BEIJING, Dec. 5 (Xinhua) -- The Baltic Exchange has published its weekly report of the dry and tanker markets for November 27- December 1, 2023 as below:

Capesize

This week has been exceptional for the capesize market, consistently gaining traction. The Pacific market kicked off the week with strong momentum, with all the major players from west Australia to China actively participating. The Atlantic witnessed a notable uptick, prompting owners to favour ballasting towards this region. The positive sentiment in the Atlantic persisted despite reduced activity from south Brazil and West Africa. Tuesday saw subdued activity in the Pacific, resulting in a slight decline in C5 rates, but stability prevailed overall. Tight conditions in the north Atlantic led to an optimistic outlook, with anticipation of further upward pressure on rates. Wednesday brought a rebound in the Pacific, contributing to a surge in rates that was also witnessed in the north Atlantic. Brokers indicated a reduction in available ballasters from the Pacific to the Atlantic, limiting arrivals in south Brazil in December. This resulted in more constrained conditions in the south Atlantic, coupled with a notable presence of a major on C3 looking for December loaders, prompting a substantial increase in rates. As the week concludes, the overall sentiment remains highly optimistic, as exemplified by the BCI 5TC. It commenced the week at $31,671 and has experienced a notable increase, reaching $51,727 by close.

Panamax

Whilst not as spectacular as the capesize market, the recent bull continued in the Panamax market this week, yielding solid gains for the owners. The north Atlantic was driven by tonnage shortage hindered by severe weather delays, consequently authentic trans-Atlantic rounds were seen concluded several times towards the upper $28,000s. Activity ex South America was less prevalent; however, rates did see a small up-tick towards the end of the week. A similar picture emerged in Asia tight tonnage count appeared on the nearby, with the Indonesia to China coal supply transpiring as a catalyst for firmer numbers on these trips and filtering into the longer Australia coal trips into Japan/India etc. A $18,500 figure being the headline rate on an 81,000dwt delivery Japan for a trip via New Zealand to South Korea run, whilst $16,000 emerged as the median rate for NoPac round trips as the immediate firm outlook continued to find support.

Ultramax/Supramax

A strong week for the sector as a lack of prompt tonnage in areas such as the US Gulf and Mediterranean fueled positive momentum with the knock-on effect of seeing charterers sourcing tonnage further afield. From Asia, a slightly less turbulent week, although as the week closed rates and demand were seemingly pushing up with better numbers being achieved. Period cover was actively sort, with a 52,000dwt open Turkey was fixed for minimum four months to about six months trading at $20,000, whilst a 61,000dwt open New Mangalore was fixed for minimum three months to maximum 4.5 months trading at $16,500. Stronger numbers were seen in the Atlantic, with a 63,000dwt fixing delivery US Gulf with wood pellets for a trip to the Continent at $39,000, whilst Ultramaxes were fixing at close to $18,000 plus $800,000 ballast bonus for South American fronthaul cargoes. From Asia, a 56,000dwt was fixed for a trip from Singapore to China at $17,000, whilst a 63,000dwt was heard to have been fixed delivery Japan for a NoPac round redelivery Southeast Asia in the mid $17,000s.

Handysize

Unlike the larger sisters, the Handysize sector had a rather calmer feel, certainly from Asia where cargo and tonnage levels remained finely balanced. That said, as the week closed owners’ expectations were on the rise and looking forward there was a more positive feel. In the Atlantic, a lack of prompt tonnage from South America saw stronger numbers being achieved, with a 35,000dwt fixing delivery Recalada in early December for a trip with steels to the US Gulf at $25,000. Further north, a 37,000dwt was heard to have been fixed delivery US Gulf for a trip to Morocco at $27,000. From the Continent, a 36,000dwt was heard to have been fixed delivery Baltic for a trip via Hamburg to Portugal at around $18,000-$19,000. There was also talk of a 33,000dwt fixing delivery Skaw for a trip via Russian Baltic to the US Gulf with fertiliser at $20,000.

Clean

LR2

LR’s in the MEG have been on a downward trajectory this week. The 75Kt MEG/Japan TC1 index lost 16.11 points to WS113.33 with reports of WS107.5 currently on subjects in the market. The 90kt MEG/UK-Continent TC20 run to the UK-Continent also dropped 10% of its value to $3.19m. West of Suez, Mediterranean/East LR2’s on TC15 returned to being sedate, with the index dropping off $244,000 to $3.45m as a result.

LR1

In the MEG, LR1 freight levels have managed to hold stable despite the downturns of the vessel sizes either side of them. The 55kt MEG/Japan index of TC5 dipped an incremental 3.12 points to WS119.38 and the 65kt MEG/UK-Continent of TC8 ticked down across the week from $2.91m to $2.78m. On the UK-Continent, the 60kt ARA/West Africa TC16 index, hovered around the WS200-205 range all week after WS205 reported on subjects during the week.

MR

MR’s in the MEG took a tumble this week. The 35kt MEG/East Africa TC17 index subsequently shed 28.57 points to WS170. UK-Continent MR’s resurged optimistically this week, while rates in the USG attracting ballast vessels to head in that direction for the moment. The 37kt ARA/US-Atlantic coast of TC2 shot up nearly 20% this week to WS216. Similarly TC19 (37kt ARA/West Africa) added 36.87 points, taking its value to WS235.31. Baltic round trip TCE’s for the runs are up to $27,000/day and $32,000/day, respectively.

The USG MR’s reached the top of their current rally this week, followed by a correct down. TC14 (38kt US-Gulf/UK-Continent) peaked at WS280.71 up from WS264.29 and is back down at WS267.86 at time of writing. The 38kt US Gulf/Brazil on TC18 followed a similar trend, reaching a precipice of WS365 with the index currently marked at WS357.14 or $58,000/day round trip on Baltic TCE. A 38kt US-Gulf/Caribbean TC21 trip topped out at $1.95m early in the week to shuffle back down to $1.78m ($84,000/day on Baltic round trip TCE).

The MR Atlantic Triangulation Basket TCE ultimately climbed from $55,212 to $59,782.

Handymax

In the Mediterranean, Handymax’s were subject to a sharp drop to the WS260’s where they look to have plateaued. Up in northwest Europe, the TC23 30kt Cross UK-Continent rallied 6.67 points to the mid WS180’s.

VLCC

Rates for the sector showed the tiniest movement downwards, except for the US Gulf to China run, which suffered a heavier burden. The rate for 270,000 mt Middle East Gulf to China remained around the WS66.5 level, which corresponds to a daily round-trip TCE of just over $46,000 basis the Baltic Exchange’s vessel description, although this is actually almost $2,000 greater than a week ago. The 280,000 mt Middle East Gulf to US Gulf trip (via the cape/cape routing) is still assessed around the WS36 mark.

In the Atlantic market the rate for 260,000 mt West Africa/China is now a point off from last Friday’s number at WS67.4 (which shows a round voyage TCE of a little over $47,000/day), while the rate for 270,000 mt US Gulf/China lost $278,889 to $9,861,111 ($44,126/day round trip TCE).

Suezmax

Suezmaxes in West Africa remained at levels seen last Friday where the rate for 130,000 mt Nigeria/UK Continent plateaued at WS98.77 (a daily round-trip TCE of $36,195). In the Mediterranean and Black Sea region the 135,000 mt CPC/Med route slipped a solitary point to WS137.35 (showing a daily TCE of $63,326 round-trip). In the Middle East, the rate for 140,000 mt Middle East Gulf to the Mediterranean lost four points to just under WS69.

Aframax

In the North Sea, the rate for the 80,000 mt Cross-UK Continent route was cropped by another 20 points to WS145.36 (showing a round-trip daily TCE of $46,546 basis Hound Point to Wilhelmshaven). In the Mediterranean market, the rate for 80,000 mt Cross-Mediterranean continues to hover around WS150 (basis Ceyhan to Lavera, with a daily round trip TCE of $41,605, about $500/day firmer than a week ago).

On the other side of the Atlantic, after returning from Thanksgiving, the market has been tracking downwards since Monday. The rate for 70,000 mt east coast Mexico/US Gulf (TD26) has fallen 10 points since Monday to WS181.56 (a daily round-trip TCE of $48,692) while the 70,000 mt Covenas/US Gulf rate has shed just five points to WS170.63 (a round-trip TCE of $46,546/day). The rate for the trans-Atlantic route of 70,000 mt US Gulf/UK Continent also slackened by five points to WS176.88 (a round trip TCE basis Houston/Rotterdam of $43,808/day).

LNG

It was another quiet week overall for LNG. A little flurry of activity in the Pacific basin didn’t do much to bolster rates, with one MEGI ship reported at $140,000 for January loading in the East, a downward correction could have been expected. With little cargo out there and charterers looking for modern tonnage, which is very thin on the ground the levels have remained somewhat stagnant.

For BLNG1g Aus-Japan a slight dip of $2,769 gave a final publication of $142,998, while the Atlantic routes fared slightly better. BLNG2g USG-Cont rose by $3,400 to finish at $160,249 while BLNG3g USG-Japan fell little to close at $166,371. Like in LPG the Panama Canal is causing issues on scheduling and availability but it hasn’t affected freight rates quite as much, at least not yet. Period is quiet there have been no reported term fixtures for six month up to 1-3 years as yet, although charterers are interested in seeing what opportunities could be available in the new year.

LPG

The AG market has lost $5.428 this week to close at $148.143 giving a daily TCE earning of $136,571. It’s been a tough one for the market. Activity has been muted but tonnage remains stronger with pretty much all ships that are finished in the East re-routing via the AG to make their way back to the US. The Panama Canal is still having quite an affect and with such availability of tonnage, rates have taken a hit.

The main thing hogging the headlines is the Panama Canal. Nothing new reported so far, but the market is reacting now with rates forming an almost two tier market. Panamax vs. Neo-Panamax transiting vessels have quite the disparity between rates, with reports for those ships transiting the canal (of which it is almost exclusively Panamax size) showing levels of over $300, while the Baltic Standard ships, and therefore the index, has fallen quite significantly to $223.571 (a fall of $15.572). What’s important to note is that brokers are reporting that ships fixing via the Suez Canal or via the Cape, though they avoid huge delays in Panama Canal transits are giving almost the same sort of TCE earnings to charterers by taking the longer route hence the correction down. The Baltic TCE was published at $133,821 for BLPG3. BLPG2 has been quiet with nothing reported fixed into Flushing. Rates themselves lost $8 over the week to finish at $126 and a daily TCE earning of $152,132.

Headquartered in London and a subsidiary of the Singapore Exchange (SGX), the Baltic Exchange publishes a range of indices and assessments which provide an accurate and independent benchmark of the cost of transporting commodities and goods by sea. These include the Baltic Dry Index (BDI), the dry bulk shipping industry's best known indicator. Published daily since 1985, this provides a snapshot of the daily spot market earnings of capesize, panamax and supramax vessel types on the world's key trading routes.

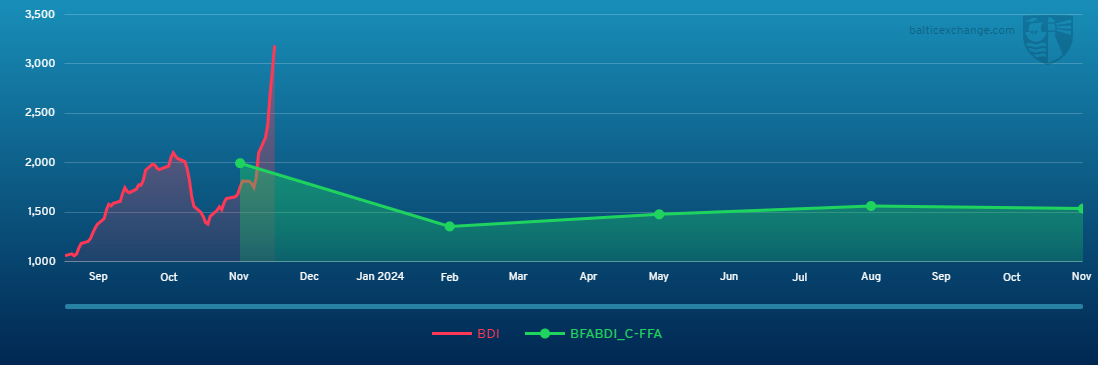

Chart shows Baltic Dry Index (BDI) during Dec. 2, 2022 to Dec. 1, 2023

Baltic Forward Assessment for BDI

In March 2018 the BDI was re-weighted and is published using the following ratios of time charter assessments: 40 percent capesize, 30 percent panamax and 30 percent supramax. The information is provided by a panel of international shipbrokers.

(Source: The Baltic Exchange, edited by Niu Huizhe with Xinhua Silk Road, niuhuizhe@xinhua.org)

A single purchase

A single purchase