BEIJING, April 25 (Xinhua) -- The Baltic Exchange has published its weekly report of the dry and tanker markets for April 17-21, 2023 as below:

Capesize

This week the market saw a slow start, with a healthy supply of tonnage in the Pacific and limited enquiry, particularly from East Coast Australia to China. The market continued to deteriorate on thin volume. By the middle of the week all three majors were in the market from West Australia to China, albeit briefly, and fresh enquiry began to emerge from East Coast Australia to China. A positive paper market also helped to create optimistic sentiment, although towards the end of the week sources had said there had been some profit taking which resulted in rates losing ground. The North Atlantic appeared to be tight on tonnage and at the start of the week and there was a noticeable lack of activity. However, during the week, more enquiry surfaced and stronger fixtures from the North Atlantic were being concluded. As the week comes to an end, most of the activity today has been in the Pacific, mainly from West Australia to China with iron ore, several vessels have been fixed, all at firmer levels. Overall, it has been a positive end to the week.

Panamax

Slow and small gains was the story on the week for the Panamax market. The Atlantic appeared tonnage tight and very positional for the most part with grain trades paying a premium still. Further south, index dates ex EC/NC South America found some levels of support with rates hovering around the $16,000 mark basis route P6 criteria. Asia returned a mixed bag, the north of the arena failed to produce any meaningful demand, allied with an increasing tonnage count the week ended with Charterers seemingly holding the trump cards. Conversely, the south saw a good flow of mineral demand both ex Indonesia and Australia with rates slowing improving as the week progressed, $12,500 concluded several times via Indonesia to China on 76,000dwt tonnage with this mark now closer to $13,000. Period rates remained steady all week with several deals concluded, $18,000 agreed a few times for one-year period on 82,000dwt types.

Ultramax/Supramax

A more positive week for the sector. In the Atlantic stronger numbers were seen from the US Gulf with a shift in tonnage to enquiry balance. Similarly, from East Coast South America, brokers spoke of a tightness in supply of open tonnage. From Asia, with the Eid holidays approaching, there was more coal enquiry from Indonesia which in turn saw an uptick in rates. Further north, demand was steady from the NoPac and there was continued interest for backhaul cargoes. From the US Gulf, a 63,000dwt was heard to have fixed a petcoke run to India at $30,000. Elsewhere, a 63,000dwt fixed delivery Recalada for a trip to China at $16,500 plus $650,000 ballast bonus. From Asia, an Ultramax was rumoured fixed for steels run to the Continent basis delivery Kashima at $11,500. From the south, a 59,000dwt fixed delivery Bahodopi trip via Indonesia redelivery China at $14,250.

Handysize

Despite widespread holidays at the beginning of the week, positivity continued in the Atlantic and returned to the Asia markets, with brokers speaking of more enquiry across both basins and some areas seeing limited tonnage availability. In the US Gulf, a 37,000dwt was fixed for a trip from SW Pass to the Eastern Mediterranean with an intended cargo of grains at $13,000. In the Mediterranean, a 32,000dwt was fixed from Antalya to the Caribbean at a rate between $11,500 to $12,000 and a 36,000dwt was fixed from Samsun via Constantza to Spain-Portugal range at $15,500. In Asia, a 40,000dwt open in Zhoushan to the Continent-Mediterranean range with an intended cargo of Steels at $12,500. Another 40,000dwt was fixed from North China via Australia to the Continent-Mediterranean range with an intended cargo of concentrates at $11,500. A 33,000dwt fixed from Samalaju via Western Australia to East Coast India with Redelivery passing Penang at $9,500.

Clean

LR2

LR2s in the MEG this week saw a quick turnaround and a rapid surge in freight rates. TC1 hopped up 21.25 points to WS178.75 (a round-trip TCE of $45,564 /day). TC20 also shot up, adding $628,000, the index is currently pegged at $4,557,143 after reports of $4,550,000 on subjects.

West of Suez, Mediterranean/East LR2s improved incrementally with TC15 hovering around the $3,550,000 mark all week.

LR1

In the MEG, LR1s have held stable this week. TC5 has remained in the mid WS190s and for a trip West TC8 has held around $3,550,000-3,600,000 level.

On the UK-Continent, TC16 has improved for the second week, climbing 24.64 points to WS202.14 following a flurry of fixing activity during the week and taking the round-trip TCE firmly back up over the $40,000 / day mark to $45,051 /day.

MR

MEG MRs have been steady and poise to move in either direction. The TC17 index has subsequently floated around the WS290-WS300 mark all week.

Up on the UK-Continent activity levels have been notably sedate this week. As a result, the TC2 and TC19 indices have both shed circa 30-35 points and TC2 currently sits at WS283.93 and TC19 at WS233.57.

Over in the Americas, another slower week has seen rates slide again on the MRs. TC14 lost another 16.67 points to WS115 and TC18 came down 19.16 points to WS191.67. On a TC21 trip to the Caribbean the index currently rests at $650,000 (-$137,500) a round trip TCE of $18,624 /day.

Handymax

Mediterranean Handymax vessels saw the TC6 index peak at WS329 midweek only to then return to WS294 after enquiry slowed.

Similarly, on the UK-Continent, the TC23 index leaped up circa 30 WS points to WS250 to then resettle back down at WS242 at time of writing.

VLCC

The VLCC market was weaker this week with rates falling in all areas. The rate for 270,000mt Middle East Gulf to China fell seven points to WS65.32, which translates to a daily round voyage TCE of $47,100 basis the Baltic Exchange’s vessel description.

The rate for 280,000mt Middle East Gulf to US Gulf (via the cape/cape routing) is assessed two points lower at WS44.89.

In the Atlantic market, the rate for 260,000mt West Africa/China dropped 3.5 points to WS66.20 showing a round-trip TCE of $48,700 per day. The rate for 270,000mt US Gulf/China fell over $677,000 to $8,961,111 ($39,500 per day round trip TCE).

Suezmax

The Black Sea and Mediterranean markets have struggled this week with lack of demand leading to general softening of rates alongside little interactions with the Aframax market. A US oil major was reported to have taken a Shell relet earlier in the week for 135,000mt CPC/Med at WS145. With the weakening market, the rate for TD6 is now assessed at WS140.78 (a round-trip TCE of $65,800 per day) - down 17 points week-on-week.

In the Atlantic, owners with ships trading from West Africa have managed to halt the slide in rates, bottoming at WS95 in the first half of the week and are marginally recovering despite the strikes in four major West Africa terminals. With other Atlantic markets showing some signs of life, the rate for 130,000mt Nigeria/Rotterdam now stands at a fraction over WS97.5 (a round-trip TCE of about $36,000 per day). In the Middle East, the rate for 140,000mt Basrah/Lavera eased two points to WS65.

Aframax

In the North Sea market, the rate for the 80,000mt Hound Point/Wilhelmshaven route crashed 35 points to WS128 (a round-trip daily TCE of $33,400).

In the Mediterranean, the rate for 80,000mt Ceyhan/Lavera also had a significant decline, losing 29 points to now be rated at WS147.7 (a daily round trip TCE of $40,600).

Across the Atlantic, the Stateside Aframax market was steadier for the shorter voyages and firmer for the Transatlantic with the majority of owners in position wanting to remain local in order to pick up the expected Transatlantic enquiries.

Some charterers may have already quietly booked tonnage off forward dates. The rate for 70,000mt East Coast Mexico/US Gulf was flat at a little over WS133 ($27,300 per day round-trip TCE) and the rate for 70,000mt Covenas/US Gulf slipped one point to WS128 (a daily round-trip TCE of $23,500).

For the Transatlantic route of 70,000mt US Gulf/Rotterdam, the rate firmed almost 12 points to WS151.5 (showing a round trip TCE of $34,300 per day).

LNG

The spot LNG Market remains flat. Although some spot activity has taken place, there are few requirements and the position list is populated mainly by sublets. Charterers and traders are trying to optimise their usage of extra tonnage while their own programs remain light. This means the list is tighter than it first appears as ships can be taken off quickly into own program. Having a relatively warm spring so far has meant storage and usage are well balanced. This has put more pressure on spot demand as it decreases the need for un-programmed movement. As always, focus has been on period with people looking out to the end of the year to take coverage for what could potentially be another bumper season. Rates themselves barely saw any movement with an Aus-Japan run closing at $54,021 - a drop of nearly $2,500. Meanwhile, a US-Cont rose $1,199 to finish at $42,123. A lower fall for US-East gave the index a publication of $47,976 at the end of the week.

LPG

The LPG market has lost some momentum this last week. Rates across all the three routes have moved very little with BLPG2 shifting only $0.4 over the whole course of the week. Out in the East for BLPG1 the route gained marginal ground of just over half a dollar. But with a tight position list for first half of May there has still been resistance from charterers to begin paying up, even though numerous cargoes have been reported. The TCE earnings for a VLGC on a Ras Tanura-Chiba run remains flat at about $60,895 per day round voyage daily return. For Houston-Flushing and Houston-Chiba very little movement has done nothing to stymie any gains or losses on freight with rates closing at $76, and $127.286 respectively. This has meant there have been slight falls in TCE earnings with BLPG2 to $80,696, and BLPG3 to $59,513 at the end of the week. There was a split of opinion at the close of the week regarding BLPG3 where some participants felt that the publication of $127.286 (a loss of $1.714 on the week) was not as much of a correction as required and a further fall in freight could be expected.

Headquartered in London and a subsidiary of the Singapore Exchange (SGX), the Baltic Exchange publishes a range of indices and assessments which provide an accurate and independent benchmark of the cost of transporting commodities and goods by sea. These include the Baltic Dry Index (BDI), the dry bulk shipping industry's best known indicator. Published daily since 1985, this provides a snapshot of the daily spot market earnings of capesize, panamax and supramax vessel types on the world's key trading routes.

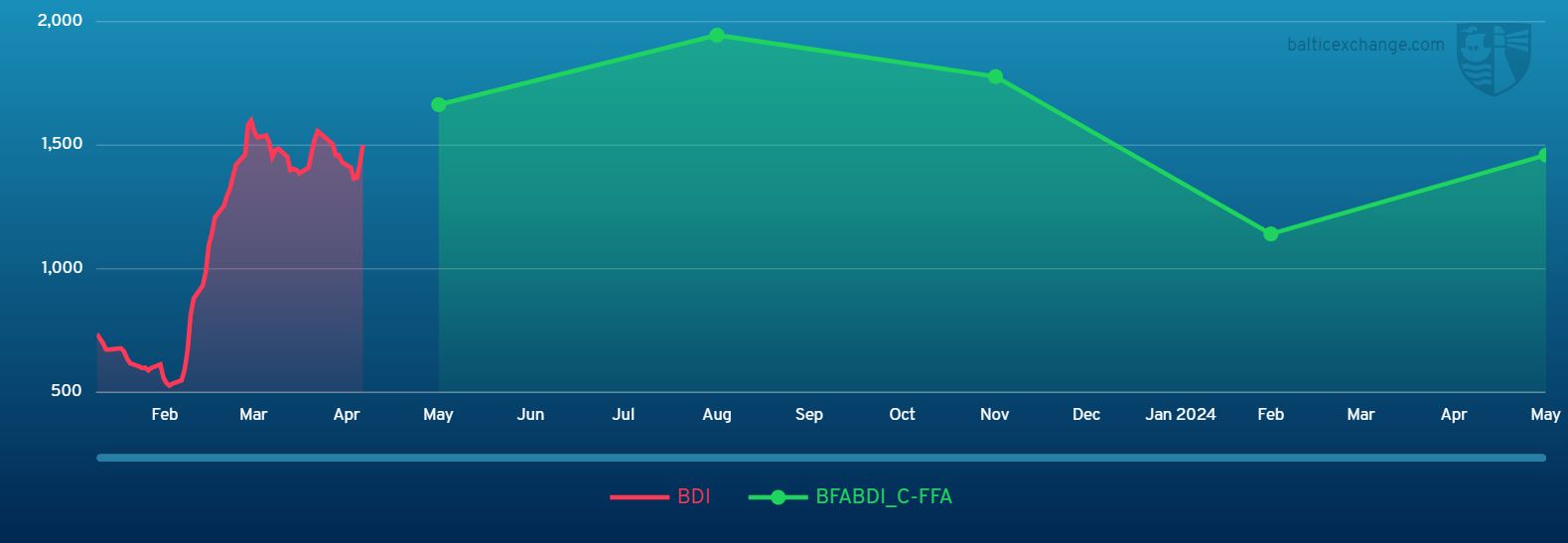

Chart shows Baltic Dry Index (BDI) during April 22, 2022 to April 21, 2023

Baltic Forward Assessment for BDI

In March 2018 the BDI was re-weighted and is published using the following ratios of time charter assessments: 40 percent capesize, 30 percent panamax and 30 percent supramax. The information is provided by a panel of international shipbrokers.

(Source: The Baltic Exchange, edited by Niu Huizhe with Xinhua Silk Road, niuhuizhe@xinhua.org)

A single purchase

A single purchase