BEIJING, April 20 (Xinhua ) -- EU authorised benchmark administrator the Baltic Exchange has partnered with air cargo pricing publisher TAC Index Company of Hong Kong to tap into air cargo market.

In a news release, the Baltic Exchange said it will partner with TAC to provide new regional general air cargo rate assessments.

TAC's Regional General Air Cargo Indices will be rebranded as the Baltic Air Freight Index (BAF Index) powered by TAC Index and come under the governance of Baltic Exchange Information Services Limited (BEISL). TAC Index will act as the Calculating Agent, it said.

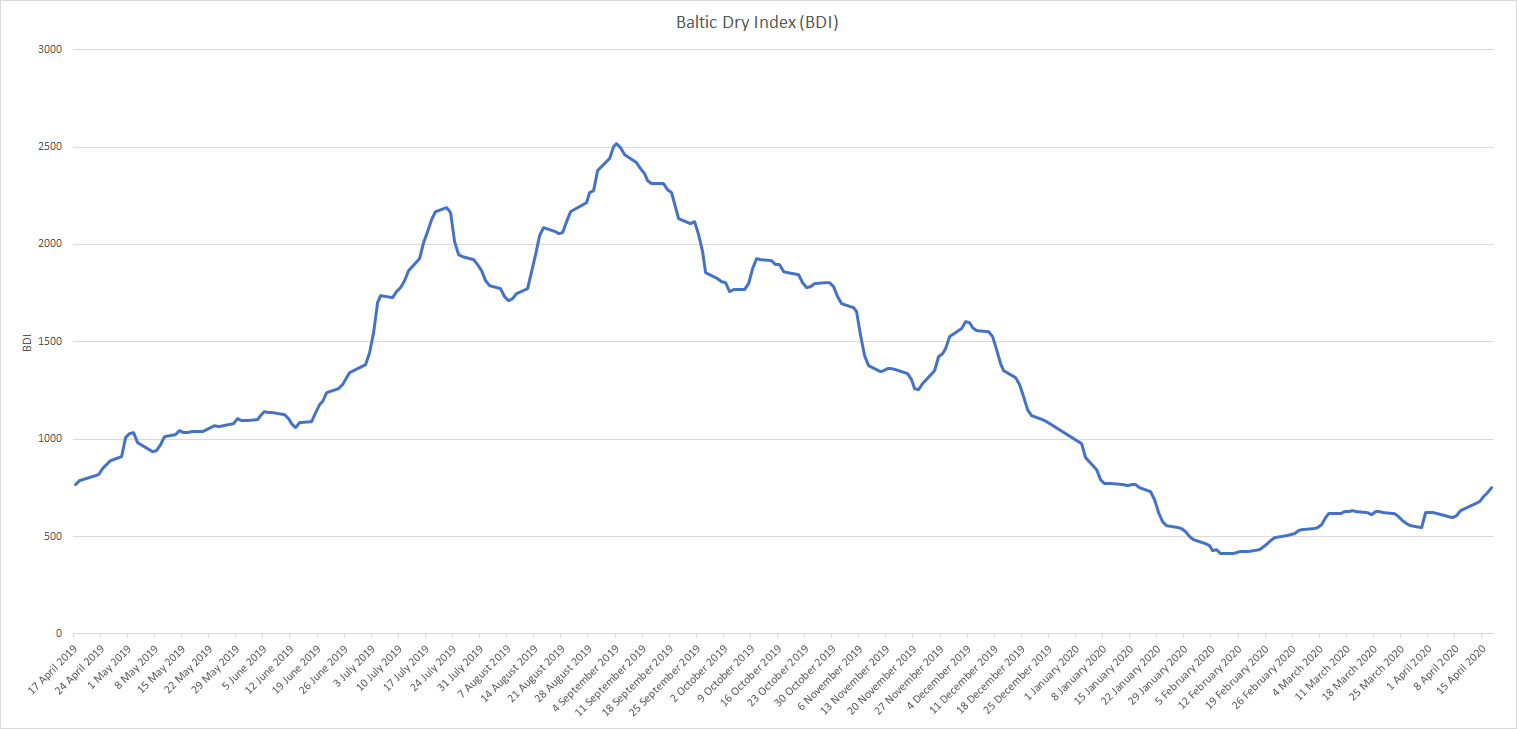

Headquartered in London and a subsidiary of the Singapore Exchange (SGX), the Baltic Exchange publishes a range of indices and assessments which provide an accurate and independent benchmark of the cost of transporting commodities and goods by sea. These include the Baltic Dry Index (BDI), the dry bulk shipping industry’s best known indicator. Published daily since 1985, this provides a snapshot of the daily spot market earnings of capesize, panamax and supramax vessel types on the world’s key trading routes.

Chart shows Baltic Dry Index (BDI) during Apr.17, 2019 to Apr.15, 2020

In March 2018 the BDI was re-weighted and is published using the following ratios of timecharter assessments: 40 percent capesize, 30 percent panamax and 30 percent supramax. The information is provided by a panel of international shipbrokers.

The Baltic Exchange also publishes weekly report of the dry and tanker markets and below is the weekly report for April 13-17, 2020.

Dry Bulk Report

Capesize

This week was the strongest period seen for the Capesize market in several months. All routes globally succumbed to improved sentiment, albeit the Pacific Basin lagged somewhat, with the West Australia to China C5’s usual flow proving resistant. Ending the week on a high, the C5 route added +0.232 to settle at $4.918. The Pacific round voyage route C10 opened the week at a premium to the Transatlantic C8. However, this was quickly surpassed, as the Atlantic Basin saw a lifting of cargo levels to available tonnage as several fixtures posted stronger returns. The Atlantic C8 stands at $10,075 to the Pacific C10 at $8,500. The Atlantic Basin was ignited predominantly on fronthaul C9 and ballaster routes back to the Far East. While fundamentals don't appear drastically changed the push-pull between the Basins is now in motion, adding volatility and opportunity at above OPEX levels. The Capesize 5TC opened the shortened week at $6,762 to close out at $9,875.

Panamax

Easter holidays impacted the market last week, with only minor movements in the Baltic Panamax Index (BPI). Baltic mineral trades proved active, so too were South American fronthaul grains, particularly from North Coast South America (NCSA). Rates crept up a little from NCSA, with $13,350 plus $335,000 ballast bonus being paid for an 82,000dwt ship. Rates for Baltic round trips generally hovered around the $5,000 mark, but activity elsewhere was limited. In the Pacific, grain demand from the North Pacific started brightly. An 82,000dwt ship achieving $8,250 for a trip via the North Pacific, back to Singapore-Japan. However, generally demand in the region eased as the week went on, in turn weakening rates in the process. Some brief activity this week in the period market included a well described 82,000dwt ship agreeing to $10,850 for one year’s period.

Supramax/Ultramax

With the ongoing Covid-19 situation the market remained bleak, with a lack of fresh enquiry and tonnage readily available in most areas. Period activity was sparse, but a 60,000dwt ship, open Campha, was linked to about six to nine months trading at $8,500. From the Atlantic, East Coast South America lacked impetus, while from the US Gulf, an Ultramax was rumoured fixing in the mid $12,000s for trips to the Far East. From the Continent, a 56,000dwt ship was fixed delivery Baltic trip, redelivery East Mediterranean, in the mid $5,000s. Little encouragement was seen from Asia as well. A 56,000dwt vessel fixing delivery Philippines trip, via Australia, redelivery Singapore-Japan, at $5,000. A 52,000dwt ship fixing an Indonesia coal run to China at $4,400. There were a few green shoots appearing from the Indian Ocean, with a 61,000dwt vessel covering a trip delivery West Coast India, via Aqaba, redelivery East Coast India, at $6,500.

Handysize

A short week with the overall Baltic Handysize Index (BHSI) falling below 300 after the Easter weekend. By the end of the week, the BHSI had declined to the same level last seen in April 2016. Little fresh cargo emerged in key areas, with sentiment remaining negative throughout the week. Whilst the tonnage supply was getting more excessive in both Basins, brokers saw limited market information or movement, suggesting more pressure on owners to get their vessels fixed any closer to the level of last done.

Tanker Market Report

VLCC

Activity in the Middle East has slowed while owners await the May program. Rates have continued to come under downward pressure and WS167.5 was agreed for 270,000mt to the East, but we understand this has now failed. Currently the market is assessed at around WS150, with owners pinning their hopes on renewed activity next week when May cargoes appear. 280,000mt to the US Gulf via the Cape to Cape routing is rated at close to mid WS90s. This contrasts with just over WS100 at the start of the week. There was weaker sentiment also in the market for 260,000mt. West Africa to China saw rates soften from WS143 at the start of the week to around WS137.75. This was before Vitol reportedly took a Koch relet at an improved WS146 level. Enquiry from the US Gulf to China was negligible, although HOB failed a Mexico to Korea run at $15 million and the route is today assessed at just below $14 million.

Suezmax

The market for 130,000mt West Africa to the UK-Continent had an uneventful week, with rates maintained at WS130. A similar scenario ensued in the 135,000mt Black Sea to Mediterranean trade, with rates hovering between WS132.5/135 region. The 140,000mt Basrah to Mediterranean route started the week at WS105 before dipping down to WS100 for a run to Turkey. However, rates then recovered, with Shell taking Trafigura tonnage at WS115.

Aframax

Rates for 80,000mt Ceyhan to the Mediterranean, which eased considerably in the run up to Easter, stabilised in the mid to high WS90s. However, with the subsequent improvement in the North, owners will be hoping this will filter through to the Mediterranean. 80,000mt Cross-North Sea had been fixed at between WS107.5/110 before a surge of activity. Around 20 ships on subjects in the last 24 hours saw rates shoot up, with the market now evaluated at around WS140. Likewise, in the 100,000mt Baltic to UK-Continent trade, which initially slipped 2.5 points to WS90, rates have rebounded. Last seen here was Total fixing at WS115, while a Murmansk cargo went at WS126.5. Across the Atlantic the market for 70,000mt Caribbean to the US Gulf regained 2.5 points to sit now at WS105 region, but with potential to firm further. The 70,000mt US Gulf to UK-Continent-Mediterranean is following a similar pattern, with rates nudging up from WS95 to low WS100s.

Clean

For owners trading in the clean market it was a prosperous week all round. The market in the Middle East Gulf to Japan trade for 75,000mt gained 32.5 points to WS240. LR1s also saw renewed activity, with rates gaining 27 points to WS235. This has reportedly been agreed by BP and brokers feel there is potential to firm further. In the 37,000mt UK-Continent to the US Atlantic Coast trade rates are now nudging WS160, having started the week at WS140. Similarly rates in the 38,000mt backhaul trade from the US Gulf to UK-Continent firmed 10 points to just over WS105. The 30,000mt clean cross-Mediterranean market recovered 15 points to around WS207.75, with the Black Sea continuing to pay 40 plus points over the Mediterranean.

(Source: The Baltic Exchange, edited by Niu Huizhe with Xinhua Silk Road, niuhuizhe@xinhua.org)

A single purchase

A single purchase