BEIJING, May 4 (Xinhua) -- The Baltic Exchange has published its weekly report of the dry and tanker markets for April 24-28, 2023 as below:

Capesize

After the surge of activity in the middle of the week, the Capesize market calmed on Friday to welcome the long weekend approaching in most of the countries in both basins. The time charter average settled at $19,080, rising $2,810 week-on-week. The Brazil to China and west Australia to China both further improved compared with the beginning of the week, to $22.728 and $9.043 respectively. The backhaul route also finally came back to positive territory after a long wandering in the negative. In the North Atlantic, there was talk of tonnage supply tightening. On the period front, the Boston (177,827 2007) delivery Zhenjiang 4/14 May was fixed for 14/17 months at $17,000.

Panamax

Overall, the Panamax market returned a lacklustre week. The North Atlantic market looked tonnage heavy from the get-go, with Transatlantic trips few and far between. The front haul trips saw decent demand overall with rates easing only slightly. An 82,000dwt delivery Gibraltar fixed midweek a fronthaul trip via NC South America redelivery Singapore-Japan at $24,500. However, the mean average rate for route P2A on the week hovered just below this. Asia, by contrast, had limited support on some of the longer round trips. However, route P3A lost ground only slightly week-on-week. Rates on the shorter Indonesian round trips held steady week-on-week with reports of various 76,000dwt types giving delivery China rates around the $12,000 mark for the Indonesian coal rounds. Period news was mostly thin. There were several reports of various 82,000dwt tonnage agreeing rates of between $17,500 and $17,750 for short period up to one year.

Ultramax/Supramax

A rather positional week overall for the sector. Whilst the Atlantic at the beginning of the week remained optimistic as it progressed, lower demand was seen from the US Gulf which led to a lower rate of expectations. The South Atlantic had reasonable volume - although again this seemed to be waning. With the upcoming widespread holiday, it was unsettled in the Asian arena with owners looking to take a discount before the holiday period. Limited fresh enquiry from Indonesia didn't help overall sentiment. In the Atlantic, a 55,000dwt was fixed delivery US Gulf for trip to South Korea with petcoke at $23,00. Elsewhere, a 56,000dwt fixed a scrap run from the North Continent to the East Mediterranean in the upper $18,000s. From Asia, a Supramax open South China fixed a trip via Philippines redelivery China with nickel ore at $11,500. More action surfaced from the Indian Ocean, with a 53,000dwt open Kuwait fixing a trip via Salalah to Southeast Asia around $9,500 - $10,000.

Handysize

With Holidays looming, it was also a lacklustre week of activity across the Asia Markets which saw levels soften. A 38,000dwt open in Newcastle was fixed for a trip via Eastern Australia to China with an intended cargo of grains at $14,500. Meanwhile, a 38,000dwt open in Koh Si Chang was fixed via Western Australia to China with concentrates at $9,500. A 37,000dwt open in South Korea was fixed for two laden legs at $15,000. The Atlantic had showed some signs of continued positivity, but activity had reduced in East Coast South America after a recent spike. A 37,000dwt was rumoured to have been fixed for a trip from Mucuripe to Singapore-Japan range at $19,500. The US Gulf had remained buoyant with a 38,000dwt fixing from Havana via Cape Henry to Venezuela at $14,000. A 37,000dwt open in Bejaia with end of April dates was fixed for a short period in the region of $15,000.

Clean

LR2

LR2s in the MEG this week have been relatively subdued. TC1 has remained resolute in the WS180 region. TC20 has shed $107,143 leaving the index currently marked at $4,507,143.

West of Suez, Mediterranean/East LR2s have also declined this week (circa $91,000) after a widely reported fixture at $4,350,000 led the index to $3,491,667.

LR1

In the MEG, LR1s have been keeping by this week. As a result TC5 has held in the high WS190s – WS200 range and for a trip West TC8 has hopped up from $3,580,000 to $3,840,000. This took the round trip TCE up into the low $40,000’s /day. On the UK-Continent, TC16 suffered from inactivity this week and the index dropped from WS194.29 to WS158.57.

MR

MEG MRs have been consistently marked down this week. The TC17 index has hemorrhaged 58.57 points in total bringing it to currently rest at WS232.14.

On the UK-Continent a surplus of vessels has driven weak sentiment this week. Subsequently, TC2 and TC19 have both seen substantial declines in freight levels. TC2 is currently pegged at WS142.78 (-65.55) and TC19 is marked at WS153.57 (-65). This has taken a circa 50% chunk out round-trip TCEs for the runs which are now in the $13,000-16,000 /day range.

Over in the Americas, the MRs have been similarly affected to those on the UK-Continent. TC14 has shed 22.5 points to WS90 and TC18 has lost 18.34 points to WS163.33. A run to the Caribbean on TC21 is currently marked at $525,000 (-110,833) with that rate reported on subjects at time of writing.

Handymax

Mediterranean Handymax vessels took a 34% hit this week dropping from WS253 to WS165 off the back of minimal enquiry. Likewise on the UK-Continent the TC23 declined 53.12 points to WS185.63.

VLCC

The VLCC market lost ground again this week, as we approach the Far Eastern public holiday period, with rates lower than a week ago in all areas. The rate for 270,000mt Middle East Gulf to China shrank by more than 8.5 points to WS56.64, which translates to a round-trip TCE of about $36,400 per day basis the Baltic Exchange’s vessel description.

The rate for 280,000mt Middle East Gulf to US Gulf (via the cape/cape routing) is now assessed at WS36.5, about 5.5 points down week-on-week. In the Atlantic market, the rate for 260,000mt West Africa/China fell eight points to WS57.40 showing a daily round voyage TCE of $38,000. The rate for 270,000mt US Gulf/China is now $900,000 lower than a week ago at $8,000,000 ($32,250 per day round trip TCE).

Suezmax

The Black Sea and Mediterranean markets again struggled to gain any traction with demand still low. The rate for 135,000mt CPC/Med fell 14.5 points to WS124.28 (a round-trip TCE of $53,600 per day). In the Atlantic, despite busy activity in the US Gulf and Caribbean markets early on, rates slid for 130,000mt Nigeria/Rotterdam which now sits seven points lower than a week ago at a WS90.5 (a round trip TCE of about $32,400 per day). In the Middle East, the rate for 140,000mt Basrah/Lavera dropped 8 points to WS56.88.

Aframax

In the North Sea market, the rate for the 80,000mt Hound Point/Wilhelmshaven route seems to have settled and has remained at the WS130-132.5 level since last Friday (showing a round-trip daily TCE of $37,600).

In the Mediterranean, the rate for 80,000mt Ceyhan/Lavera has hovered at the WS152.5 mark this week (a daily round-trip TCE of $44,400).

Across the Atlantic, the Stateside Aframax market crumpled as charterers became inundated by available tonnage. A major oil company relet was reported to have fixed to Chevron from East Coast Mexico to US Gulf at WS85.

Since that deal, the commentary has been that other owners may find it a difficult pill to swallow and perhaps won’t be so competitive.

The rate for 70,000mt East Coast Mexico/US Gulf is assessed now 43 points lower for the week at WS88.75 ($7,500 per day round-trip TCE) and the rate for 70,000mt Covenas/US Gulf has been reduced by 41.5 points to WS84.38 (a daily round-trip TCE of about $5,950).

For the Transatlantic route of 70,000mt US Gulf/Rotterdam, the rate crumbled 31 points to just below WS120 (showing a round trip TCE of $22,700 per day).

LNG

This month for LNG has been one of keeping the status quo. Rates have remained pretty flat throughout the month with this last week seeing only around $2,000 lost on BLNG1g Aus-Jap (out of a total $10,498 lost throughout April). Fixing has continued, although with most of the positions being from sublet tonnage there has been fewer ships available as charterers and traders hold on to cover their own contracts.

BLNG2g has stayed very stable, moving a total of $200 over the week with a total movement from the start of the month of only $691. The index published at $42,041, a slight rise, driven mainly by the fuel prices. A similar story for BLNG3g Houston-Japan, which closed at $48,217 - a rise of $400 - but from the start of the month a fall of $1,310. Market participants have been still mainly focussed on the period although rates for 1- and 3-year terms remain relatively flat. Six month period deals have seen an uptick in pricing with ships taking advantage of potentially higher winter months.

LPG

The BLPG routes saw little movement across the week once again. Fixing has continued with reported cargoes working out towards to the end of May. However, despite activity rates have remained relatively muted. Out in the East for a Ras Tanura-Chiba run, rates fell from a high of $78.571 midweek to close at $73.929 a fall of $4.5. The TCE earnings on the same run closed at $56,310 - a fall of just over $5,000.

Out in the West a greater degree of fixing was done compared to the last two weeks. This had little impact on rates with BLPG3 Houston-Chiba seeing a moderate rise of just under $6 to finish at $131.714 from a low of $125.786. This rise didn’t do much to the TCE Earnings either, which closed at $67,789. Market sentiment is pushing towards the possibility that freight might have topped out. With sustained fixing and little to see for it, charterers look to be holding back. Vessel supply remains tight though and this type of position list can get market participants a little worried. More cargoes getting worked could push rates up more. For the quite quiet BLPG2 Houston-Flushing a minimal rise closed the week at $77.2, a slight fall from the week high of $78.6, but still a gain overall from the start of $1.6.

Headquartered in London and a subsidiary of the Singapore Exchange (SGX), the Baltic Exchange publishes a range of indices and assessments which provide an accurate and independent benchmark of the cost of transporting commodities and goods by sea. These include the Baltic Dry Index (BDI), the dry bulk shipping industry's best known indicator. Published daily since 1985, this provides a snapshot of the daily spot market earnings of capesize, panamax and supramax vessel types on the world's key trading routes.

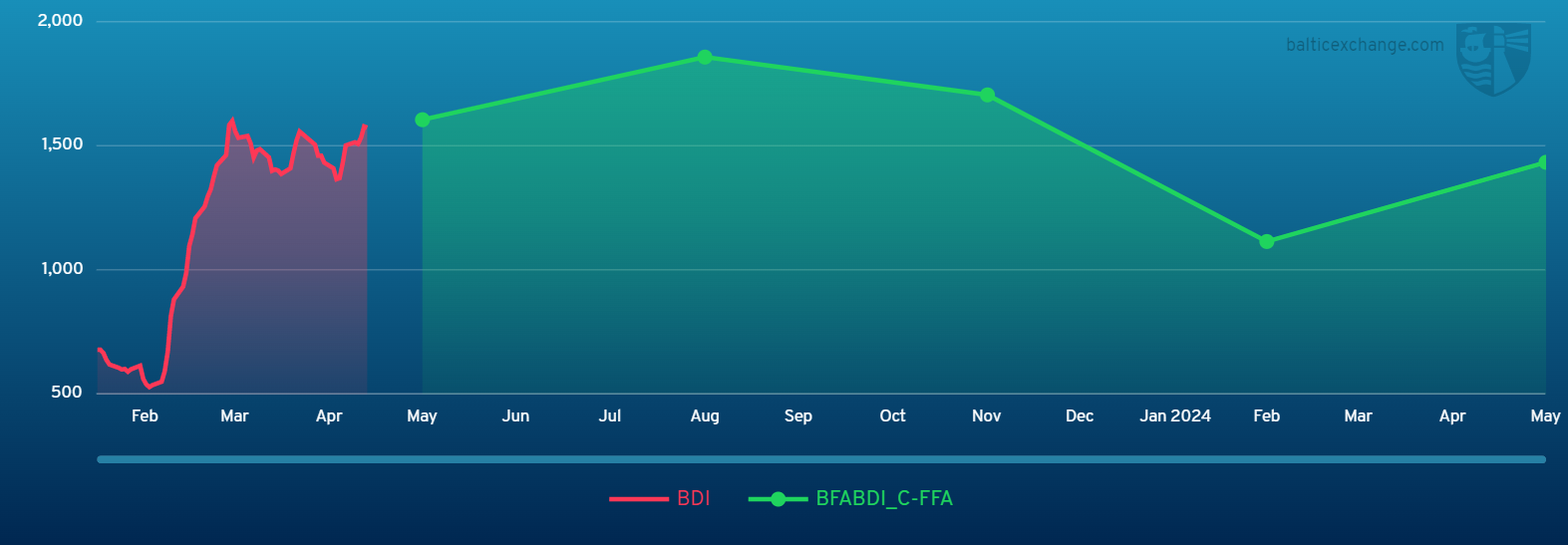

Chart shows Baltic Dry Index (BDI) during April 29, 2022 to April 28, 2023

Baltic Forward Assessment for BDI

In March 2018 the BDI was re-weighted and is published using the following ratios of time charter assessments: 40 percent capesize, 30 percent panamax and 30 percent supramax. The information is provided by a panel of international shipbrokers.

(Source: The Baltic Exchange, edited by Niu Huizhe with Xinhua Silk Road, niuhuizhe@xinhua.org)

A single purchase

A single purchase