BEIJING, June 2 (Xinhua) -- The Baltic Exchange has published its weekly report of the dry and tanker markets for May 25-29, 2020 as below:

Capesize

A sober end to the week, with the market seemingly ready for the weekend. After a steady week of rate declines a small flurry of Atlantic business - combined with a little activity in the Pacific - managed to end the week up a tick. While a bottom may have been found, there’s no bull flags as the Capesize 5TC posted up 141 to settle at a low $3369. While most global routes - both on time-charter and voyage - varied little from opening levels at the beginning of the week, the Pacific Round C10 looks to have fared the worst dropping from $6563 to close the week at $4581. Bunker levels have once again been on a downward trajectory ending the week, although high versus low sulphur spreads are said to have widened. The Pacific C5 West Australia to China route settled the week at $4.123 - which equates to a little less than $3000 per day in earnings for a Capesize vessel - and leaves the market still trading well below operating cost levels.

Panamax

Various holidays at the start of the week failed to dampen the Panamax market, with significant gains made in index values. Transatlantic volume was thinner but positive sentiment radiated from good volumes and better rates on the fronthaul trips. South America remained the market’s driving force, with the second-half June arrival window absorbing several vessels throughout the week. Typically, some of the well described units were able to achieve in the region of $12,500+$250,000 mark arrival at South America. The P6 route gained value and was pegged well into the $9,000’s delivery Singapore by the end of the week, impacting positively on south positions in the Pacific basin. The week in Asia started slowly due to the holiday in Singapore. However, solid levels of demand from Indonesia and Australia soaked up tonnage and rates held steady throughout the week, with index tonnage yielding around the $7,250 mark.

Ultramax/Supramax

A short week with activity levels a little slower than the previous week. Period activity surfaced, which some saw as a positive move. There was a 60,000dwt open north China fixing short period in the high $9,000s. Whilst from the Atlantic, a 58,000dwt open Mediterranean fixed three to five months Atlantic trading at $8,500. Activity remained subdued from the US Gulf area with limited fresh enquiry. From east coast south America, tighter prompt tonnage helped rates. A 61,000 open up river Plate fixed at $11,250 - plus $125,000 ballast bonus for a trip to south east Asia. A mixed bag from the Asian arena, rates remained firm from the Indian Ocean. A 55,000dwt fixing delivery South Africa trip Singapore-Japan at $11,500 plus $150,000 ballast bonus. In south east Asia rates traded sideways as the week ended, with a 58,000 fixed from Vietnam via Australia redelivery Singapore-Japan at $7,000. There was more activity on nickel ore business with a 57,000dwt open CJK fixing in the mid $7,000s.

Handysize

A short week with east coast South America and the Pacific lending strong support for Handysizes. Slightly more cargoes circulated from the continent and Mediterranean, whilst owners showed some resistance towards the end of the week. Despite the US Gulf remaining weak, positive sentiment from other key regions pushed the rates higher and led the BHSI with a continued improvement. A 36,000dwt was fixed from Liverpool for a trip to Darrow at $4,000. A 28,000dwt open Myanmar end May was fixed at $6,750 for a trip via east coast India to China. A 39,000dwt, meanwhile, was fixed from Esperance for a grain trip to China at $10,000. On the period front, a 33,000dwt open in the Philippines in end June/beginning July was fixed on index-linked basis for about seven / nine months worldwide redelivery at 88 percent of BSI58 10TC.

Clean

Overall it was another slow week in the Middle East Gulf, although levels appear to be stabilising with rates for 75,000 mt to Japan hovering around WS115/120 region. Likewise, the status quo is being maintained on the LR1s with rates assessed close to WS130 level for Japan discharge. Owners plying the 37,000mt UKC to USAC trade saw a good volume of enquiry. Rates recovered from low WS100s to WS140, which was agreed by Exxon on Torm tonnage. Brokers feel there is potential for further improvement here. It was a similar story in the 38,000mt backhaul trade from US Gulf to UKC, which saw a flurry of activity at end of last week ahead of the Memorial Day holiday in the USA. This led rates to firm from WS80 a week ago and the momentum was maintained with rates now sitting in the mid WS90s. The 30,000mt clean cross-Med trade continued to firm, gaining over 20 points a week ago. Levels were broadly maintained with west Med loading now paying in the low/mid WS150s with a Skikda load covered at WS 152.5. Cargoes loading in the east Med were fixed as high as WS 172.5/175, with Black Sea load paying around WS185.

VLCC

Improved volumes have tightened the supply of vessels, enabling owners to regain some of the recent lost ground. The Middle East Gulf sector saw rates flat in the first half of the week, then progressive rises midweek with rates for 270,000mt to China jumping from WS50 to WS60 - and then mid WS60s. They now appear for the time being to have settled around WS65-67 region. Rates for 280,000mt to USG via the cape/cape route are now assessed five points higher than a week ago at WS36. In West Africa rates recovered 12 points to WS 64/65 level. In the Gulf of Mexico, although there has been limited activity, rates for 270,000mt USG/China rates are now assessed at just over $6.5 million, up about $750,000.

Suezmax

Rates in this sector in the West remained flat as 130,000mt Nigeria/UKCont are still at WS72 and 135,000mt Black Sea/Med at WS73. In the 140,000mt Middle East/Med market, rates have eased a further 4 points and now rest around WS32.

Aframax

There was more downward pressure on this sector. In the 80,000mt Ceyhan/Med route, rates slipped another eight points to WS80. In Northern Europe, 80,000mt Cross-North Sea lost another 15 points to WS92.5 and 100,000mt Baltic/UKC is now at WS75, 18 points lower than last week. Across the Atlantic yet more pain for owners as rates for 70,000mt Carib/USG were weakened by another 15 points to WS75. The market for 70,000mt USG/ARA is down around 13 points at WS72.5-75 level.

Headquartered in London and a subsidiary of the Singapore Exchange (SGX), the Baltic Exchange publishes a range of indices and assessments which provide an accurate and independent benchmark of the cost of transporting commodities and goods by sea. These include the Baltic Dry Index (BDI), the dry bulk shipping industry's best known indicator. Published daily since 1985, this provides a snapshot of the daily spot market earnings of capesize, panamax and supramax vessel types on the world's key trading routes.

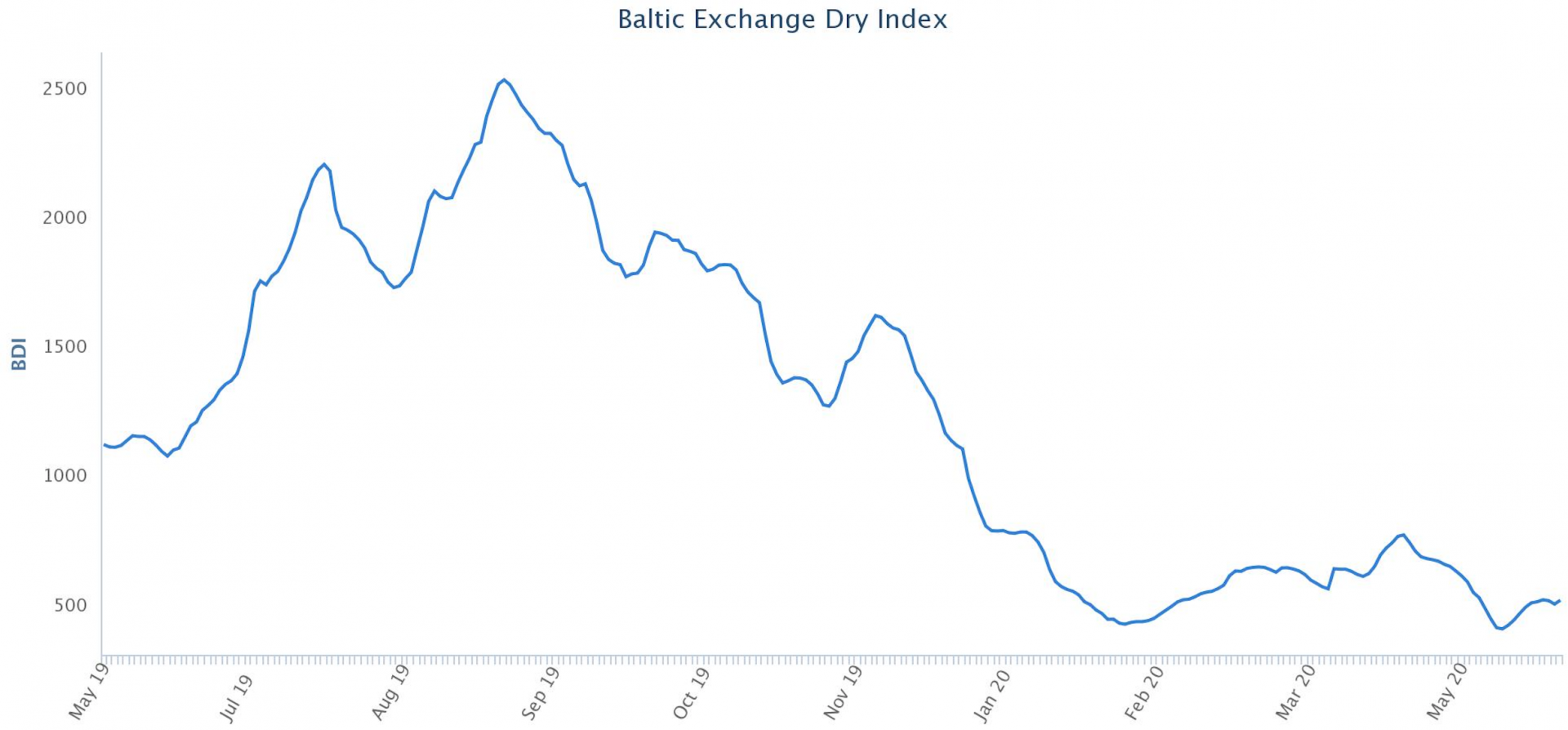

Chart shows Baltic Dry Index (BDI) during May 19, 2019 to May 29, 2020

In March 2018 the BDI was re-weighted and is published using the following ratios of timecharter assessments: 40 percent capesize, 30 percent panamax and 30 percent supramax. The information is provided by a panel of international shipbrokers.

(Source: The Baltic Exchange, edited by Niu Huizhe with Xinhua Silk Road, niuhuizhe@xinhua.org)

A single purchase

A single purchase