlighting the volatility of the sector. The BCI 5TC rose $466 to finish the week at $35,320.

Panamax

It proved to be a tumultuous week in the Panamax market, with the stronger optimism seen last week carrying over to the early part of this week, although this dramatically eroded away with the week ending on a far weaker tone. In the Atlantic, short front-haul trips ex US east coast to India contracted throughout, with $38,000, and $26,500 reported fixed on this run, albeit on two contrasting types, providing a good indicator of the market trend on all routes. Asia also saw further erosion in rates despite solid levels of demand in most loading origins, but the weaker sentiment emanating from the Atlantic basin impacted confidence here as well, with tonnage count slowly building. About $21,000 concluded early on an 82,000dwt delivery China for a NoPac round trip, with deals for similar trips now concluding at closer to $18,500 as momentum switched back firmly in charterers favour.

Ultramax/Supramax

A rather patchy week after the recent strength in the sector as the week saw a change in direction. That said, it was described as positional. In the Atlantic, rates remained healthy with a good amount or fresh enquiry in the north, although south Atlantic demand slowed as the week ended. In Asia, similarly the recent positive sentiment wavered, brokers saying that enquiry levels had eased across the region. In the Indian Ocean, enquiry levels remained fairly healthy and the market was seen as finely balanced. Period activity was limited but a 63,000dwt open Philippines fixed a short period at around $16,000. In the Atlantic, a 63,000dwt was heard fixed in the mid $17,000s plus mid $700,000s ballast bonus basis delivery Santos for a fronthaul. Whilst a 56,000dwt fixed a trip from Spain to the US east coast at $18,000. From Asia, a 58,000dwt open Malaysia fixed a trip via Indonesia redelivery China at $15,500. Further north, a 56,000dwt fixed delivery mid-China for an Indonesian round voyage at $12,000.

Handysize

Positivity grew across the sector as tonnage availability remained limited. In the US Gulf, a 35,000dwt opening in Tuxpan fixed from SW Pass to the eastern Mediterranean in the mid $20,000s. The south Atlantic also saw further gains as a 37,000dwt fixed from Itaqui for mid-December dates for a trip to the Baltic at $27,650. Whilst an unnamed large handy was rumoured to have been fixed for a trip from Recalada to the western Mediterranean at $26,000. In the eastern Mediterranean, activity remained high as a 36,000dwt fixed from Diliskelsi via Alexandria to Houston with an intended cargo of steels at $15,000. The continent was also strong with a 37,000dwt opening in Riga fixing for a trip to West Africa at $30,000. Small gains were seen in the Pacific as a 28,000dwt fixed from Japan to Southeast Asia at $10,000 and in west coast South America, a 35,000dwt was fixed for a trip to Singapore-Japan at $21,000.

Clean

LR2

LRs in the MEG saw activity levels pick up this week and freight resurged optimistically. The 75Kt MEG/Japan TC1 index gained 19.17 points to end up at WS130.56. The 90kt MEG/UK-Continent TC20 run to the UK-Continent also climbed $375,000 to $3.56m.

West of Suez, Mediterranean/East LR2’s on TC15 held resolute at $3.4m all week and the TCE hovered over the $10,000/day Baltic round trip at time of writing.

LR1

In the MEG, LR1s also saw a welcome uptick in their value this week similar to their larger siblings. The 55kt MEG/Japan index hopped up 11.87 points to WS130.31 and the 65kt MEG/UK-Continent of TC8 climbed $46,800 to $2.82m.

On the UK-Continent, the 60Kt ARA/West Africa TC16 index just dipped from WS205.63 to WS198.44. The Baltic round trip TCE for the run is still just under $45,000/day at these levels.

MR

MRs in the MEG recharged after having been on the ropes last week. TC17 pumped up 59.64 points to WS243.93 with the Baltic TCE for the run climbing by 75% to $27,588/day round trip.

UK-Continent MRs took a downturn this week, with some attributing celebrations of the season in London as a factor. The 37kt ARA/US-Atlantic coast of TC2 dipped from WS211.25 to WS193.75. On a TC19 run (37kt ARA/West Africa) the index, by comparison, lost just five points to WS232.81. Baltic round trip TCEs for the runs are now $24,200/day and $33,100/day, respectively.

The USG MRs have seen continued action this week with plenty of open enquiry and the available tonnage in a state of flux. TC14 (38kt US-Gulf/UK-Continent) danced around a little but ultimately added 9.64 points to currently be marked at WS268.93. The 38kt US Gulf/Brazil on TC18 was a bit more assured in its direction and the index went from WS350.71 to WS377.86. A 38kt US-Gulf/Caribbean TC21 trip stepped up from $1.74m to $1.81m.

The MR Atlantic Triangulation Basket TCE ultimately climbed from $57,821 to $58,239.

Handymax

In the Mediterranean, Handymax’s have stabilised this week at WS265 with demand and supply balanced for the moment.

Up in northwest Europe, the TC23 30kt Cross UK-Continent ticked up for the second week in a row, adding 23.33 points to WS213.61.

VLCC

The market has been relatively flat this week, with rates from the Middle East sideways, and slightly softer in the Atlantic. For the 270,000 mt Middle East Gulf to China route, the value is unchanged at WS66.5, which corresponds to a daily round-trip TCE of just over $48,747 basis the Baltic Exchange’s vessel description, although this is actually about $3,000/day greater than a week ago. The 280,000 mt Middle East Gulf to US Gulf trip (via the cape/cape routing) is still assessed around the WS35-36 level.

In the Atlantic market, the rate for 260,000 mt West Africa/China is now a point off from last Friday’s number at WS66.4 (which shows a round voyage TCE of $49,961/day, about a $1,500/day increase from a week ago), while the rate for 270,000 mt US Gulf/China fell $188,889 to $9,511,111 ($44,290/day round trip TCE, an increase of over $1,000/day), while overnight there are reports of a traders relet on subjects to another trader at $9,350,000.

Suezmax

Suezmaxes in West Africa firmed a little this week with assessments for 130,000 mt Nigeria/UK Continent route climbed four points to WS102.73 (a daily round-trip TCE of $41,010). In the Mediterranean and Black Sea region, the 135,000 mt CPC/Med route rose one point to WS137.5 (showing a daily TCE of $65,723 round-trip). In the Middle East, the rate for 140,000 mt Middle East Gulf to the Mediterranean dropped a point to WS67.

Aframax

In the North Sea, the rate for the 80,000 mt Cross-UK Continent route slipped about 2.5 points to WS142.14 (showing a round-trip daily TCE of $45,996 basis Hound Point to Wilhelmshaven). In the Mediterranean market the rate for 80,000 mt Cross-Mediterranean dropped 12 points to WS136 (basis Ceyhan to Lavera, that shows a daily round trip TCE of $35,745).

On the other side of the Atlantic, the market has continued in a downward direction. The rate for 70,000 mt east coast Mexico/US Gulf (TD26) has fallen 40 points to WS138.13 (a daily round-trip TCE of $29,543) and the 70,000 mt Covenas/US Gulf rate has shed 32 points to WS134.38 (a round-trip TCE of $27,359/day). The rate for the trans-Atlantic route of 70,000 mt US Gulf/UK Continent has been weakened by 17 points to WS159.06 (a round trip TCE basis Houston/Rotterdam of $38,597/day).

LNG

BLNG1g Australia-Japan again fell this week shedding $29,023 to close at $113,975. This level has been seen a few times in the last year but we haven’t been lower since mid-August and prior to that January. The fall came despite a fair amount of activity in the East, a few ships fixed ex-Aus one 2-stroke in the region of $140,000/day, while a TFDE was fixed closer to $100,000. Other bits of enquiry has kept the market talking and, though rates have been hit, there is life that most brokers have agreed is a good sign.

The US export market has been hit with continued issues with the Panama Canal making Asian LNG prices more tempting than in the Atlantic, and Christmas, which is also in full force for those returning from the conference in Athens last week. With many brokers and market players out in droves celebrating the festive period, it has kept market activity down. BLNG2g Houston-CONT lost $18,921 to finish at $141,328 while BLNG3g Houston-Japan fell to a close of $145,141. The LNG period assessment fell again week-on-week to $85,000 for six months, $96,900 for one year, and $104,200 for three-year-term deals.

LPG

A quiet week for the BLPG1 Ras Tanura-Chiba route, the index fell by $23 to close at $125.286. The significant drop comes mainly from the lack of activity, with few enquiries and ships failing subjects with cargoes being taken back internally, it has resulted in rates significantly weakened compared to a few weeks ago. There isn’t much left of 2023 but optimism hasn’t quite died out yet with brokers feeling there could be some life before we celebrate the New Year.

With the continued essential closure (and no sign of it being let up) for ships to route via the Panama Canal, ships are almost exclusively going via the Suez. This has hit rates quite a lot, with a drop of $22.857 pushing the index below $200 for the first time since the end of October. Publishing at $198.286 for BLPG3 Houston-Chiba, we have a daily TCE earning of $115,935. BLPG2 Houston-Flushing suffered a similar blow but losing the least of the three routes at $13.6 as we closed at $109.8 and a daily TCE earning of $130,681.

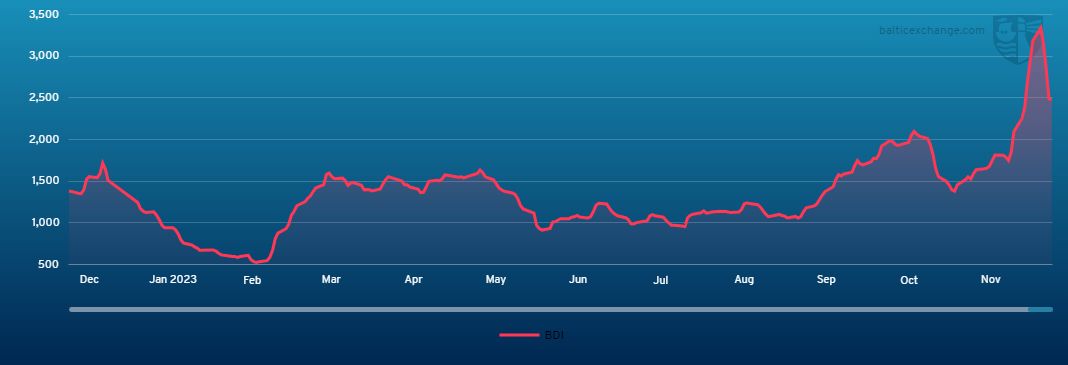

Headquartered in London and a subsidiary of the Singapore Exchange (SGX), the Baltic Exchange publishes a range of indices and assessments which provide an accurate and independent benchmark of the cost of transporting commodities and goods by sea. These include the Baltic Dry Index (BDI), the dry bulk shipping industry's best known indicator. Published daily since 1985, this provides a snapshot of the daily spot market earnings of capesize, panamax and supramax vessel types on the world's key trading routes.

Chart shows Baltic Dry Index (BDI) during Dec. 9, 2022 to Dec. 8, 2023

Baltic Forward Assessment for BDI

In March 2018 the BDI was re-weighted and is published using the following ratios of time charter assessments: 40 percent capesize, 30 percent panamax and 30 percent supramax. The information is provided by a panel of international shipbrokers.

(Source: The Baltic Exchange, edited by Niu Huizhe with Xinhua Silk Road, niuhuizhe@xinhua.org)

A single purchase

A single purchase