BEIJING, Nov. 6 (Xinhua) -- The Baltic Exchange has published its weekly report of the dry and tanker markets for October 30-November 3, 2023 as below:

Capesize

The capesize market started the week on a sluggish note with the PPA conference in Perth creating a quieter atmosphere, leading to reduced trading volumes in the Pacific and a softening of rates. Despite some stabilisation in conditions midweek, the Pacific market remained uninspiring with limited activity and rates on the C5 route dipped. However, as the week drew to a close, there was a slight uptick in volumes and rates on C5 have nudged back up by 45 to 50 cents. In the Atlantic, conditions experienced a slight downturn in the early part of the week from south Brazil to West Africa and the Far East. However, towards the end of the week, brokers have reported a positive shift in the market, with bids on the rise, leading to a minor rally. The north Atlantic showed a favourable outlook towards the end of the week, with stronger fronthaul fixtures concluded and expectations of an uptick in the Trans-Atlantic market due to tight tonnage supply. Overall, it was a challenging week for the capsize market, with brief moments of stability that ultimately culminated in a modest rally as the week drew to a close. The BCI 5TC gained about $350 over the week, closing at $17,690.

Panamax

A rather protracted affair as the week started with limited demand in both basins. However, as the week came to a close, increased mineral demand saw increased activity in the north Atlantic, which offered support. A slight caveat being limited fresh enquiry appearing from the south Atlantic adding further downward pressure on ballasting vessels. An 81,000 dwt fixing delivery Passing Muscat for a trip via EC South America redelivery Passing Muscat Outbound at $13,500. From Asia, it was a mixed bag with little enquiry to begin as rates struggled to gain traction. Towards the end of proceedings, there was a slight improvement on demand but with little excitement from South America, any rate increase was limited. An 82,000 dwt fixed delivery Philippines for a trip via Indonesia redelivery India at $11,800. Period action was limited but an 81,000 dwt open January 2024 was heard to have been fixed for 12 months trading in the mid $15,000s.

Ultramax/Supramax

A poor week overall for the sector as demand remained low in both basins. The only upside was seen in the Atlantic from the US Gulf were fresh enquiry combined with a shortage of tonnage saw rates push up. A 63,000 dwt delivery US Gulf trip to India with petcoke at $33,750. Elsewhere in the Mediterranean/Continent region, opinions differed but some felt fresh demand was surfacing. In Asia, with very little fresh demand from both the north and south, sentiment remained poor. A 58,000 dwt open north China fixing a trip via Indonesia to SE Asia in the mid $8,000s, whilst a 56,000 dwt open Philippines fixed a trip via Indonesia redelivery Thailand at $9,000. Limited demand was seen from the Indian Ocean, but a 63,000 dwt reportedly fixed delivery South Africa redelivery China at $18,500 plus $185,000 ballast bonus. Little was heard on the period front, with a 60,000 dwt open Singapore fixed for a period up to minimum 10 November 2024/maximum 10 January 2025 at $12,500.

Handysize

A week of general negativity across the handy sector with limited cargo availability and growing tonnage lists across both basins. The lone region of positivity was in the US Gulf and US east coast where tonnage was said to be limited, with a 35,000 dwt fixed for a trip from Panama City to the UK-Continent range at $20,000. In the south Atlantic, pressure remained on owners and a 39,000 dwt was rumoured to have been fixed basis delivery Upriver Plate to the Caribbean at $16,000 whilst a 38,000 dwt was fixed from Santos to Morocco with a cargo of sugar at $15,000. The Continent and Mediterranean were said to have been relatively inactive partially due to widespread holidays across Europe this week. In Asia, activity was stifled due to a lack of cargo availability and a 38,000 dwt was fixed from Singapore via Dampier to Taipei, China with a cargo of salt at $7,000 and shows signs of continued negativity in the coming days.

Clean

LR2

LR’s in the MEG have taken a heavy re-correction down this week in terms of freight. The 75Kt MEG/Japan TC1 index lost 25.78 points to WS146.11. Similarly on a 90kt MEG/UK-Continent TC20 run nearly 10% of the value was lost down to the current mark at a shade over $4m.

West of Suez, Mediterranean/East LR2’s on TC15 have again been inactive this week, with the index subsequently dropping from $3.475m to $3.27m.

LR1

In the MEG, LR1 freight levels also came off this week, although to a lesser extent than the LR2’s. The 55kt MEG/Japan index of TC5 dipped from WS167.5 to WS154.69 and on the 65kt MEG/UK-Continent of TC8 lost about $200,000 to $3.34m.

On the UK-Continent, the 60Kt ARA/West Africa TC16 index returned back to WS175 gradually over the course of the week with little open market fixing to report.

MR

MR’s in the MEG continued on their downward trajectory this week. The 35kt MEG/East Africa TC17 index, as a result, dipped to the tune of 17.14 points to WS210. This took the Baltic round trip TCE for the run under $20,000/day mark for the seventh time this year.

UK-Continent MR’s continued to be active this week, with available tonnage thinned and steady off market fixing bolstered firming. The 37kt ARA/US-Atlantic coast of TC2 added 10.25 points to be currently pegged at WS180. TC19 (37kt ARA/West Africa) also optimistically hopped up to a current level of WS191.88 (+11.25).

The USG MR’s have been sitting on the fence this week, with just enough happening in the open market to prevent rates from dropping off. TC14 (38kt US-Gulf/UK-Continent) lingered around the WS112.5-115 level whilst 38kt US-Gulf/Brazil on TC18 hovered in the WS197.5-200 region. A 38kt US-Gulf/Caribbean TC21 run has followed suit but ultimately added $30,000 to the index to $703,571.

The MR Atlantic Triangulation Basket TCE climbed for the second week by $817 to $24,003.

Handymax

In the Mediterranean, Handymax’s remained balanced, with rates holding flat around the WS195 mark all week. In northwest Europe, the TC23 30kt Cross UK-Continent shed just under 10 points to WS164.17.

VLCC

The market turned upwards this week across the board, peaking on Wednesday and then steadying. The rate for 270,000 mt Middle East Gulf to China rose 12 points week-on-week to WS71.83, corresponding to a daily round-trip TCE of $51,290 basis the Baltic Exchange’s vessel description. The 280,000mt Middle East Gulf to US Gulf trip (via the cape/cape routing) is now assessed six points higher than last Friday at WS39.44.

In the Atlantic market, the rate for 260,000 mt West Africa/China rose 11 points to WS74.10 (which shows a round voyage TCE of $54,551/day), while the rate for 270,000 mt US Gulf/China is $211,111 firmer at $10,238,889 ($45,884/day round trip TCE).

Suezmax

Suezmaxes in West Africa had another progressive week until Thursday, with sentiment now a little weaker. The rate for 130,000 mt Nigeria/UK Continent has risen eight points over the week to WS161.36 (a daily round-trip TCE of $76,743), having peaked at WS164 on Wednesday. In the Mediterranean and Black Sea region, the 135,000 mt CPC/Med route, with the assistance of a very firm Aframax market, has risen another 19 points since last Friday to WS167.3 (showing a daily TCE of $86,989 round-trip). In the Middle East, the rate for 140,000mt Middle East Gulf to the Mediterranean climbed nine points to just shy of WS90.

Aframax

In the North Sea, the rate for the 80,000 mt Cross-UK Continent route has gradually slackened this week, losing 15 points since last Friday, to WS199.64 (showing a round-trip daily TCE of $90,970 basis Hound Point to Wilhelmshaven). In the Mediterranean market, the rate for 80,000 mt Cross-Mediterranean continued upwards, adding another 32 points, to WS252.89 (basis Ceyhan to Lavera, that shows a daily round trip TCE of $96,603).

On the other side of the Atlantic, rates were steady until Thursday, when a build-up of available tonnage and thereby weakening sentiment, pulled rates back down. The rate for 70,000 mt east coast Mexico/US Gulf has fallen 38 points since last Friday to WS270 (a daily round-trip TCE of $88,615) and the 70,000 mt Covenas/US Gulf rate tumbled 33 points to WS259.06 (a round-trip TCE of $77,748/day). The rate for the trans-Atlantic route of 70,000mt US Gulf/UK Continent has slipped 10.5 points since a week ago to WS259.38 (a round trip TCE basis Houston/Rotterdam of $75,129/day).

LNG

While the LPG market has been significantly rocked after the Panama Port Authority cull on crossings per day, the LNG market has reacted a little more mutely. The affect is still to be absorbed but the big increase in waiting times, or potentially much higher tonne miles via the Cape, will no doubt affect routing and pricing. As the LNG market has shifted focus towards Cont deliveries from the US, there have been fewer Panama canal transits to be affected, but it will not go unnoticed.

Rates have been flat despite the reported flurry of fixtures this week and the reduction of available ships. Reports of cargoes working out to December laycans in both the Med and Middle East has not pushed rates much, but all three routes closed positively. BLNG1g Aus-Japan rose $4,943 to finish at $144,644, while the Atlantic BLNG2g US-Cont rose to $162,179 and BLNG3g US-Japan finished at $181,632. Period rose for multi-month deals with the one-year and three-year terms flat/soft, while many players take stock over what happens in the short term.

LPG

A quiet week on the LPG Eastern market with few fixtures reported. November is not shaping up to be overly busy either and with balanced tonnage vs. enquiry rates look stable. We have seen a rise for BLPG1 on the week with Ras Tanura-Chiba rising $10 overall to close at $141.571 while TCE earnings moved up to finish at $128,239 for a round voyage trip.

BLPG2 and BLPG3 have both been more active but rates are mainly buoyed on the recent news coming out of Panama. With one VLGC ship reportedly paying a whopping $2,800,000 for a slot to go through and the Panama Canal port authority reducing daily passings dramatically, there is upset and volatility on the horizon. Tight tonnage supply against opening of the arb is causing stiff rises. BLPG3 Houston-Chiba jumped $35.571 on the week to finish at $235, while TCE earnings grew as well to $141,859. Houston-Flushing BLPG2 has fallen a little behind but still managed a $16.6 rise to close at $129.4 with TCE earnings for a round trip at $155,657.

Headquartered in London and a subsidiary of the Singapore Exchange (SGX), the Baltic Exchange publishes a range of indices and assessments which provide an accurate and independent benchmark of the cost of transporting commodities and goods by sea. These include the Baltic Dry Index (BDI), the dry bulk shipping industry's best known indicator. Published daily since 1985, this provides a snapshot of the daily spot market earnings of capesize, panamax and supramax vessel types on the world's key trading routes.

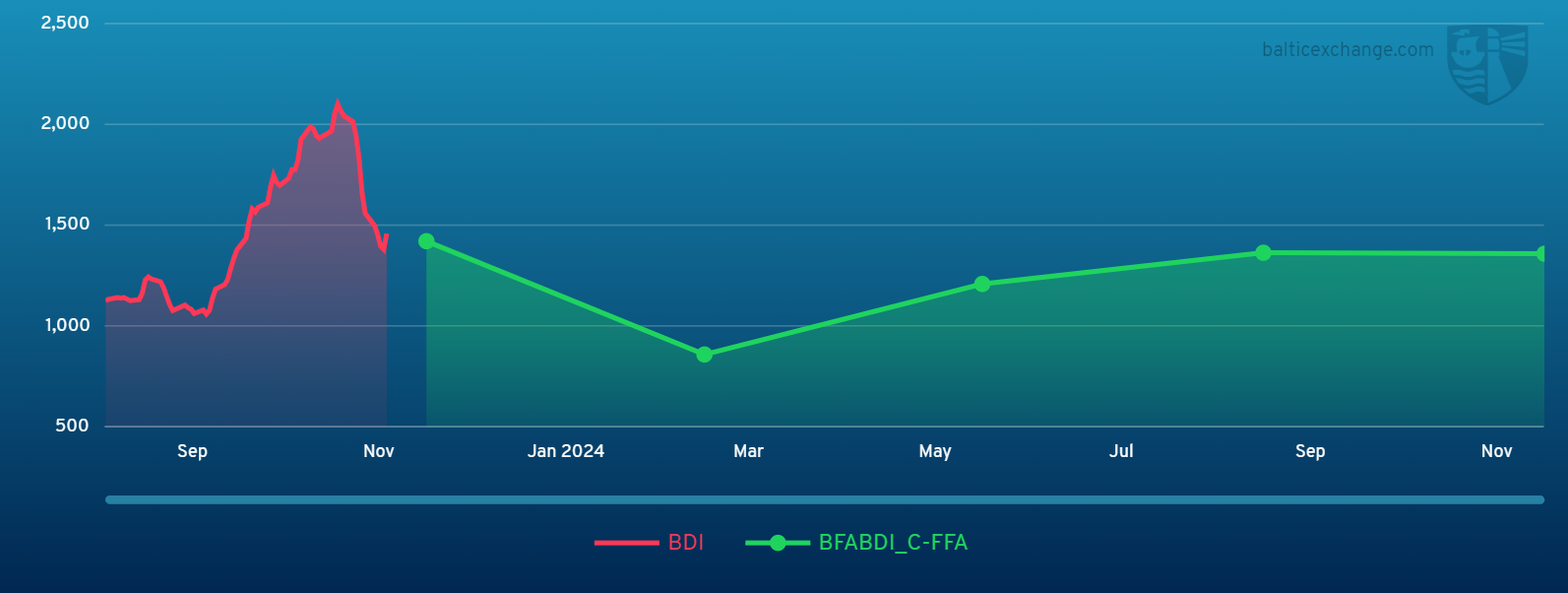

Chart shows Baltic Dry Index (BDI) during Nov. 3, 2022 to Nov. 3, 2023

Baltic Forward Assessment for BDI

In March 2018 the BDI was re-weighted and is published using the following ratios of time charter assessments: 40 percent capesize, 30 percent panamax and 30 percent supramax. The information is provided by a panel of international shipbrokers.

(Source: The Baltic Exchange, edited by Niu Huizhe with Xinhua Silk Road, niuhuizhe@xinhua.org)

A single purchase

A single purchase