BEIJING, June 5 (Xinhua) -- The Baltic Exchange has published its weekly report of the dry and tanker markets for May 29 - June 2, 2023 as below:

Capesize

The capes have faced a challenging week, marked by holiday disruptions. Despite a slow start to the week, there has been no shortage of cargo in both the Atlantic and Pacific regions. However, both markets have been grappling with an excess supply of tonnage, which has been putting downward pressure on the mar ket. By the middle of the week, there was a significant downturn in sentiment and the overall timecharter index lost 33 pct to close at $9,254. The North Atlantic saw a flurry of fixing at considerable discounted rates, and conditions continued to slide further in the Pacific. As the holiday in Singapore approached towards the end of the week, there was an uptick in the level of activity from West Australia to China, and the market started to find some stability. The Atlantic, on the other hand, still appears to be under pressure.

Panamax

For another successive week, corrections were seen in the Panamax market. Despite better demand week-on-week, it was again met by a sea of prompt tonnage along with an increasing ballaster count. The Atlantic appeared predominantly grain centric with minimal mineral activity seen towards the latter part, several EC South America front haul deals concluded mid-week, delivery Aps loadport for end June arrival window, the mean average rate for same hovered around the $15,000+$500,000-mark basis for 82,000dwt types. Asia saw a relative rise in volume week-on-week ex Indonesia and Australia. However, this appeared to have very little impact with a desolate NoPac market and ships returning to the market following quick trips in recent weeks. An 82,000dwt delivery China agreed $7,250 for a coal trip via Australia delivery Japan. A limited week of period activity, although an 82,000dwt delivery South China achieved $14,000 for one year employment.

Ultramax/Supramax

The only saving grace for the sector was it was a short week for many, with widespread holidays at the beginning and end. Both basins suffered from an oversupply of prompt tonnage with fresh enquiries being snapped up by owners securing employment. The Atlantic saw strong declines in both the US Gulf and South America regions, including a 56,000dwt fixing delivery Mobile for a trip to the Black Sea at $12,000. Whilst from EC South America, a 63,000 fixed delivery Itaqui for a trip to Singapore-Japan at $13,100 plus $310,000 ballast bonus. Little excitement across the ‘Pond’, a 58,000dwt fixing a trip from Oran to West Africa at $10,500. Asia fared little better, with demand from Indonesia dropping and little in the way of backhaul cargo rates were under hefty downward pressure. A 56,000dwt open CJK fixed a trip via Indonesia redelivery WC India at $4,250. Elsewhere a 53,000dwt was heard fixed delivery Chittagong trip via Indonesia redelivery India at $3,000.

Handysize

Another short week for many but a general lack of activity and a lack of fresh enquiry dominated the handy sector across both basins. In East Coast South America, a 32,000dwt fixed from Paranagua to the US East Coast with an intended cargo of Sugar at $10,950, whilst a 33,000dwt had fixed basis delivery Fazendinha to Norfolk with an intended cargo of grains at $14,750. Meanwhile, a 37,000dwt fixed from Vila Do Conde to the Mississippi with an intended cargo of alumina at $15,000. On the US East Coast, a 37,000dwt fixed from Savannah to the Continent intention Rotterdam with an intended cargo of wood pellets at $8,000. In Asia, a 34,000dwt fixed from Hire to Southeast Asia at $7,000 and a 32,000dwt open spot in Onsan fixed for a short trip within the region at $5,000. A 36,000dwt opening in Laemchabang on 8 June fixed a trip to Australia at $7,000.

Clean

LR2

MEG LR2’s have suffered from relatively little activity this week, exacerbated by a short week in Singapore. Freight levels have been level with TC1 stable in the mid WS140’s and a trip west on TC20 dipped $178,000 to $3,942,000.

West of Suez, Mediterranean/East LR2’s look to have taken a similar trajectory to the MEG. TC15 is currently pegged at $3,066,667 following a $3,250,000 deal failing and $3,100,000 widely reported on subjects.

LR1

In the MEG, LR1’s have taken a small hit similar to their larger sisters. TC5 dropped 12.86 points to WS147.14 and a TC8 voyage heading west shed $250,000 to $3,008,000.

On the UK-Continent, TC16 held flat at WS134-135 but due to the bunker prices the Baltic TCE has ticked over the $25,000 /day round trip.

MR

MEG MR’s have been retested down again this week. Subsequently the TC17 index has dropped from WS296.43 to WS272.86. At these levels the run is still returning a Baltic TCE of $34,000/day round trip.

UK-Continent MR’s showed good momentum this week. Both TC2 and TC19 climbed 15 points to WS197.78 and WS208.57 respectively off the back of less available tonnage.

USG MR’s saw market direction return downward this week following a short week after Memorial Day activity has been limited. TC14 came off 32.5 points to WS145.31 and TC18 dropped 38.34 points to WS272.86. A run to the Caribbean on TC21 took a $190,000 (20 pct) hit down to $735,000.

The MR Atlantic Triangulation Basket TCE dropped from $36,010 to $32,121.

Handymax

Mediterranean Handymax’s continued to trundle along at WS135 for a TC6 run with just enough activity to prevent further decline.

Up on the UK-Continent, TC23 similarly to the Mediterranean hovered in the WS130-135 region all week.

VLCC

Another quiet week has led to rates slipping again. In the Middle East the rate for 270,000 mt Middle East Gulf to China was eased about 2.5 points to WS44.95 (a round trip TCE of $22,300 per day basis the Baltic Exchange’s vessel description), while the 280,000 mt Middle East Gulf to US Gulf trip (via the cape/cape routing) the rate is now assessed half a point lower at 31.28.

In the Atlantic market, the rate for 260,000 mt West Africa/China dropped 2.7 points to WS47.15, which shows a daily round voyage TCE of $26,200. In the US Gulf arena, while the market has been quiet for US exports, an influx of Brazil export enquiry has kept rates to minimal reductions. The rate for 270,000 mt US Gulf/China is now assessed $416,667 lower than a week ago at $7,600,000 ($30,600 per day round trip TCE, about $3,000 less than last Friday).

Suezmax

The Black Sea and Mediterranean markets continued on a downward trend with the rate for 135,000 mt CPC/Med shedding another eight points to WS121.28 (a round trip TCE of just below $53,000 per day).

In the Atlantic region, the West African market was quiet again, and the US Gulf arena was not attracting vessels away either. The rate for 130,000 mt Nigeria/Rotterdam tumbled 12 points to WS101.75 (a round trip TCE of $49,100 per day). In the Middle East, the rate for 140,000 mt Basrah/Lavera eased again, losing four points to WS65.

Aframax

In the North Sea, the rate for the 80,000 mt Hound Point/Wilhelmshaven lost six points to settle around the WS147.5-150 level (showing a round-trip daily TCE of $54,500).

In the Mediterranean, despite a very busy Libya programme, the rate for 80,000 mt Ceyhan/Lavera fell 21 points to WS176 (a daily round trip TCE of about $58,900).

Across the Atlantic, the Stateside Aframax, after a short week with very little reported activity, has weakened rates. The rate for 70,000 mt East Coast Mexico/US Gulf dropped a little over 30 points WS167.5, which shows a TCE of about $45,500 per day round trip. For the 70,000 mt Covenas/US Gulf trip the rate slackened almost 26 points to WS156.5 representing a round trip TCE of $38,200 per day, and for the trans-Atlantic route of 70,000 mt US Gulf/Rotterdam the rate is now nearly 32 points softer than last Friday at WS148 (a round trip TCE of $35,500 per day).

LNG

Without many actual market fixtures taking place, the LNG spot market did see increased rates across the board on all three routes. With the ARB opening expectation, there will be an influx of cargoes and opportunities for traders to begin moving cargo. This has created some uncertainty in the list with ships shown being removed or held back on the expectation that traders will create internal program, which further helps the rate gain. The greatest increase was seen in BLNG3g as expected from last week where a rise of $11,740 per day gave a Round Voyage rate of $48,531, while BLNG2g Houston-Cont saw $7,611 rise to a Round Voyage rate of $40,236. It would be pre-emptive to say this rise shall continue, as we would need to see physical fixtures to support it, but brokers are optimistic and feel that the next few months should see the spot LNG brought out of the doldrums of the last quarter.

For BLNG1g Aus-Japan a modest rise of $2,981 gave us an index Round Voyage at $40,351 and, although focus has been on what improvements can be made in the West on rates, the East sees similar interest from market participants. Rates went positive in a quick turnaround from the end of the previous week where a drop of a few thousand pre-empted brokers to adjust their opinions and look at the positives in market macro-economics.

LPG

The Eastern LPG market has seen a slight boom this week with a rise of $8 from $107.29 to close at $115.429. This is driven mainly by a good steady stream of cargoes and a tighter tonnage list going into mid-June. It is a stronger market by far than the same time last year, when heading into the summer rates were $25-35 lower than the levels we have seen in 2023 and the levels we are achieving running into summer weren’t really repeated until the stronger winter market of 2022. Strong footing, higher sentiment and healthy earnings will keep BLPG1 looking strong.

Out in the West it was a different story with a more subdued fixing the rates came off slightly. BLPG1 Houston-Chiba fell by $1 to close at $156.143 with a TCE daily earnings of $84,576, while BLPG2 Houston-Flushing saw little movement at all and finished $0.4 down at $95.2 with a daily TCE earning of $111,082. Few fixtures kept sentiment and optimism low and with delays still in Panama there could have been expectation of a rise but with ships available for fixing for the end of June and early July this did not materialise.

Headquartered in London and a subsidiary of the Singapore Exchange (SGX), the Baltic Exchange publishes a range of indices and assessments which provide an accurate and independent benchmark of the cost of transporting commodities and goods by sea. These include the Baltic Dry Index (BDI), the dry bulk shipping industry's best known indicator. Published daily since 1985, this provides a snapshot of the daily spot market earnings of capesize, panamax and supramax vessel types on the world's key trading routes.

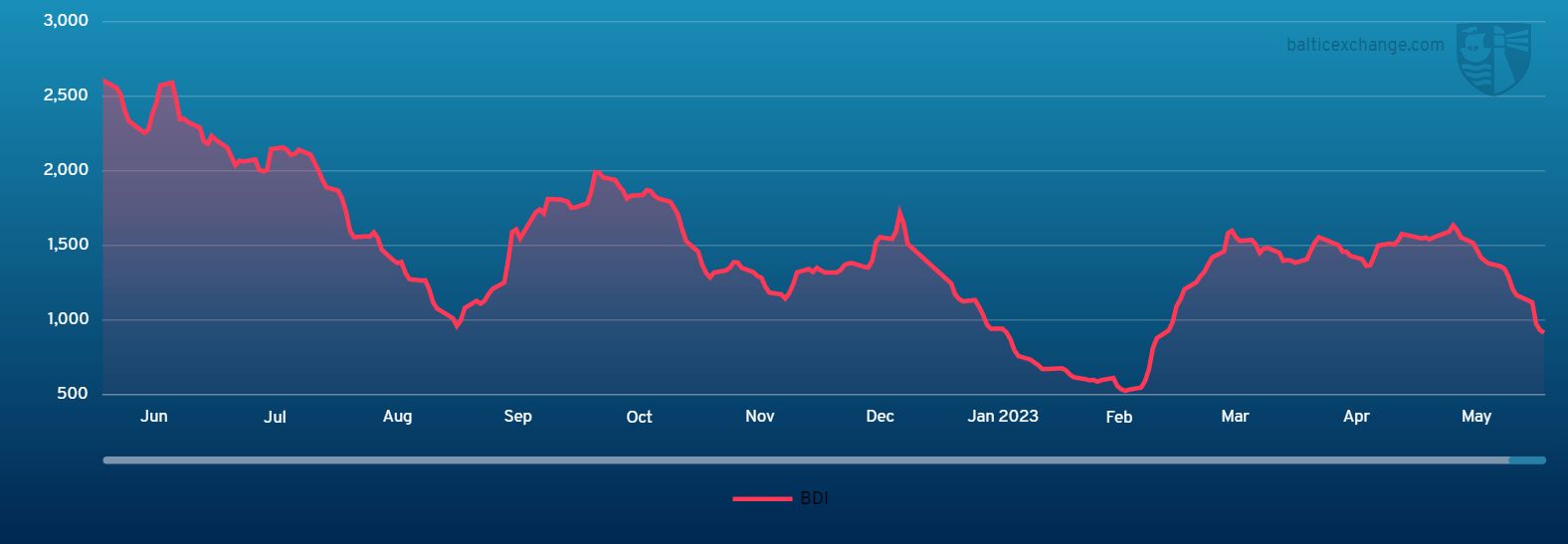

Chart shows Baltic Dry Index (BDI) during June 2, 2022 to June 2, 2023

Baltic Forward Assessment for BDI

In March 2018 the BDI was re-weighted and is published using the following ratios of time charter assessments: 40 percent capesize, 30 percent panamax and 30 percent supramax. The information is provided by a panel of international shipbrokers.

(Source: The Baltic Exchange, edited by Niu Huizhe with Xinhua Silk Road, niuhuizhe@xinhua.org)

A single purchase

A single purchase