BEIJING, May 18 (Xinhua) -- The Baltic Exchange has added quarterly assessments, the gas operating expense (GOPEX), on the cost of operating LNG and LPG tankers to its growing suite of shipping investor tools.

Data will be provided by leading independent third-party ship management companies Anglo-Eastern and AEX LNG Management, Fleet Management and V-Group, the Baltic Exchange said in a news release.

The Baltic Exchange's latest offering follows benchmarking that also covers vessel earnings.

"Adding OPEX indices for gas carriers brings transparency to the marketplace about how much it costs to run an LNG or LPG carrier and complements our data for the spot earnings of these vessels. They assist investors assess health of earnings using independent and reliable information from a credible provider of benchmarks for the shipping industry", said Baltic Exchange Chief Executive Mark Jackson.

It is noted that all values are expressed in USD per day and the published OPEX value is the sum of crew, technical, insurance and fees. Drydock costs do not contribute to the OPEX, but are published for both LNG and LPG vessels.

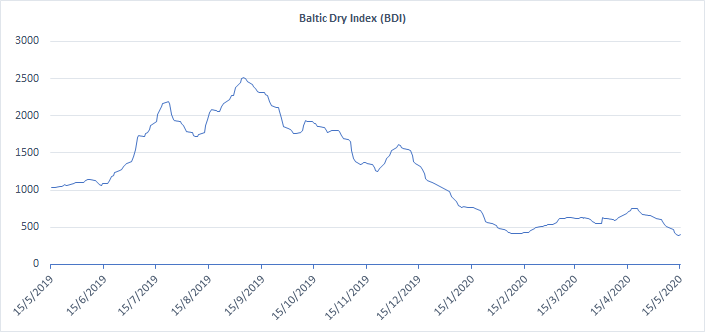

Headquartered in London and a subsidiary of the Singapore Exchange (SGX), the Baltic Exchange publishes a range of indices and assessments which provide an accurate and independent benchmark of the cost of transporting commodities and goods by sea. These include the Baltic Dry Index (BDI), the dry bulk shipping industry's best known indicator. Published daily since 1985, this provides a snapshot of the daily spot market earnings of Capesize, panamax and supramax vessel types on the world's key trading routes.

Chart shows Baltic Dry Index (BDI) during May 15, 2019 to May 15, 2020

In March 2018 the BDI was re-weighted and is published using the following ratios of timecharter assessments: 40 percent capesize, 30 percent panamax and 30 percent supramax. The information is provided by a panel of international shipbrokers.

The Baltic Exchange also publishes weekly report of the dry and tanker markets and below is the weekly report for May 11-15, 2020.

Capesize

A precipitous fall in the market this week had the Capesize 5TC shedding over 50 percent in value. A small rebound at the end of the week gave slim hopes that the market may recover faster than anticipated. The Capesize 5TC lifted +402 to close the week out at $2,394. Market troubles have been well brewed this year. With a concoction of interrupted cargo supplies, vessels racing on cheap bunkers, weather events, and demand destruction amid the COVID-19 pandemic, the market is in need of a positive. The iron ore stockpile situation in China has inventories dropping sharply, which will surely require tonnage. Half way through Q2 - and with many economies looking to re-open - there is talk of infrastructure spending to rekindle the flames, which will again require iron ore. While not an immediate relief, prospects are not all bleak. The West Australia to China C5 closed up +.314 to close the week at $3.942. While the Brazil to China C3 was heard to be better bid closing out the week up +.28 settling at $6.975.

Panamax

Rates in the Atlantic came under severe pressure this week. Sizeable losses on the respective routes, with absent mineral demand and long tonnage counts alleviated by ballaster numbers from the East in recent weeks, only compounded a bleak situation. Asia appeared to resist the negative sentiment emanating from other areas. There was a healthy volume of fresh enquiry and volume of fixtures, with the North Pacific seeing a steady flow of enquiry. However, minerals from Australia and Indonesia were the more dominant. End-week rates here were looking softer in most areas. EC south America saw healthy levels of fixing throughout the week but index-type tonnage by Thursday were only capable of achieving sub $11,500 + $150,000 numbers delivery at the port with a ballast bonus. NoPac rounds in the pacific hovered around the $6,000 for 82,000dwt, whilst the median rate for shorter Indonesian round trips lent towards the $5,000 mark.

Ultramax/Supramax

With a few areas in the world slowly getting back to a "new normal", demand on the Ultramax/Supramax size increased. However, this split into two main camps with the Atlantic overall still soft, whilst from Asia and the Indian Ocean activity levels and rates increased. Little was reported on period activity. But a 56,000-dwt open Kandla was failed for five to eight months trading in the high $5,000s for the first 40 days - and $8,000 thereafter. From the Atlantic, east coast South America lacked enquiry with Supramax being fixed in the $4,000s for transatlantic runs. The east Mediterranean/Black Sea saw increased activity with cargo and tonnage being a little more balanced. All Asian routes gained ground during the week, a 55,000 open Iligan fixing at $6,500 via Indonesia redelivery India. The Indian Ocean had pent up demand, with a 63,000 fixing delivery South Africa for a trip to the Far East at $11,000 plus $150,000 ballast bonus.

Handy

Midweek, the BHSI reached its lowest point of the year, with the same level last seen in early March 2016. The downward momentum in the Atlantic remained in all key areas. However, positive sentiment gained pace in the Pacific, with better rates discussed and more activity appearing in general. A mid/large Handy vessel was fixed from the north coast South America for a trip to the Far East at a rate close to mid $7,000s. A 37,000-dwt was fixed from Norfolk for a trip to the Continent/Baltic and a 33,000-dwt was fixed from Southwest Pass for a trip to east Mediterranean both at $2,500. In the East, more logs cargoes from New Zealand lent support and put vessels in Southeast Asia in demand. A 33,000-dwt open spot in CJK was fixed at $3,500 for a trip to Southeast Asia.

Clean

Reverse gear was the name of the game this week as clean markets everywhere continued their dramatic falls. In the Middle East Gulf, the rates almost halved with 75,000mt to Japan now assessed at barely WS200, having started the week at WS387.5. The LR1s also followed suit, losing over 180 points to barely WS200 basis 55,000mt and remain under heavy downward pressure here. In the 37,000mt UKC to USAC trade rates began the week at WS 167.5, peaking at just below WS170 before falling away to settle at WS150 region. The market in the 38,000mt backhaul trade from US Gulf to UKC was flooded with tonnage and rates fell 15 points to WS87.5. The 30,000mt clean cross-Med trade continued its dramatic decline, with the market down 36.25 points at WS105 with charterers rather spoilt for choice here.

VLCC

There has been a good volume of fixtures in the Middle East Gulf as charterers worked towards covering the balance of May cargoes. Next month will see fewer fixtures as there will be less cargoes due to the OPEC+ cuts, with reports of one charterer getting a third of their requested stems from Saudi Arabia - and the Kuwaitis reported to be aiming for their contractual minimums. Owners this week have managed to maintain rates, with 270,000mt to China at WS59 level, while 280,000mt to USG via the cape/cape routing remaining at just under WS35. In West Africa a similar tale bore out with rates remaining flat at WS57. In the Gulf of Mexico little activity was seen, with only a couple of cargoes being covered. Rates for 270,000mt USG/China voyages slipped $400k to now be assessed around $6.5m.

Suezmax

Rates in this sector remain under downward pressure, particularly in West Africa and the Middle East. The market for 130,000mt Nigeria/UKCont is currently assessed at mid WS80s, down 5 points. However, due to the downturn of Middle Eastern fortunes for shipowners there are several ballasters from the East looking ex West Africa, demonstrating a weaker feel to both markets. Rates for 140,000mt Basrah/Med took a 10-point dive yesterday to WS45 level, as a trader’s relet was taken by a Greek refiner at the equivalent of low WS40s. In the 135,000mt Black Sea/Med market rates have remained flat around the WS90 level.

Aframax

There were mixed fortunes in this sector, with rates for 80,000mt Ceyhan/Med falling steadily to WS110-112.5 level, down 20 points, with owners still trying to find the floor. Meanwhile, in North Western Europe rates for 80,000 Cross-North Sea were boosted by 15 points to WS115 and the 100,000mt Baltic/UKC route gained a modest 5 points. Across the Atlantic, rates for 70,000mt Carib/USG climbed 15 points to WS145 level, and 70,000mt USG/ARA is up 10 points to WS135.

(Source: The Baltic Exchange, edited by Niu Huizhe with Xinhua Silk Road, niuhuizhe@xinhua.org)

A single purchase

A single purchase