BEIJING, Sept. 10 (Xinhua) -- The Baltic Exchange has published its weekly report of the dry and tanker markets for September 2-6, 2024 as below:

Capesize

The Capesize market saw a strong start to the week, particularly in the Pacific, where two of the three major miners became active, leading to a steady rise in the C5 route. However, as the week progressed, Pacific activity began to slow, with the C5 index dipping midweek to $11.135, having started the week at $11.785. A slight recovery followed as Thursday saw increased cargo enquiry and improved rates, although concerns lingered over Typhoon Yagi as it approached southern China. In the Atlantic, activity was more subdued on C3, with limited fixtures and initially a persistent gap between bids and offers, although as the week progressed the gap narrowed but there was no significant upward movement. Fronthaul routes out of the north Atlantic provided some support and the market maintained positive sentiment, particularly on the transatlantic route, although overall fixture volumes were low. Overall, the market showed resilience, ending the week on a stronger note, with the BCI 5TC closing at $27,832, up from its opening level at the start of the week of $26,935.

Panamax

Another softer week for the Panamax market as owners continued to feel the recent pressure, particularly in the Atlantic basin where owners' resistance was hard to find with early tonnage and ballaster tonnage continuing to discount. The P1A route hovered in the $8,000s all week, although this was being challenged with APS load port deals equating to a lot less by comparison. Activity ex EC South America was flat for index arrival dates, with earlier date arrivals heavily discounted by the armada of ballasters. Asia returned good demand overall, rates appeared to have found a floor mid-week with owner's resistance appearing more substantiated. Rates of low $14,000s were seen on NoPac trips on inferior to index types, whilst much of the Indonesia demand continued to be absorbed by smaller/older tonnage rates improved into five-figure levels. Period activity was minimal, although reports emerged of an 81,000dwt delivery China achieving $14,900 basis 5/7 months.

Ultramax/Supramax

A rather mixed affair for the sector as the summertime lull still impacted the Atlantic but a slightly more positive feel from the Asian arena. The north and south Atlantic suffered from a lack of fresh enquiry, putting downward pressure on an already subdued market. An Ultramax was heard fixed basis delivery EC South America for a fronthaul trip at $16,000 plus $600,000 ballast bonus. Elsewhere, a 56,000dwt fixed delivery Mediterranean for a run to West Africa at around $11,000.

Asia, on the other hand, seemed a bit more buoyant, although as the week ended some said prompt tonnage availability was increasing. A 58,000dwt fixing delivery China for a trip to West Africa at $14,500 for the first 60 days and $16,000 thereafter. From the south, a 60,000dwt fixed delivery Koh Sichang trip via Indonesia redelivery China at $14,750. The Indian Ocean saw a little action, with a 60,600dwt fixing delivery South Africa trip Pakistan at $18,500 plus $185,000 ballast bonus. The period market remained rather muted, with a 61,000dwt open China fixing 12-14 months trading at $15,500.

Handysize

The Handy sector saw minimal visible activity across both basins this week. In the Continent and Mediterranean, the tonnage list remains relatively long for September dates, while fresh demand appears quite thin. A 34,000dwt fixed delivery Skaw trip with grain via Baltic to Luanda at $12,500. In the south Atlantic, negative sentiment persisted throughout the week, with only a few new inquiries but no significant actions taken. Momentum in the US Gulf was also shifting slightly negative this week, with very few new enquiries and an increasing tonnage list. A 38,000dwt open San Pedro De Macoris prompt fixed for Barranquilla to Poland with coal at around $17,500. Little new information emerged from the Asian market, although some sources noted an increase in available tonnage, anticipating further market softening.

Clean

LR2

MEG LR2's seem to have found a base, with rates holding on the TC1 (75Kt MEG/Japan) at the WS115-116 level, while rates for the 90kt MEG/UK-Continent TC20 voyage hovered around the $4,000,000 mark. West of Suez, the Mediterranean/East LR2's were somewhat softer, with TC15 index losing a little over $45,500 to $2,848,010

LR1

In the MEG, LR1's going east did not have the same steadiness as their larger cousins this week. The 55kt MEG/Japan index of TC5 slackened about three points to WS140.63, although the 65kt MEG/UK-Continent of TC8 climbed another $150,000 to $3,442,400 (or $52.96/mt). On the UK-Continent, a 60Kt ARA/West Africa run on TC16 fell eight points to WS119.05.

MR

Rates were softer across all regions this week. The TC17 35kt MEG/East Africa shed 10 points to WS195 (showing a daily TCE of $16,549/day round trip). On the UK-Continent MR's the 37kt ARA/US-Atlantic coast of TC2, recent gains were lost, with the rate coming down about 17 points to WS120.74, which gives a Baltic round trip TCE of $9,335/day and the TC19 run (37kt ARA/West Africa) came off 16 points to WS140.

Across the Atlantic, the TC14 (38kt US-Gulf/UK-Continent) route lost another five points to WS148.53 (just over $15,600/day basis a round trip TCE). The 38kt US Gulf/Brazil on TC18 went from WS204.29 to WS198.57 (showing a daily round trip TCE of about $24,100) and the 38kt US-Gulf/Caribbean of TC21 closed $9,000 lower at $625,000 (a daily TCE round trip of $17,797).

Handymax

In the Mediterranean, 30kt Cross Mediterranean (TC6) took another heavy hit, closing 24 points lower than a week ago at WS114.84. In northwest Europe, the TC23 30kt Cross UK-Continent added a solitary point to its value, taking it to WS156.45 ($13,760/day round trip TCE).

VLCC

The VLCC market ended the week a little firmer, with sentiment suggesting further gains can be made. Yesterday, Vietnamese charterers took a vessel over 15 years old and ex drydock at WS45 for a trip that is considered as typically freighting at three points less than a China discharge. The 270,000 mt Middle East Gulf to China trip climbed three points week-on-week to WS47.5, which gives a daily round-trip TCE of $24,409 basis the Baltic Exchange's vessel description.

In the Atlantic market, the rate for 260,000 mt West Africa/China rose 2.5 points to WS51.78 (corresponding to a round voyage TCE of $29,487/day), whilst the rate for 270,000 mt US Gulf/China lost $100,000 to $7,170,000 ($31,565/day round trip TCE).

Suezmax

Suezmaxes in all regions have had a tough week with rates falling. In West Africa the 130,000 mt Nigeria/UK Continent voyage eased three points to WS79.31 (a daily round-trip TCE of $26,524). The TD27 route (Guyana to UK Continent basis 130,000 mt) was assessed on Thursday at WS79.44 down two points for the week, which translates into a daily round trip TCE of $26,282 basis discharge in Rotterdam. In the Mediterranean and Black Sea region, the 135,000 mt CPC/Med route lost ground just falling through the WS80 mark (showing a daily TCE of about $18,100 round-trip). In the Middle East, the rate for 140,000 mt Middle East Gulf to the Mediterranean (via the Suez Canal) was slightly firmer at WS94.44.

Aframax

In the North Sea, the rate for the 80,000mt Cross-UK Continent was 2.5 points softer at WS117.08 (translating to a daily round-trip TCE of $22,622 basis Hound Point to Wilhelmshaven).

In the Mediterranean market the rate for 80,000mt Cross-Mediterranean had 11 points taken away, closing on Thursday at the WS100 level (basis Ceyhan to Lavera showing a daily round trip TCE of $14,900).

Across the Atlantic, the market has found the bottom, for the moment. For 70,000 mt east coast Mexico/US Gulf (TD26) owners maintain at WS100.94 (a daily TCE of $12,300 round trip, about $1,000/day more than a week ago). The same was seen for 70,000mt Covenas/US Gulf (TD9) holding on to the WS100 level (a round-trip TCE of a little over $12,300/day). The rate for the transatlantic route of 70,000 mt US Gulf/UK Continent (TD25) eased three points to WS127.78 (a round trip TCE basis Houston/Rotterdam of $25,428/day, about $300 per day less than a week ago).

LNG

As the weather in the UK moves decidedly into autumn and the winter is fast approaching, there had been hopes the LNG market would see the typical winter boost. However, with no sign on the horizon of a rate rise coming, there are worries it could be a rather slow period still for LNG, at least when it comes to spot activity. Gas Tech is just around the corner and those gearing up for a busy few days will be keen to see what the LNG market has been working on.

In regard to the rates this week, there hasn't been much to report. The Pacific market has continued its fall and BLNG1 Aus-Japan on the 174cbm fell by $4,000 to $73,000 while the 160cbm fell to $58,800. Across the Atlantic BLNG2 Houston-Cont saw a minimal fall closing at $58,800 and $45,900 for the 174cbm and 160cbm, respectively. BLNG3 Houston-Japan moved least of the three but still lost some value with a close of $78,500 on the 174cbm and $62,500 on the 160cbm.

Period for longer term remains active and there are discussions taking place for 10 years plus, but the Baltic print of six-month period fell to $91,300 while the one-year term finished down at $75,700 and the three-year closed at $81,600.

LPG

The sluggish market has continued this week, with few reported fixtures and rates beginning to fall on the back of sentiment and the lack of open interest. Tonnage remains longer and with few cargoes working, the rates have reacted as expected falling by several dollars. BLPG1 Ras Tanura-Chiba fell by $4.667 from a high of $64 to $59.333 pushing TCE Earnings down, as well by $4,729 to an equivalent of $8,754/day.

Across the Atlantic, the market wasn't much busier with very little being reported and open tonnage, although tighter than in the East, beginning to pile up rates took a hit. BLPG2 Houston-Flushing dropped by $2.75 to $64.125 while the TCE earnings fell to $65,860. BLPG3 Houston—Chiba lost the most this week falling from a high of $118.833 to $114 and TCE earnings falling to a close of $45,361.

Headquartered in London and a subsidiary of the Singapore Exchange (SGX), the Baltic Exchange publishes a range of indices and assessments which provide an accurate and independent benchmark of the cost of transporting commodities and goods by sea. These include the Baltic Dry Index (BDI), the dry bulk shipping industry's best known indicator. Published daily since 1985, this provides a snapshot of the daily spot market earnings of capesize, panamax and supramax vessel types on the world's key trading routes.

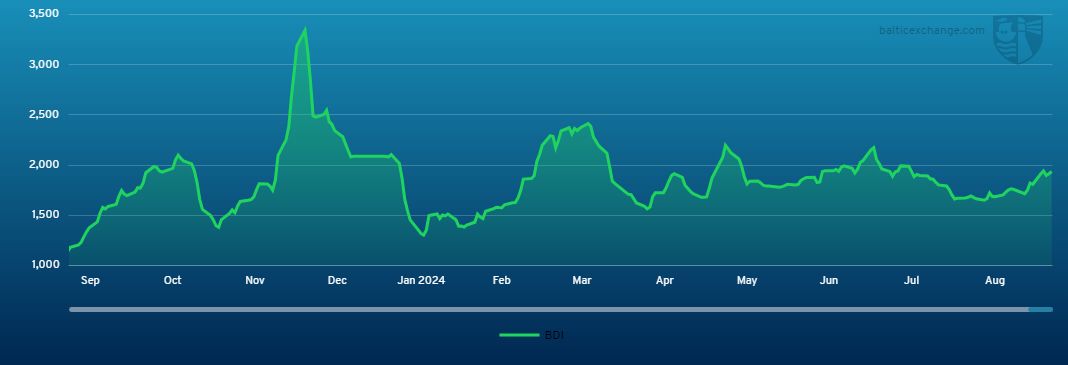

Chart shows Baltic Dry Index (BDI) during Sept. 8, 2023 to Sept. 6, 2024

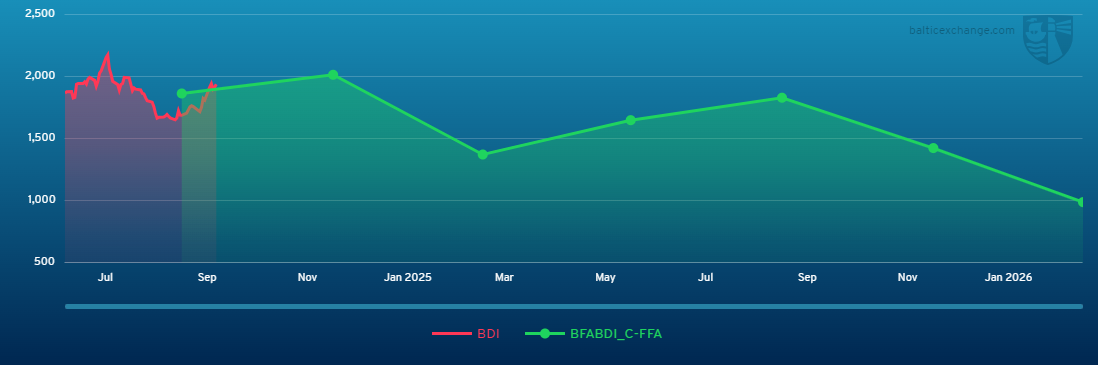

Baltic Forward Assessment for BDI

In March 2018 the BDI was re-weighted and is published using the following ratios of time charter assessments: 40 percent capesize, 30 percent panamax and 30 percent supramax. The information is provided by a panel of international shipbrokers.

(Source: The Baltic Exchange, edited by Niu Huizhe with Xinhua Silk Road, niuhuizhe@xinhua.org)

A single purchase

A single purchase