BEIJING, May 15 (Xinhua) -- The Baltic Exchange has published its weekly report of the dry and tanker markets for May 8-12, 2023 as below:

Capesize

The capes started the week on an upbeat note. All three majors were active in the market at the beginning of the week, resulting in a healthy volume of cargo from West Australia to China. As a result, rates pushed up accordingly, together with a positive paper market. Although by mid-week there was a feeling that the Pacific was looking a little toppy and sentiment shifted. This was also reflected in the paper market losing value. Rates began to diminish towards the end of the week, with a noticeable lack of activity. Brokers said that the supply of tonnage in the North Atlantic is tight and remained so during the week. There were stronger fronthaul and trans-Atlantic fixtures concluded earlier in the week, although, overnight brokers said a slightly softer fixture was done from Seven Islands to China. At the beginning of the week there was more activity from South Brazil to China and conditions were said to be steady. As the week comes to an end there is a quieter feel, particularly from South Brazil to China, which appears to be rather flat. There is a spread starting to develop between charterers’ and owners’ ideas, which has resulted in many owners taking the attitude to watch, wait and see.

Panamax

After a mixed start it returned a week of negativity with rates falling throughout. Reduced fixing volumes and a build-up of tonnage in most origins gave charterers the upper hand and reduced bids consequently became the common theme. The Atlantic lacked any real demand, both in the North and the South, this week. Ballaster tonnage began to show signs of under pinning rates and many APS load port deals were concluded for end May/early June arrival ex EC South America. Earlier in the week, several reports of 82,000dwt types achieving about the $17,500+$750,000-mark basis delivery aps EC South America for trips to the Far East. Asia began the week with solid coal demand, ex Australia to India, but overall the arena returned an oppressed market with rates easing, including an 82,000dwt delivery China agreeing $12,250 for a trip via Australia redelivery India. Period activity was slim, although reports emerged of an 81,000dwt agreeing $15,250 basis 8/10 months.

Ultramax/Supramax

A mixed bag during the week as brokers described a rather positional feel to many areas. In the Atlantic, the US Gulf seemed to be gaining momentum, although little information surfaced. Further South, EC South America saw little fresh impetus, with some commenting little fresh enquiry kept a lid on rates. From Asia, it appeared to a two-tier market as the small size lost out rate wise to the larger Ultramax size, which some charterers preferred to utilise. A little more enquiry was seen from the North, although generally it remained finely balanced. From the Atlantic, a 61,000dwt was heard fixed delivery US Gulf trip to the Arabian Gulf at $24,000. Elsewhere, a 53,000dwt was fixed delivery West Africa for a trip to the Continent at $12,250. From Asia, a 56,000dwt open China fixed a trip to the Mediterranean at $9,500. Further south, a 61,000dwt fixed delivery East Kalimantan trip via Indonesia redelivery Vietnam at $19,000. The Indian Ocean saw a little action, with a 61,000dwt fixing delivery Durban trip redelivery Far East at $20,000, plus $200,000 ballast bonus.

Handysize

Despite minimal visible activity, positivity returned to the Asia markets, although the Atlantic continued to see a general lack of enquiry leading to a growing list of open vessels. A 32,000dwt was fixed basis delivery passing Skaw for a trip to the Mediterranean at $13,000, whilst a large handy was rumoured to have been fixed for a trip from Damietta, with 15-20 May dates to the US Gulf with an intended cargo of cement in the low to mid-teens with a figure of about $150,000 for hold cleaning. A 33,000 dwt open in Geelong was fixed via Adelaide to South East Asia with an intended cargo of grains at $15,500. A 38,000dwt opening in CJK was fixed for a trip to EC Central America at about $10,000. Whilst a 28,000dwt opening in South Korea was rumoured to have been placed on subjects for a trip via North China to South East Asia at $7,000.

Clean

LR2

LR2 freight in the MEG looks to have bottomed out this week. TC1 levelled off at WS145 to then return to WS154.69 after several vessels fixed at WS150. A trip west on TC20 has ticked up $153,572 to $3,832,143.

West of Suez, Mediterranean/East LR2’s have been notable quiet this week. The TC15 index dropped $191,666 to $2,941,667, the first time the route has been sub $3,000,000 since early February.

LR1

In the MEG, LR1’s have been stable this week. TC5 has remained in the WS175-180 mark all week and west run on TC8 hovered around the $3,400,000-3,500,000 level.

On the UK-Continent, TC16 suffered from inactivity and the index dipped 16.07 points to WS117.86.

MR

MEG MR’s saw a sharp upturn this week, TC17 has shot up 68.82 points to WS317.14 giving the Baltic TCE a 122% increase to $41,782/day round trip.

Despite more activity on the MR’s in the UK-Continent this week, a glut of available tonnage has kept freight sliding downward. TC2 shed 25.28 points and is currently pegged at WS125.83 and similarly TC19 is marked at WS136.79 (-22.50).

In the US Gulf, the MR’s were retested back down this week. TC14 was quickly cut back down 15.41 points to WS84.17 after WS85 was fixed a couple of times. TC18 shed 19/17 points to WS147.08. A run to the Caribbean was also retested down to $550,000 mid-week, leading the TC21 index to where currently sits at $533,333.

The MR Atlantic Triangulation Basket TCE dropped from $21,347 to $14,164.

Handymax

Mediterranean Handymax’s were subject to diminished activity levels this week. Despite this there was just enough to hold the TC6 index at WS150 all week.

Up on the UK-Continent, the TC23 index took a 34.7 point cut to WS117.49.

VLCC

The rate for 280,000 mt Middle East Gulf to US Gulf (via the cape/cape routing) is now assessed one point lower than a week ago at WS31.39, while the rate for 270,000 mt Middle East Gulf to China reduced about seven points by midweek and rebounded two points on Thursday to be assessed now at WS40.45, giving a corresponding round trip TCE of $15,500 per day basis the Baltic Exchange’s vessel description.

In the Atlantic market, the rate for 260,000 mt West Africa/China sank to WS40 midweek but due to the firmer demand in the US Gulf & Caribbean region, drawing tonnage away from West Africa, rates have rebounded five points to be assessed at WS44.70, which shows a daily round voyage TCE of $22,300. Since publishing at this level yesterday, Chevron have been reported to have taken a Maran vessel on subjects at WS45 for West Africa to Eastern options.

A busy week in the US Gulf arena has pushed rates up $138,889 from a week ago for 270,000 mt US Gulf/China, which is now assessed at $6,905,556 ($23,900 per day round trip TCE).

Suezmax

The Black Sea and Mediterranean markets firmed this week with the rate for 135,000mt CPC/Med rising six points to WS126 (a round trip TCE of $55,700 per day).

In the Atlantic region, the West African market became busier than seen in recent weeks, while the US Gulf & Caribbean region continues to attract tonnage away, and rates rose 24 points for 130,000 mt Nigeria/Rotterdam, which now sits at WS116.5 (a round trip TCE of $50,600 per day).

In the Middle East, the rate for 140,000mt Basrah/Lavera gained further strength, rising 10 points this week to WS70.75.

Aframax

In the North Sea market, the rate for the 80,000 mt Hound Point/Wilhelmshaven route climbed 7.5 points to almost WS136 (showing a round-trip daily TCE of $42,100).

In the Mediterranean, the rate for 80,000mt Ceyhan/Lavera remained flat at WS162.5 (a daily round trip TCE of $50,600).

Across the Atlantic, the Stateside Aframax market had charterers under pressure early on and by midweek were unable to resist the owners’ strength. Rates have gone on a somewhat meteoric rise and now the rate for 70,000 mt East Coast Mexico/US Gulf is 186 points higher than a week ago at WS380 ($145,600 per day round-trip TCE) and the rate for 70,000mt Covenas/US Gulf has risen 175 points (or increasing 100%) to WS351.25 (a daily round-trip TCE of $120,800).

For the trans-Atlantic route of 70,000 mt US Gulf/Rotterdam, the rate was catapulted 86.5 points to WS256 (showing a round trip TCE of $77,525 per day), which may start attracting tonnage ballasting from Europe if the demand continues and is not depleted by the Suezmax and VLCC activity on this route.

LNG

There has been some fixing activity on the spot with LNG. At the beginning of the week a 155 cbm vessel was fixed from Gladstone up to JKTC for mid-June dates in the high $40,000s. The market has since come down a touch, with rates falling to $43,262 on BLNG1g, a decrease of $6,764 on the week. There are further ships working cargoes at the moment, but rates are hovering around their bottom with expectations of a further fall very low.

Out in the Atlantic, rates moved in a similar direction. There have been several tenders floated and ships have offered in, although with many market players already with good coverage, there has been muted interest and rates are stagnated around the lower levels. For a BLNG2g run Houston-Cont a fall below $40,000 shows the lack of interest really as we published at $38,701. While a US-Japan BLNG3g also closed below the $40k mark at $39,811. Opinions between panellists for LNG have been split the last few weeks, with outliers suggesting a difference of opinion. This has now narrowed and most market players see the same levels achievable for what business is fixed.

LPG

The Middle East has continued its bull run, with rates rising just under $10.5 over the week to give a closing index publication of $90.143 (a daily TCEC earning return of $75,423). On Monday a rise of $7 in the index set the week off to a good start with market participants seeing bid/offers at ever increasing numbers. This has been the result of plenty of cargoes coming into the market, acceptances were out early on and this fresh interest gave credence to owners pushing higher who already had the bit between their teeth.

The US market faired almost as well but with a little less of a meteoric rise. Rates finished strong reversing some of the lack lustre sentiment of late, continued fixing against open cargoes and tenders being offered up has kept pressure on an ever-tightening position list and for BLPG3 Houston-Chiba closed at $138.714 a rise of more than $5.5 on the week. One vessel fixed for last decade June dates had options for China and Flushing from Houston at $138 and $82 respectively. We did not quite hit the mark of $82 with the index but with delays still in the canal and ships fixed for more long haul there is pressure still on requirements optionality, which is expected to push rates above the Baltic publication of $81.2 at the end of the week.

Headquartered in London and a subsidiary of the Singapore Exchange (SGX), the Baltic Exchange publishes a range of indices and assessments which provide an accurate and independent benchmark of the cost of transporting commodities and goods by sea. These include the Baltic Dry Index (BDI), the dry bulk shipping industry's best known indicator. Published daily since 1985, this provides a snapshot of the daily spot market earnings of capesize, panamax and supramax vessel types on the world's key trading routes.

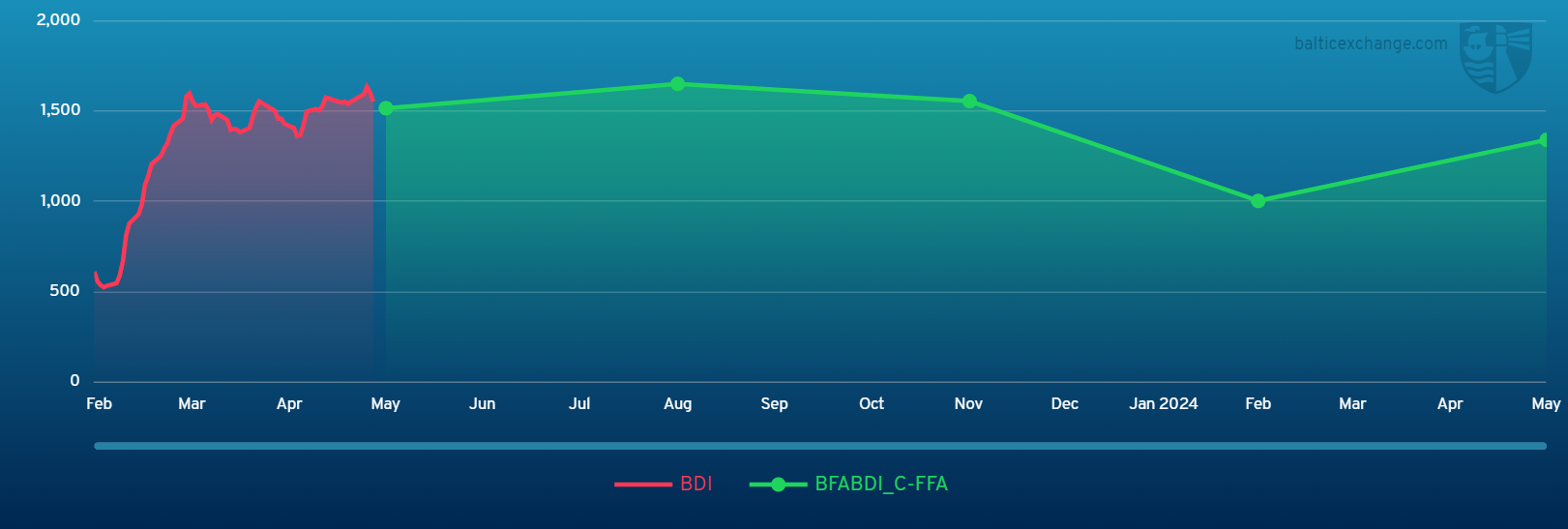

Chart shows Baltic Dry Index (BDI) during May 13, 2022 to May 12, 2023

Baltic Forward Assessment for BDI

In March 2018 the BDI was re-weighted and is published using the following ratios of time charter assessments: 40 percent capesize, 30 percent panamax and 30 percent supramax. The information is provided by a panel of international shipbrokers.

(Source: The Baltic Exchange, edited by Niu Huizhe with Xinhua Silk Road, niuhuizhe@xinhua.org)

A single purchase

A single purchase