BEIJING, July 1 (Xinhua) -- The Baltic Exchange has published its weekly report of the dry and tanker markets for June 24-28, 2024 as below:

Capesize

The Capesize market experienced an eventful week despite starting off quietly with the BCI 5TC dropping by $409 to $25,650 on Monday. However, the market turned around midweek with a surge in activity, especially in the Atlantic. Demand from south Brazil and West Africa to the Far East for July loaders drove a tightening of the ballaster list, significantly boosting rates resulting in the BCI 5TC increasing by $1,288 to $26,082. Brokers reported by Wednesday and Thursday that approximately 18-20 fixtures had been concluded, substantially reducing the number of ballasters and adding pressure to the market. This increased activity resulted in the BCI 5TC, rising to $28,557 by the week's end. The Pacific market experienced a boost, with improved rates and stronger sentiment as a result C5 rates increased by approximately 0.50 cents, although activity levels have significantly diminished as the week concluded with the C5 index seeing a slight adjustment of 0.165 to end the week at $11.165.

Panamax

A further eroding of rates across the board for the Panamax market this week. The Atlantic returned smaller losses and throughout the week sources spoke of a two-tiered market between the mineral and grain trades, with the former seeing again hugely discounted rates, whilst $15,500 was agreed on a scrubber fitted vessel for a trans-Atlantic trip via NC South America. Rates ex South America continued to ease, with minimal activity as charterers with time decided to hold back, with several deals delivery aps EC South America 5/10 July were heard concluded around the low-mid $17,000's and equivalent ballast bonus. Asia, beset all week by a growing tonnage list, saw rates fall away dramatically, with $12,750 being concluded basis an 81,000dwt delivery South Korea for a NoPac round trip, sentiment remains bearish with little signs of a recovery. Limited period activity, however, with reports of an 82,000dwt delivery Indonesia achieved low $18,000's for 22/25 months period.

Ultramax/Supramax

Mixed fortunes again for the sector, as 'summertime blues' probably described the Atlantic whilst from Asia the week started on a positive note, although as it finished even here positive sentiment eroded. The Atlantic was rather positional, with demand from the US Gulf seemingly ebbing away, although a 63,000dwt was heard to have fixed a fronthaul from NC South America at $26,000. A similar story from the Continent-Mediterranean as prompt tonnage became readily available. A 56,000dwt fixing delivery Spain to US east coast at $9,000. From Asia, changing fortunes during the course of the week. Little fresh enquiry was seen from the south whilst better levels of interest had been seen further north. A 55,000dwt open Djakarta fixed a trip via Indonesia to China in the mid $17,000s. The Indian Ocean remained rather flat, with a 63,000dwt open Bangladesh fixed a trip via EC India redelivery China with iron ore at $16,500.

Handysize

A lackluster feel was seen across the handy sector as the week progressed. The Continent and Mediterranean were the highlights of the Atlantic, with a 38,000dwt fixing from the Black Sea to Morocco with grains at $14,000 whilst a 33,000dwt fixed from Middlesbrough to the US Gulf with a cargo of steels at $12,500. In the south Atlantic, a large handy was rumoured to have fixed from Recalada to west coast South America in the low $20,000s but further details had yet to surface. After a period of positivity, the US Gulf showed signs of stabilizing, with a 35,000dwt fixing from Cape Henry to the north Continent with coal at $15,000. Visible activity in the Asia markets was minimal but numbers had remained steady. A 33,000dwt fixing from Japan via South Korea to WC India with coils at $14,000. Period activity surfaced with a 37,000dwt fixing basis delivery SW Pass for 3 to 5 months, with Atlantic redelivery at $15,000.

Clean

LR2

MEG LR2's were subject to downward pressure this week. The TC1 rate for 75Kt MEG/Japan dropped 17.5 points to WS180.56 and the 90kt MEG/UK-Continent TC20 voyage is went from $6.08m to $5.89m.

West of Suez, Mediterranean/East LR2's continued to be sedate this week. The TC15 index remained level around $3.5m.

LR1

In the MEG, LR1's were seemingly unaffected by the drop affecting their larger sisters this week. The 55kt MEG/Japan index of TC5 trundled along in the WS230's and the 65kt MEG/UK-Continent of TC8 went from $4.61m to $4.85m.

On the UK-Continent, a 60Kt ARA/West Africa run on TC16 came down 8% to WS142.22 taking the Baltic TCE for the run to $35,306/day round trip.

MR

MR's in the MEG eventually came down, holding early in the week at around the WS340 level but a mid-week fixture much lower drove the index down 23.21 points to WS312.86 at present.

On the UK-Continent MR's began to optimistically resurge this week. The 37kt ARA/US-Atlantic coast of TC2 hopped up 30 points to WS182.19 or a Baltic round trip TCE of $19,944/day. The TC19 run (37kt ARA/West Africa) also went from WS174.06 to WS202.19.

As USG MR's continued their firm charge upwards this week. TC14 (38kt US-Gulf/UK-Continent) shot up 37.14 points to WS238.57. The 38kt US Gulf/Brazil on TC18 went from WS300.71to WS342.14 and the 38kt US-Gulf/Caribbean of TC21 jumped up 40% to $1.45m returning $65,000/day on Baltic description round trip TCE.

The MR Atlantic Triangulation Basket TCE climbed 28% to $46,085.

Handymax

In the Mediterranean, 30kt Cross Mediterranean (TC6) climbed back up to the tune of 37.5 points to its current mark of WS182.5.

In northwest Europe, the TC23 30kt Cross UK-Continent also hopped up from WS164.72 to WS177.22.

VLCC

The VLCC market remained relatively stable this week, with the rate for the benchmark 270,000mt Middle East Gulf to China climbing a modest 0.15 points to WS49.7, which gives a daily round-trip TCE of $26,135 basis the Baltic Exchange's vessel description.

In the Atlantic, the market was very similar to the Middle East Gulf. The 260,000mt West Africa to China ultimately climbed to WS55.34 (+0.38) showing a round voyage TCE of $32,876/day, and the rate for 270,000mt US Gulf to China dropped by $180,000 to $7,760,000 making a round-trip daily TCE of $35,654.

Suezmax

The Suezmax market in West Africa and the Mediterranean/Black Sea region have been flat/soft this week. The rate for 130,000mt Nigeria to UK Continent fell from the WS112.5 level to WS109.83 (a daily round-trip TCE of around $42,859) and the 135,000mt CPC/Mediterranean route held resolute around the WS120 mark (showing a daily TCE of $47,709 round-trip). In the Middle East, the rate for 140,000mt Middle East Gulf to the Mediterranean (via the Suez Canal) was stable at around the WS94-95 mark.

Aframax

In the North Sea, the rate for the 80,000mt Cross-UK Continent dropped another 10.41 points to WS157.92 (a daily round-trip TCE of $53,679 basis Hound Point to Wilhelmshaven).

In the Mediterranean market the rate for 80,000mt Cross-Mediterranean picked up 6.77 points this week to WS153.33 off the back of some improved activity, (basis Ceyhan to Lavera, that shows a daily round trip TCE of $40,450).

Across the Atlantic, negative sentiment, regrettably for owners, continued this week. For the 70,000mt east coast Mexico/US Gulf (TD26) the rate sunk 45.62 points to WS176.88 (a daily TCE of $42,032 round trip) and the rate for 70,000mt Covenas/US Gulf (TD9) was 40 points softer at WS174.38 (a round-trip TCE of $38,861/day). The rate for the trans-Atlantic route of 70,000mt US Gulf/UK Continent (TD25) fell another 14.72 points to WS172.78 (a round trip TCE basis Houston/Rotterdam of $39,580/day).

LNG

It is past the midpoint of the year and the LNG market is looking at what is next, with rates firming and the more modern and efficient 2-stroke ships pulling away from TFDE tonnage. Interest from charterers is there and there were several fixtures concluded this week with interest up until the last day of trading. For BLNG1 Aus-Japan on the 174cbm rates climbed, although not much, and finished flat at $50,900 while the 160cbm TFDE ship moved higher closing the delta slightly at $39,654. For BLNG2 Houston-Cont the 174cbm 2-stroke ships moved up by nearly $10,000 to close at $87,300 while the 160cbm TFDE ship languished behind finishing on a publication of $67,700. This delta was repeated on BLNG3 Houston-Japan where the 174cbm finished up at $94,900 while the 160cbm finished $75,511.

This widening of the delta is not unexpected the modern 2-stroke ships remain the first choice, as they allow greatest options for transits to both east and western markets. While BLNG1 remains tighter, there is greater availability of tonnage and keeping the delta tighter.

Period continues to be buoyant with multi-month deals moving up to $109,400 for a six-month charter. There is less movement on one-year and three-year constructs where ideas of where the LNG market is headed remains a little unclear. These periods finished at $85,000 and $85,500, respectively.

LPG

The MEG BLPG1 Ras Tanura-Chiba route had an up and down week, beginning lower the rates climbed to a high of $71.714 before falling to the close of $68.857 (a total drop of $3.286 for the week). The TCE earnings moved marginally gaining $3,397 to a close of $49,329. The fixing window now is looking out to the last decade of July, although brokers report that there could be a stay of calm while charterers wait for the lists to be replenished.

The Western market was quiet, with few fixtures meaning the rates softened across both BLPG2 and BLPG3. Houston-Chiba lost $4.357 to finish at $117.357 with a daily TCE earning equivalent of $47,758, while BLPG2 Houston-Flushing dropped $2.6 to a close of $66.2 and a daily TCE earning equivalent of $66,464.

Headquartered in London and a subsidiary of the Singapore Exchange (SGX), the Baltic Exchange publishes a range of indices and assessments which provide an accurate and independent benchmark of the cost of transporting commodities and goods by sea. These include the Baltic Dry Index (BDI), the dry bulk shipping industry's best known indicator. Published daily since 1985, this provides a snapshot of the daily spot market earnings of capesize, panamax and supramax vessel types on the world's key trading routes.

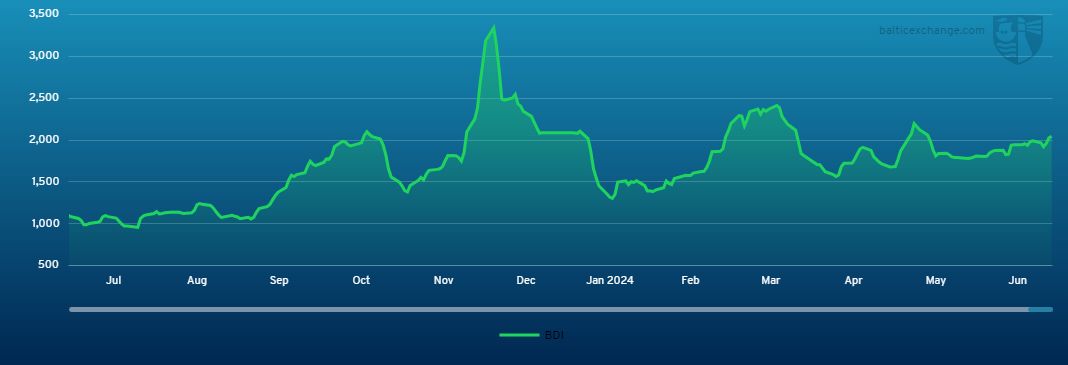

Chart shows Baltic Dry Index (BDI) during June 30, 2023 to June 28, 2024

Baltic Forward Assessment for BDI

In March 2018 the BDI was re-weighted and is published using the following ratios of time charter assessments: 40 percent capesize, 30 percent panamax and 30 percent supramax. The information is provided by a panel of international shipbrokers.

(Source: The Baltic Exchange, edited by Niu Huizhe with Xinhua Silk Road, niuhuizhe@xinhua.org)

A single purchase

A single purchase